Phynart Studio/E+ via Getty Images

There is no point in using the word ‘impossible’ to describe something that has clearly happened.”― Douglas Adams

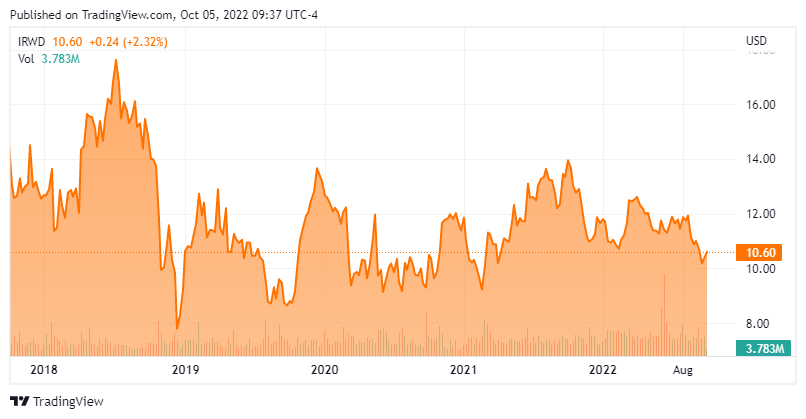

Today, we are putting Ironwood Pharmaceuticals, Inc. (NASDAQ:IRWD) in the spotlight for the first time since our last piece on this small-cap biopharma almost exactly a year and a half ago. The recommendation then was IRWD made for a good covered call candidate. That seems to have been the right call in retrospect, given the stock has largely traded sideways since. Does that thesis still hold? An analysis follows below.

Seeking Alpha

Company Overview:

Ironwood Pharmaceuticals, Inc. is based out of Boston. The stock currently trades around $10.50 a share and has an approximate market capitalization of $1.6 billion. The company’s only product on the market and really only asset of note is a compound called Linzess.

Linzess speeds up transit through the intestine to reduce intestinal pain and has been approved for irritable bowel syndrome with constipation (IBS-C) as well as chronic idiopathic constipation (CIC) for approximately a decade. This compound is an orally-dosed, room temperature-stored agonist of the enzyme guanylate cyclase type C that increases the production of that enzyme in the lining of the intestine.

Linzess is marketed outside the country by the brand name Constella via a marketing partnership with drug giant AbbVie (ABBV). Within this arrangement, Ironwood splits the profits and losses 50/50 from the sale of Linzess in the North America and is eligible to receive royalties from AbbVie for all other territories ex-N.A. except China and Japan.

