gorodenkoff/iStock via Getty Images

One of the best things about technology is that it creates entirely new industries that our ancestors never would have imagined to be possible. Many of these industries are good because of the contributions they make to society more broadly. But unfortunately, there are downsides to technology that makes other industries necessary. One great example of this would be the cybersecurity market. In an ideal world, we wouldn’t need to worry about bad actors and faulty technology. But unfortunately, the world doesn’t work that way. For the companies that do plight in this market, one smaller prospect that is interesting to look at is a firm called IronNet (NYSE:IRNT). Having only recently gone public, we have a limited view of the company’s financial track record. What we do have, however, shows that revenue might be primed to grow modestly in the near term. But even with that growth, the company’s bottom line looks far from impressive and investors would be wise to tread cautiously moving forward.

IronNet – A cybersecurity play

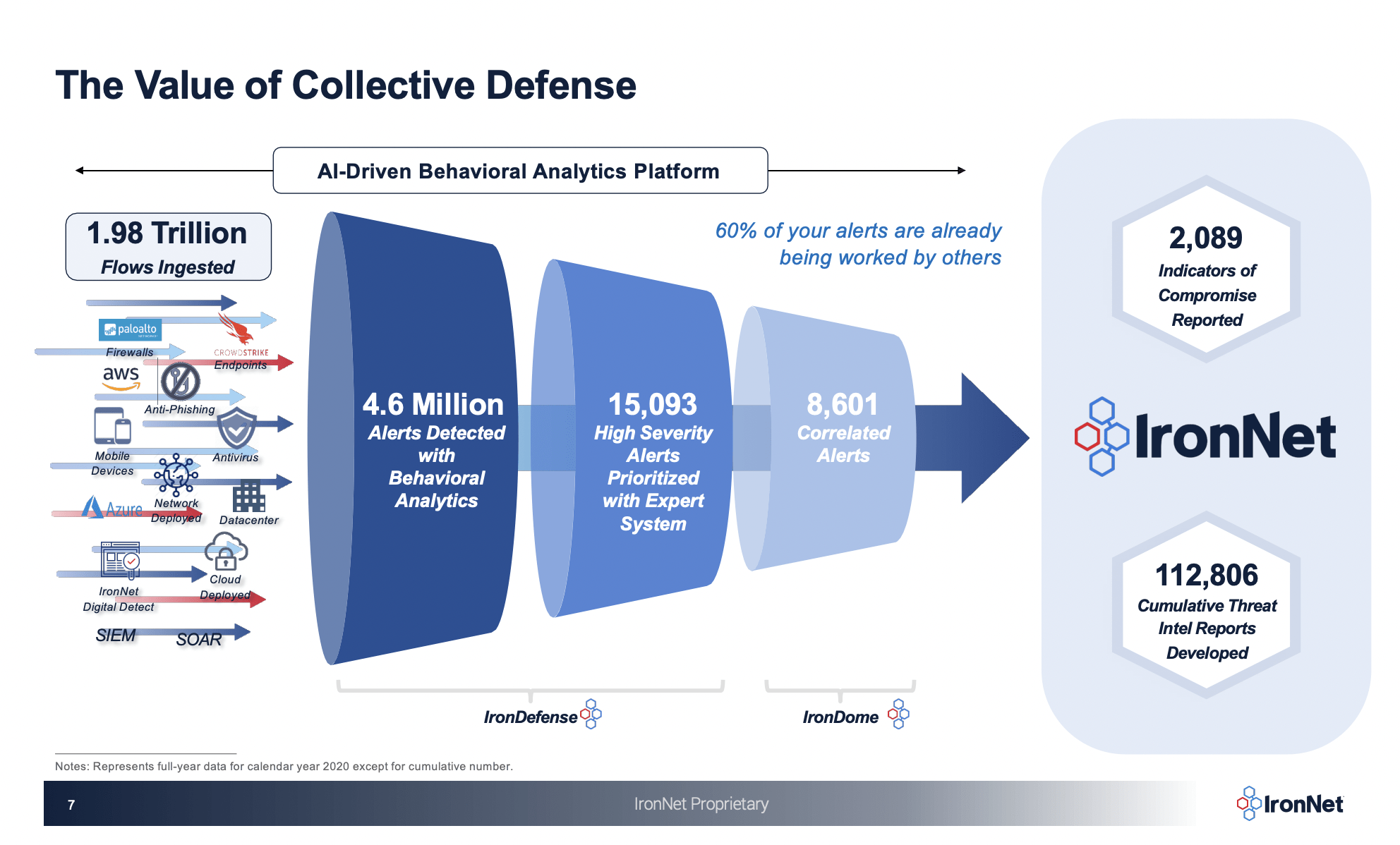

As I mentioned already, IronNet focuses on the cybersecurity market. The company’s particular business model revolves around what management refers to as Collective Defense, which utilizes artificial intelligence centered around behavioral science in order to detect and prioritize anomalous activity inside of individual enterprise network environments. In essence, the platform works by analyzing threat detections across the platform in order to identify broad attack patterns. The platform then provides anonymized intelligence back to all community members involved in the platform so that they can have insight into potential incoming attacks. At this time, there are really two key components to the strategy. The first of these is called IronDefense, which serves as an advanced network detection and response service aimed at detecting a large range of both known and potentially novel cyber threats. The second is known as IronDome and involves an automated cyber defense solution that helps to deliver threat knowledge and intelligence across various industries at rapid speed.

IronNet

In one example of how the company’s technology works, which utilizes data covering the entire 2020 calendar year, the company’s behavioral analytics platform ingested 1.98 trillion ‘flows’ worth of data. The IronDefense platform detected 4.6 million alerts through the use of behavioral analytics. It then narrowed this down to over 15,000 high severity alerts that it then prioritized using the company’s expert system. From there, the IronDome platform narrows this down further to about 8,600 correlated or alerts that ultimately resulted in just under 2,100 indicators of compromise being reported and 112,806 cumulative threat intelligence reports being developed. At the end of the day, this service really seems to be focused on cyber detection so that the appropriate actors can respond as needed.

