gorodenkoff

IQVIA Holdings (NYSE:IQV) is one of my favorite companies both in terms of their business and as an investment. I have been a fan of IQVIA thanks to its cutting-edge analytics, tech solutions, and clinical research services to customers around the globe. Admittedly, I was concerned that the company was going to have a rough time coming out of COVID, but they have continued to deliver strong financial marks in the face of market distresses, wide-ranging macroeconomic concerns, and the nearly countless global geopolitical disputes. The relentless demand for IQVIA’s products and services shows how they are leaders in the industry, which I believe justifies the ticker’s premium valuation.

I intend to provide a brief background on IQVIA and the company’s recent performance. In addition, I discuss the company’s current valuation and why I believe it is warranted. Finally, I deliberate on my plans for my dormant IQV position.

Background On IQVIA

IQVIA is one of the top contract research organizations “CROs” that provides services for the development of healthcare products through Phase I-IV clinical trials. In addition, they work on the lab and analytical services as well as consulting services. IQVIA has over 10,000 customers including all the top 25 big pharma companies around the globe.

IQVIA has three segments of their business:

- Technology & Analytics Solutions “TAS”

- Research & Development Solutions “R&DS”

- Contract Sales & Medical Solutions “CSMS”

The Technology & Analytics Solutions segment has an assortment of cloud-based applications and services such as advanced analytics and commercial performance metrics for healthcare products. IQVIA is the go-to for sales data for pharmaceutical products, prescribing trends, medical treatments, and promotional activity in the retail, hospital, and mail-order settings. Moreover, their sales or prescribing activity data can be broken down to the regional, zip code, and individual prescriber levels.

IQVIA’s Research & Development Solutions segment helps companies with project management and clinical trial support. IQVIA can be involved in basically every step of a product’s development including the trial’s planning and design, as well as providing a wide range of laboratory services. These services include discovery, genomic, bioanalytical, ADME, and biomarker lab work.

The company’s Contract Sales & Medical Solutions segment works with providers, patient services, and medical affairs services. In addition, the company assists a variety of healthcare companies including pharma, biotechs, devices, diagnostics, and consumer health.

The company has a strong track record for growth and beating earnings estimates.

IQVIA Earnings History (Seeking Alpha)

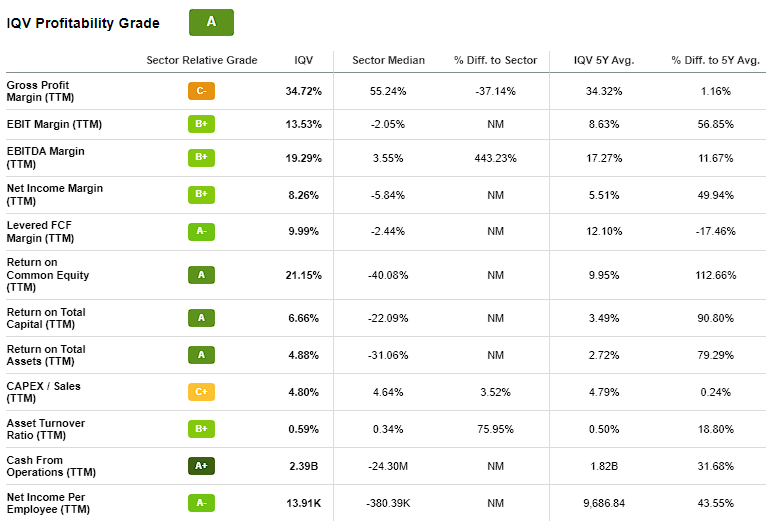

In fact, IQVIA has only reported a year-over-year decrease in revenue for Q2 of 2020… which I believe is excusable considering the global shutdowns due to COVID-19. In terms of growth, the company has a five-year average revenue growth of around 13%, and EPS diluted growth of about 288%. When looking at profitability, IQVIA is a paragon with impressive grades across the board with strong margin ratios, and return ratios.