August Company Presentation

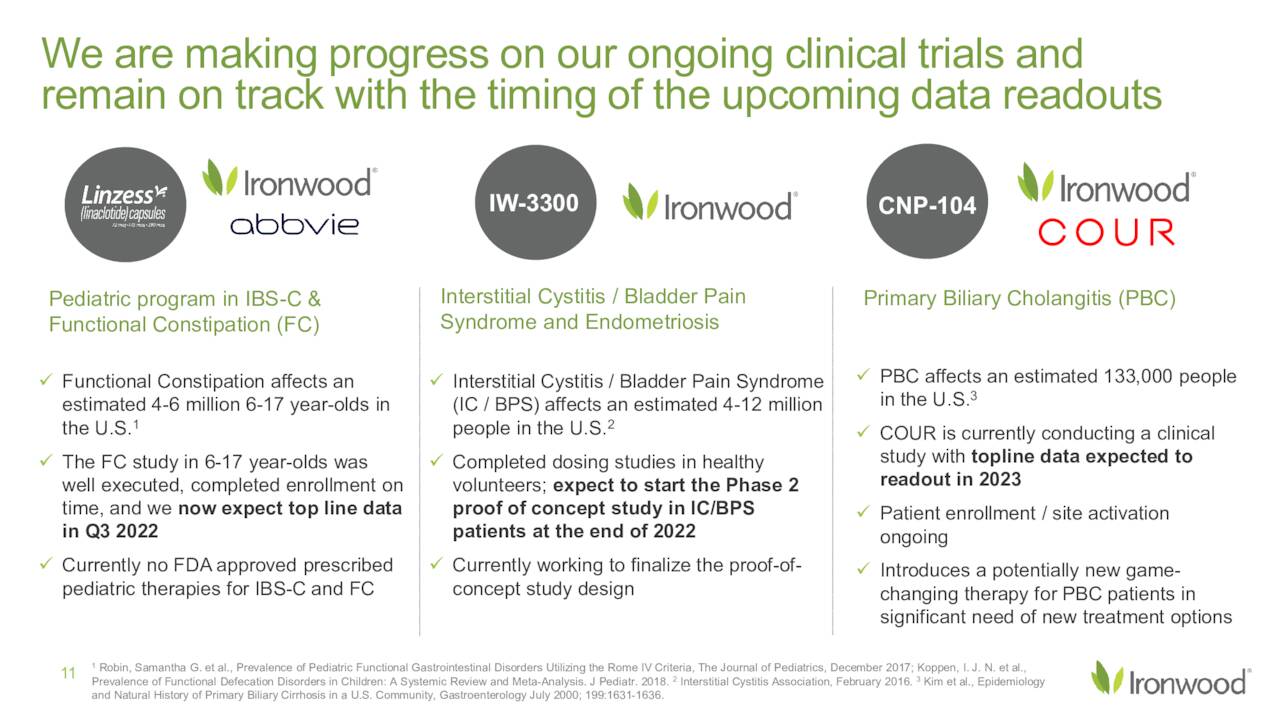

The company is currently moving forward in getting Linzess approved or 6 – 17-year-olds where there is no currently approved drugs for these indications. The company positive results from a late stage trial in this effort in September and is in the process of submitting a Supplemental New Drug Application or sNDA. The company has other drug candidates (IW-3300 and CNP-100) in its pipeline, but they are in too early stages of development to be germane to this analysis.

IRWD’s Second Quarter Results:

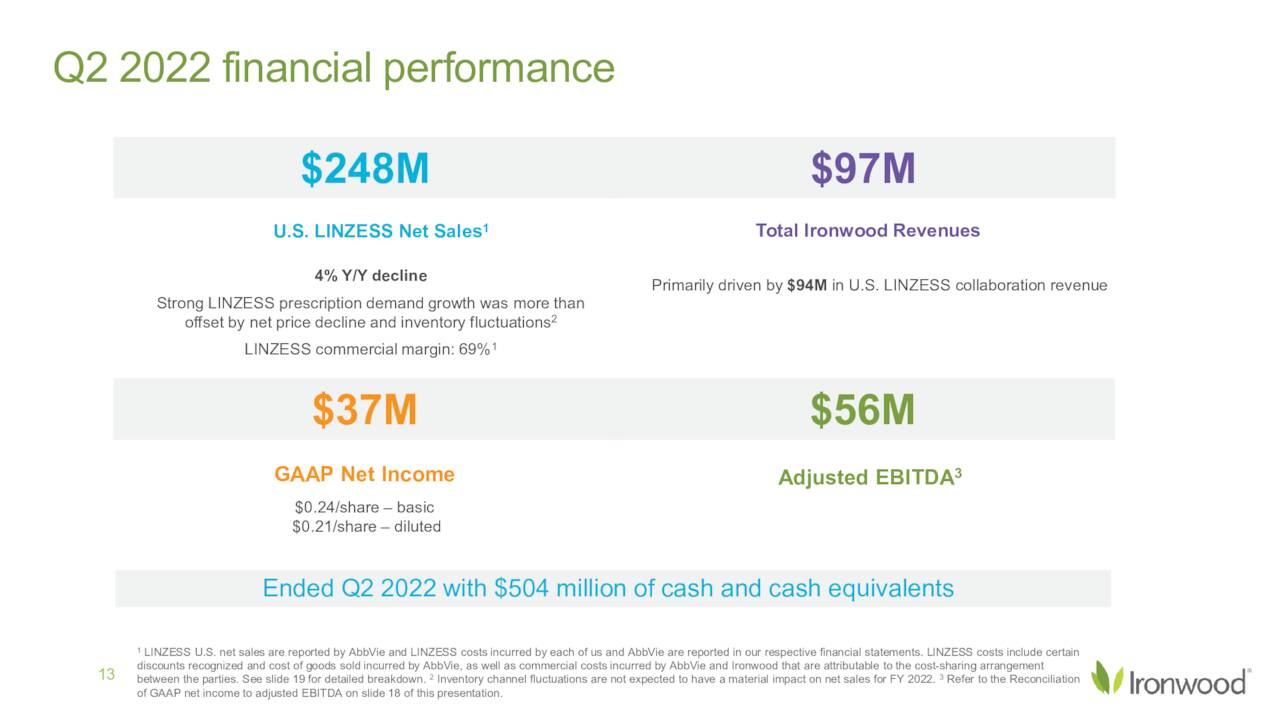

The company reported second quarter numbers on August 4th. Both the top and bottom line results missed analyst expectations. Ironwood had a non-GAAP profit of 21 cents during the quarter even as revenues shrunk just over six percent on a year-over-year basis to $97.2 million. GAAP net income for the quarter was $37.2 million.

August Company Presentation

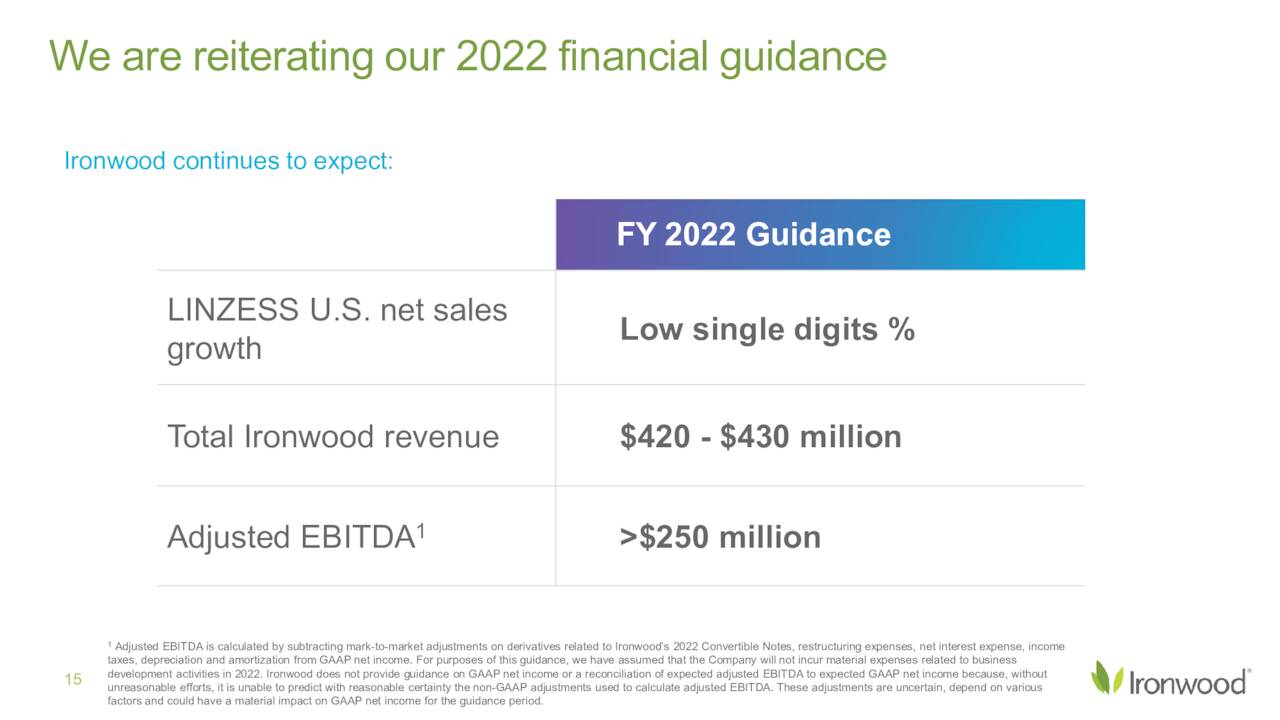

Management did reaffirm full year revenue guidance of between $420 million to $430 million despite these disappointing quarterly results.

