Spencer Platt

Overview

This post serves as an update to my coverage in September.

I still think iQIYI, Inc. (NASDAQ:IQ) is underappreciated. I anticipate increased transparency on IQ’s delivery of positive OPM as management shifts its focus to profitability and efficiency by optimizing content costs and OPEX and adjusting its content investment-centric revenue growth strategies. However, I continue to be wary of IQ’s subscription revenue growth, as the positive impact of an improving average revenue per member in a relatively stable pricing environment is offset by slow subscription growth. The continued time-spent share loss to SFV (short-form videos) platforms, tightened regulations, and COVID’s resurgence all have the potential to further delay the advertising industry’s ability to recover.

Performance review

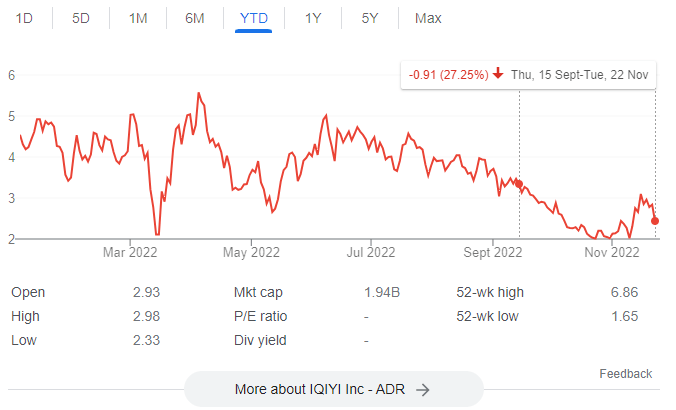

IQ’s share price has declined by 27.25% since my initial post, which is obviously not the result I was looking for, but it is not out of my expectations given the uncertainties in China.

IQ share price (Google)

Earnings review

IQ’s results were better than anticipated, with increased revenue, positive operating and net profit margins (7% operating margin), and positive free cash flow for the first time in several quarters. I’m relieved to hear this, as it shows that management is eager to see profits increase through their efforts to cut costs (note that this was one of my key thesis points).

Here is a rundown of the recent earnings:

- Revenue was down -2% to Rmb7.5 billion, but that was still 2% above projections.

- The average number of daily subscribers for membership services is now 101 million, up 2.7 million from the prior quarter, and the average revenue per paying user (ARPU) is now RMB 13.9 million per month.

- Due largely to difficult macroeconomic conditions, revenue from online advertising services dropped by 25% to RMB1.2 billion. But, in my opinion, this is much better than the 35% drop in 2Q22.

- Revenue has increased by 27% thanks to a successful collaboration with Douyin. In my opinion, this is big news because it could spur a rise in the average IQ of the population.

- The company’s non-GAAP operating profit for the quarter was RMB524.3 million, up from a loss of RMB1.1 billion in the same period a year ago.

- This is the first quarter of positive FCF and the second consecutive quarter of positive operating cash flow.

Membership revenue performing well

Paid memberships Average daily users jumped to 101 million, up 2.7 million from the previous quarter. The good news is that, for the first time in four years, September saw an increase in subscribers. This is attributable to three factors: 1) increased marketing efforts beginning in late August; 2) higher-quality premium content, especially original content; and 3) enhanced membership perks as a result of the macroeconomic recovery. In addition to an increase in volume, ARPPU rose to Rmb13.9 per month as a result of increased promotional discounts offered during the summer months.

Management has expressed optimism about the future, saying that the third-quarter result does not accurately reflect IQ’s strong growth momentum and that subscriber growth and increases in average revenue per user will be the primary drivers of the membership services business. As long as IQ maintains its focus on producing high-quality, original programming, it should see a rise in its subscriber base. I have no doubt that this is possible thanks to IQ’s novel approach to content creation, backed by skilled teams from the in-house studio, a mature and efficient full-cycle production mechanism, and an intelligent production system designed to boost both quality and productivity. On the other hand, ARPPU growth is mostly caused by two things: reducing promotional discounts and thinking about price hikes.