IQVIA Profitability Metrics (Seeking Alpha)

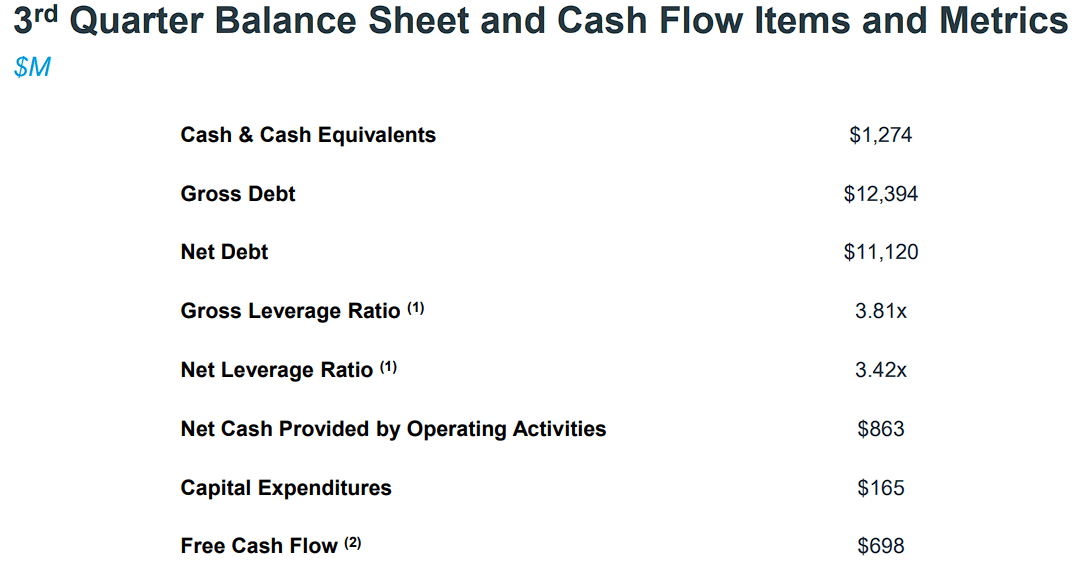

In terms of financials, the company finished Q3 with ~$1.274B with their gross debt around $12.394B.

IQVIA Q3 Balance Sheet and Cash Flow Metrics (IQVIA)

IQVIA does have a share repurchase program in place with the company repurchasing a touch above $1.1B between the start of 2022 and the end of Q3. What is more, the company still has just under $1.4B of share repurchase authorization remaining under the current program.