August Company Presentation

Analyst Commentary & Balance Sheet:

Over the past six months, Piper Sandler has initiated the shares as a new Overweight rating with a $16 price target. Capital One Financial did the same with a $15 price target. Meanwhile, JP Morgan and Wells Fargo have maintained Hold ratings with identical $13 price targets as has Cowen & Co. with a $9 price target.

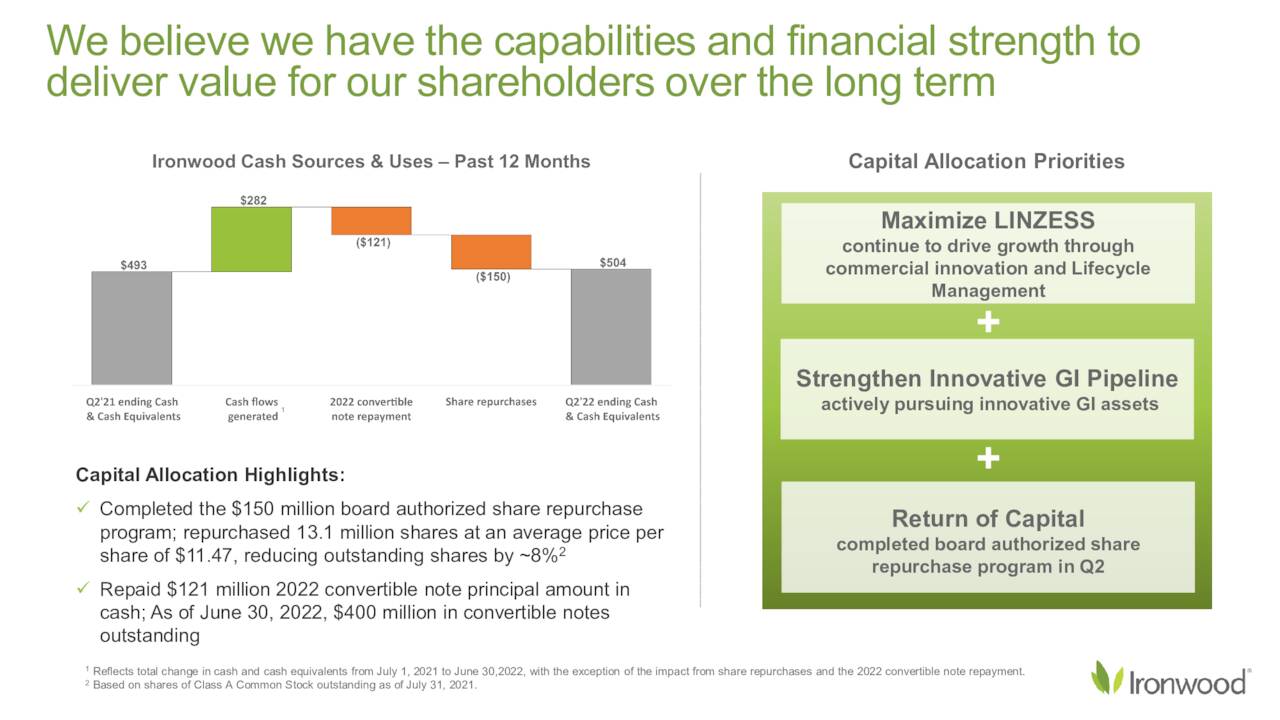

Insiders have been frequent sellers of the stock so far in 2022. In the third quarter, they sold nearly $5 million worth of shares in aggregate. Just over one out of every eight shares of outstanding float is currently held short. At the end of the second quarter, the company held just over $500 million worth of cash and marketable securities on its balance sheet against just less than $400 million of long term debt.