IronNet is not a great company fundamentally

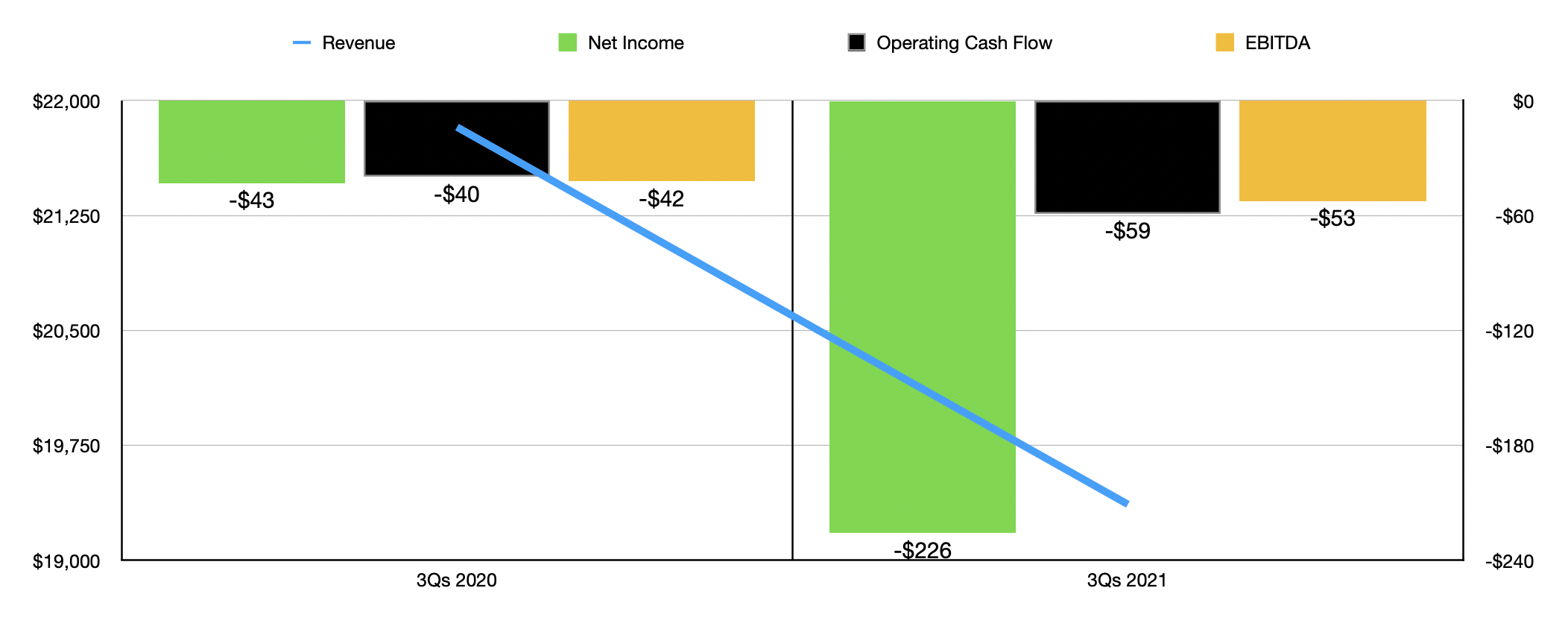

Although the cybersecurity industry likely does have tremendous potential in the long run, potential that will never cease to grow so long as technology continues to expand and become more complicated, this does not mean the company is likely to be a strong prospect. For instance, the firm’s track record has been rather disappointing. In the first nine months of its 2021 fiscal year, for instance, the business generated revenue of $21.83 million. This figure dropped to $19.37 million one year later. On the bottom line, things also worsened. The firm’s net loss from the first nine months of its 2021 fiscal year was $43.16 million. The loss widened to $225.79 million for the same timeframe last year. To be fair, a big contributor to this change involved a $160.16 million charge associated with stock compensation. Because of this, cash flows would be a more appropriate indicator of the company’s prospects. But even that fails to impress. In the first nine months of its 2022 fiscal year, for instance, the business generated net cash outflows of $59.10 million. This compares to the $39.90 million in cash flows reported one year earlier. Even EBITDA worsened during this time frame, declining from negative $42.26 million to $52.55 million.

Author – SEC EDGAR Data

If there is any good news, it’s that management has provided some interesting data ahead of the earnings release. While revenue for the year should be about $26 million, the company did say that annualized recurring revenue should be about $30 million. That implies growth for the firm’s 2023 fiscal year, which is never a bad thing. Interestingly, management does have a different opinion than what analysts expect. For the final quarter of the year, management’s guidance implies revenue of $6.64 million. This is actually less aggressive than the $6.77 million anticipated by analysts at this time. It’s also worth noting that the company is still probably going to generate a net loss. The loss per share for the final quarter should be about $0.20. Given the number of shares currently outstanding for the company, that should translate to a net loss of about $19.07 million.