Recent Performance

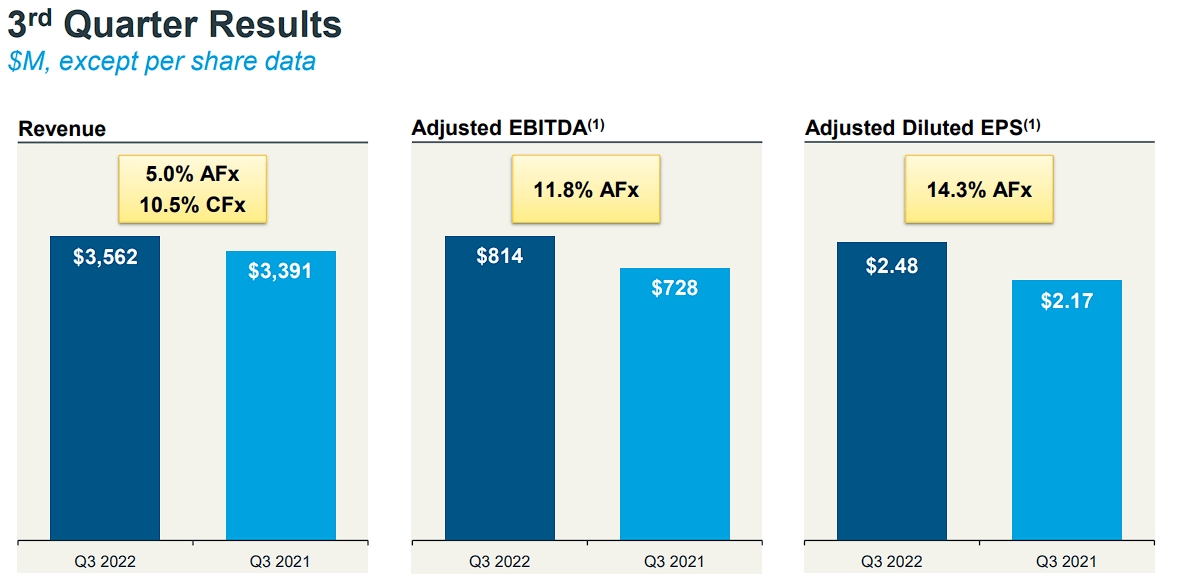

Back in October, IQVIA reported their Q3 revenue was $3.562B up 5% on a reported basis “AFx” and 10.5% at constant currency “CFx”. When excluding COVID revenue, the company’s base business experienced 14% organic growth CFx.

IQVIA Q3 Earnings Results (IQVIA)

The TAS revenue was $1.4B, up 4.7% AFx and 11.6% CFx, while the R&DS revenue came in at $1.979B, which was up 6.8% AFx and 10.7% CFx. However, CSMS revenue was $183M, which dropped 9% but grew 1% CFx.

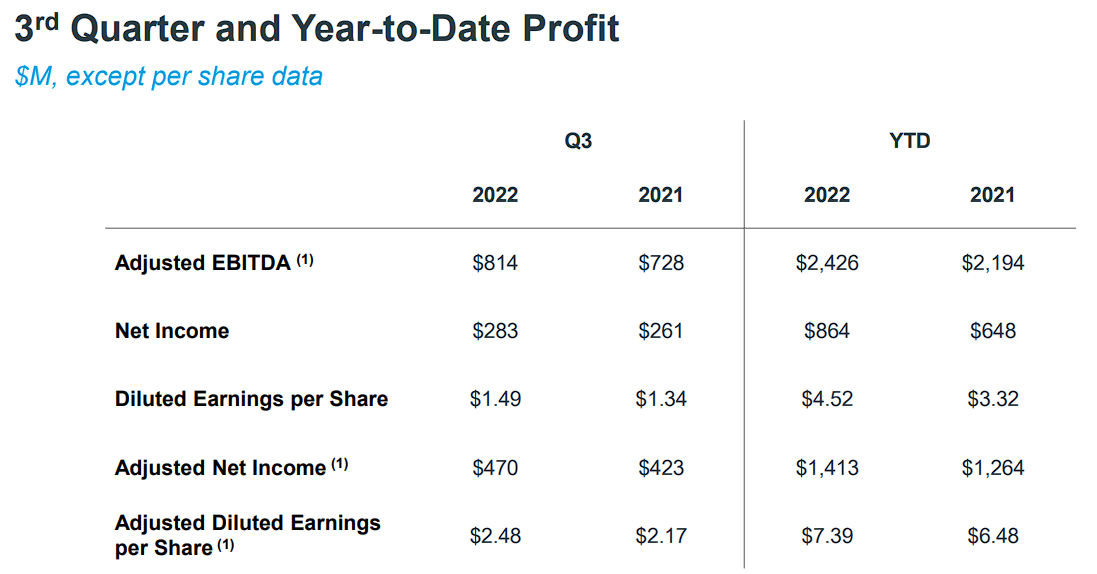

The company reported their Q3 adjusted EBITDA was $814M, signifying 11.8% growth over the first three quarters of 2022. IQVIA’s Q3 GAAP net income was $283M and GAAP diluted earnings per share were $1.49. The GAAP net income for the first three quarters of 2022 was $864M, which is $4.52 EPS.