Online ads revenue performed better than expected in a bad environment

Due primarily to difficult macroeconomic conditions, revenue from online advertising services dropped by 25% to RMB1.2 billion. But, in my opinion, this is much better than the 35% drop in 2Q22. If you look past the headline numbers, you’ll see that brand advertising revenue, especially ad demand from international brand advertisers, improved during the most recent quarter, and performance advertising revenue increased both annually and during the most recent quarter.

Future ad revenue growth for IQ will be hampered by macro headwinds, but I expect it to pick up a bit in 4Q22 thanks to a combination of a macroeconomic uptick and the launch of some new variety shows in 2H22 that should help boost IQ’s brand advertising.

On track for more profitability and positive FCF

In comparison to a loss of Rmb1.1 billion in the same period a year ago, the company’s non-GAAP operating profit for the quarter was Rmb524.3 million. Increased efficiency in managing content costs, a 21% drop in SG&A costs, a 30% drop in R&D costs, and a 5% drop in IQ’s share of compensation costs are primarily responsible for this.

Since the company changed its strategy to “Calm Growth” in 3Q22, which will be supported by continuing cost-cutting initiatives and increased top-line contribution starting in 3Q22, management expects the trend in free cash flow (“FCF”) to continue.

For me personally, as an investor in IQ, hearing that the company will soon be generating positive cash flow is like music to my ears.

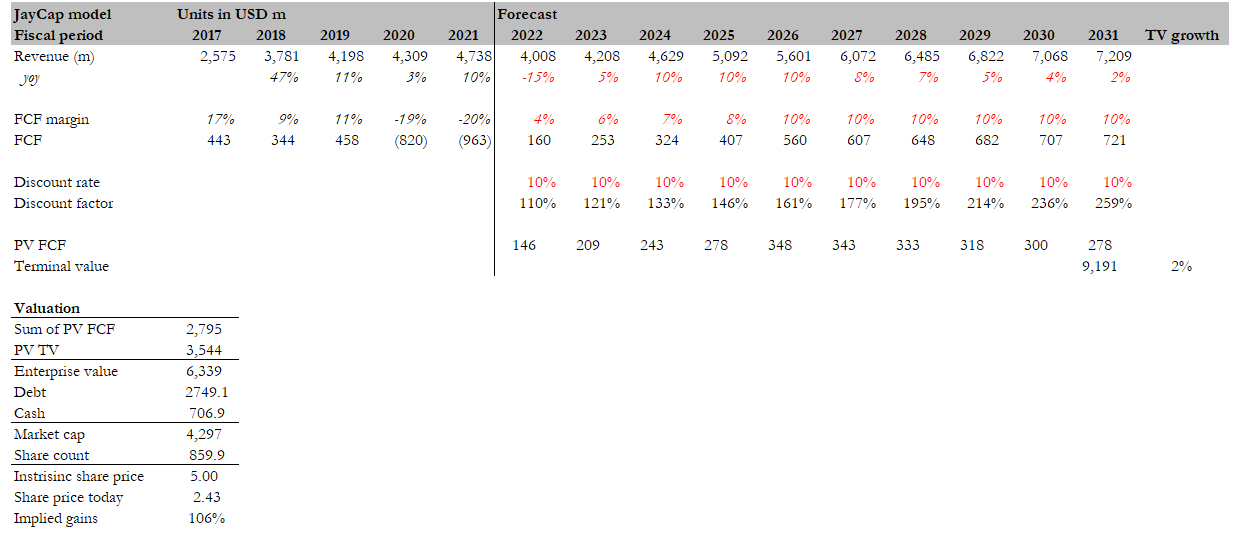

Model update

My model has been updated to better reflect FY22 revenue and to allow for the early realization of positive FCF. I still think that IQ is undervalued and that the selloff is just due to “risk-off” situations in the near future.

With my new assumptions, I believe the IQ upside remains appealing.

Author’s estimates

Conclusion

I still think that iQIYI, Inc. has a chance to go up. But I’m still worried about IQ’s subscription revenue growth because, even though the average revenue per member is going up in a pricing environment where prices aren’t too high, subscription growth is slow. With time-spent share still going to SFV platforms, regulations getting stricter, and COVID making a comeback, the timeline for ad recovery could get even longer.

Be the first to comment