As you can see, fundamentally speaking, IronNet just really is not a great business at this time. That’s not to say the firm doesn’t have anything good going for it. It operates in an interesting market with excellent potential. More specific to this particular enterprise, the company also has a rather robust balance sheet. It currently has no debt and possesses $73.89 million in cash and cash equivalents. That brings the company’s enterprise value down to a modest $283.66 million. On top of that, the company recently paid $1.75 million to Tumin Stone Capital in order for that company to be required to buy up to $175 million worth of IronNet’s shares over a 36-month window. Absent management having to jump through some hoops, the actual number likely to be purchased, at current pricing, implies proceeds of closer to $66.5 million. But the bottom line is that the company has an easy avenue for issuing stock in exchange for cash. Of course, this also comes with the downside of further dilution for investors. But given that the business continues to generate negative results, I don’t think many shareholders would complain about this kind of scenario playing out.

Takeaway

At this point in time, IronNet may be an interesting company. But it’s far from a healthy one. Financial performance for the company has not been impressive and it’s not great to see continued negative cash flows and EBITDA. While it’s possible the company could well benefit from industry demand moving forward, investors should be careful with this prospect until we have more information on what the future holds. The one saving grace the business has is access to significant amounts of cash, but at some point that comes at a high cost to investors as well.

Be the first to comment