IQVIA Q3 and Year-To-Date Profit (IQVIA)

IQVIA’s Q3 cash flow from operations came in at $863M, while CapEx was $165M yielding $698M free cash flow.

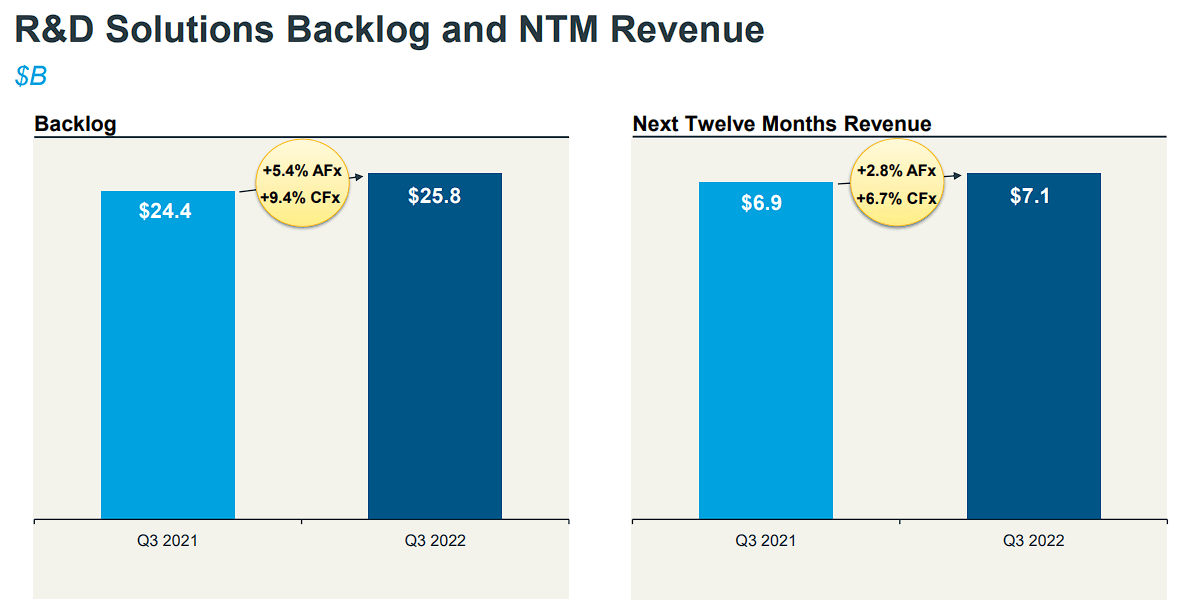

Another highlight to note is that the company’s backlog at the end of Q3 was up 5.4% year-over-year at a record $25.8B.

IQVIA R&D Backlog and Next-Twelve-Months Revenue (IQVIA)

This led to an increase in the next 12-month “NTM” revenue from backlog to $7.1B, up 2.8% year-over-year AFx, and 6.7% CFx.

Looking at the results, I think it is safe to say the company’s business is healthy with strong free cash flow performance and revenue growth hitting the mid-teens when excluding COVID-related revenue. Some highlights include the company’s RDS business bookings hitting a record of $2B for the quarter and their contracted backlog was at a new record of $25.8B at the end of Q3.

Discussion On Valuation

At the moment, IQVIA is trading at a premium valuation when considering its price-to-book (7.77x) and its price-to-earnings (36.35x). In addition, the ticker is also trading on the rich side when you take a look at the EV/EBITDA and Earnings Power Value models.

Typically, I am not willing to pay a premium for stocks, including industry leaders that have a strong track record of growth. For IQV, I am willing to pay a premium for several reasons that make it a unique ticker in my “Bioreactor” growth portfolio. First, IQVIA is considered one of the world’s leading CROs and offers a comprehensive list of products and services that have a steady demand. IQVIA has been able to thrive despite the global macro environment including wage inflation, high levels of attrition, obviously the ongoing Russia-Ukraine disruptions, and reoccurring China lockdowns that have impacted the industry.