August Company Presentation

The company completed a $150 million stock buyback program in the second quarter of this year. It also fully repaid the remaining balance on a $120.7 million convertible note in cash during the quarter as well. The company generated $61.4 million in cash from operations in the second quarter of 2022, compared to $48.6 million in cash from operations 2Q2021

Verdict:

The current analyst firm consensus has Ironwood earning 97 cents a shares as revenues rise less than two percent to $420 million in FY2022. They project six percent revenue growth in FY2023 as well a nice rise in EPS to $1.24.

August Company Presentation

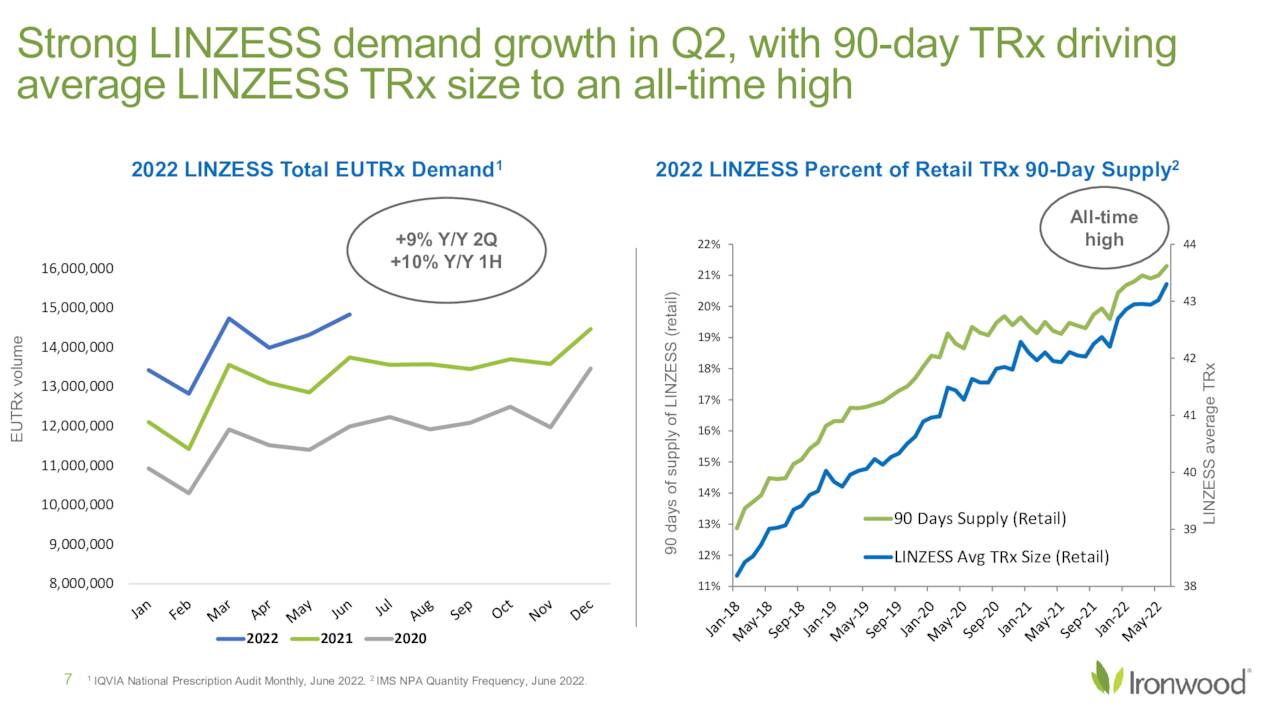

It is hard to find that much exciting about Ironwood at the moment even as Linzess continues to see solid demand. That said, the stock is fairly cheap at 11 times forward earnings, especially in light that both revenue and earnings growth should meaningfully accelerate in FY2023. The stock is even cheaper measure on a Price/Operational Cash Flow valuation.

With the stock trading in the lower end of a long term range, a worst case scenario seems to be the stock is “dead money” here. A best case one that the equity rises back to the top of its trading range in the coming quarters. Therefore, a covered call strategy seems to continue to be the best way to play what has been a ‘rinse, wash and repeat‘ trade within my own portfolio.

It is useless to attempt to reason a man out of a thing he was never reasoned into.”― Jonathan Swift

Be the first to comment