Second, IQVIA doesn’t really have a long list of competition that can match up against it. Indeed, Thermo Fischer’s (TMO) acquisition of PPD at the end of 2021 makes them a formidable force in the CRO industry. Syneos Health (SYNH) and several other companies could be challengers for IQVIA in specific industries or categories, but most do not have the broad portfolio IQVIA offers.

Third, IQVIA has an awesome growth track record and is expected to report strong growth for both EPS and revenue over the next few years.

IQVIA EPS Estimates (Seeking Alpha) IQVIA Revenue Estimates (Seeking Alpha)

In fact, if you consider the company’s projected growth and cash flow, IQVIA is trading at discount.

Value Investing IQVIA Valuation Models (Value Investing)

I have a few valuation models that point to IQV having a significant upside from its current levels. The 5-year growth exit DCF has IQV at $251 and the 10-year pointing to $374 per share.

Indeed, we don’t know if this projected growth will come to fruition, however, industry trends reveal that clinical trial starts up 8% from 2019 pre-pandemic levels. Also, keep in mind that the company’s backlog grew 5.4% versus the prior year on a reported basis, so IQVIA is benefiting from the increased activity.

Looking to the future, the dramatic increase in industry data access and complexity should benefit IQVIA as customers turn to them for superior information management capabilities. Indeed, the company’s “top 10 pharma clients selected IQVIA’s human data science cloud to power large scale data and analytics programs by centralizing and harmonizing data for 35 large countries across their primary care and specialty medicine portfolio.” On the commercial side, IQVIA had their top 20 pharma clients choosing “IQVIA’s commercial technology ecosystem suite to transform its commercial operations into an AI-enabled commercial model.” So, it appears as if the company’s products and services are only gaining more traction on a long road with its top customers.

What is more, IQVIA has recently made some noteworthy acquisitions, including Lasso Marketing and DMD Marketing Solutions. These additions have expanded IQVIA’s marketing services to help their customers reach new targets and improve brand awareness. Making deals is a great way for IQVIA to ensure growth and be able to change with industry trends, thus, maintaining their position.

Considering the points above, one must concede that IQVIA has the pedigree and prowess to continue to grow, as well as the leadership that can make the right moves to ensure they will achieve those goals. Even with a minor setback or headwind, I would still see IQV as a premium ticker worthy of a premium valuation.

My Plan

Despite my bullishness on IQV, my position has been mostly dormant throughout 2022 and into 2023. This was not due to a lack of conviction, but rather a preoccupation with scanning a target-rich environment of undervalued and oversold healthcare tickers that were too enticing to neglect. Now that I have gotten my fill of those opportunities, I need to return to my primary targets that have the capacity to flourish in any market environment… including IQV.

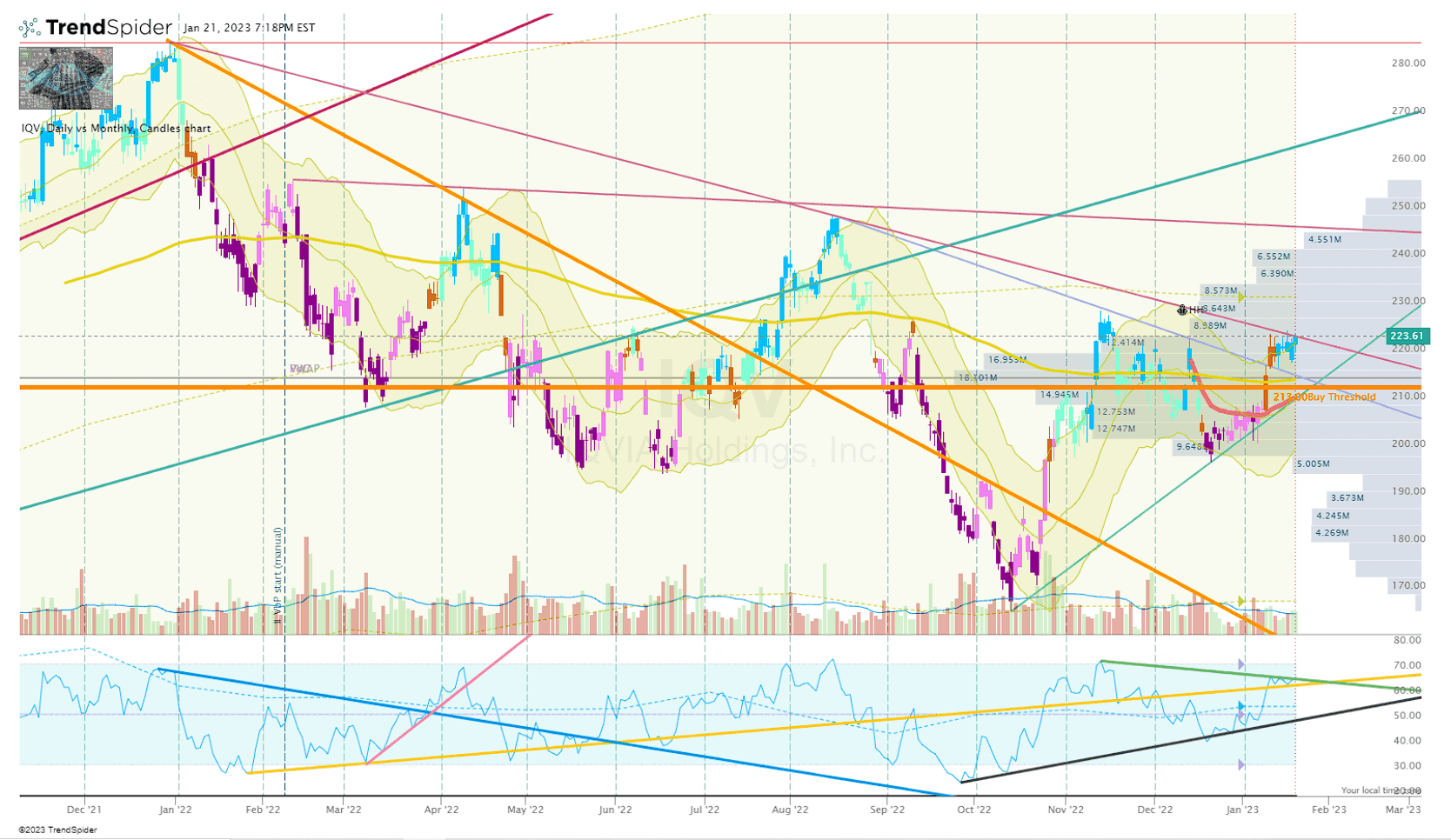

My current “Buy Threshold” for IQV is $213, with my Buy Target 1 and Buy Target 2 set at lower levels. Considering the share price is currently trading around $224 per share, I am currently sitting on my hands until the share price drops below my Buy Threshold. If it does, I plan on being more aggressive with my share sizing and frequency compared to my typical approach of waiting for my Buy Target 1 or Buy Target 2 before getting serious.

IQV Daily Chart (Trendspider)

IQV Daily Chart Enhanced View (Trendspider)

In fact, I might have to make adjustments to my targets to account for the company’s projected growth and the ticker’s technicals. If you take a look at the daily chart, you can see a potential inverse head-and-shoulder setup, which can be a bullish formation to move the share price to a higher level, while providing firm support. If we break and hold above the high of this formation (roughly $250 per share), I will have to adjust my targets higher to account for a new trading range.

On the other hand, I believe I will stick to my current Sell Targets to ensure I am booking profits and moving my position back to a “House Money” status. The goal is to achieve house money status by book profits at a series of sell targets. However, I will maintain a small remnant lot of shares to build up another position for another round of trades and/or hold for a long-term investment.

Be the first to comment