martin-dm/E+ via Getty Images

A Quick Take On Structure Therapeutics

Structure Therapeutics (GPCR) has filed proposed terms to raise $125 million from the sale of American Depositary Shares representing underlying common stock in an IPO, according to an amended registration statement.

The firm is a clinical-stage biopharma developing new therapeutics for the treatment of serious chronic diseases. GPCR has significant operations in China and Australia.

The company is still at a very early stage of development and has attendant risks from its foreign operations in China and Australia.

So, I’m on Hold for the IPO.

Structure Therapeutics Overview

South San Francisco, California-based Structure Therapeutics Inc. was founded to develop G-protein-coupled receptors, called GPCR, as small molecule therapies that promise to overcome the limitations of biologics and peptide therapies that target the GPCR-family of receptors.

Management is headed by Chief Executive Officer Raymond Stevens, Ph.D., who has been with the firm since February 2019 and was previously the founder of the Bridge Institute at the University of Southern California and has been a long-time professor of Biology at The Scripps Research Institute.

The firm’s lead candidate, GSBR-1290 is being developed for the treatment of Type 2 diabetes and has initiated a Phase 1b proof-of-concept study for this form of diabetes and obesity.

Type 2 diabetes affects over 130 million Americans and is the most prevalent form of diabetes, accounting for 90-95% of cases. Additionally, GPCRs are the largest family of receptors that play a role in obesity and in the development of Type 2 diabetes.

Management expects topline data from its Phase 1b and Phase 2a study sometime in the second half of 2023.

Below is the current status of the company’s drug development pipeline:

Company Pipeline (SEC)

Structure has booked fair market value investment of $200 million as of September 30, 2022, from investors including ERVC Healthcare, F-Prime Capital Partners, Qiming, XX-I SHT Holdings, Biotechnology Value Fund, Sequoia Capital China and Deep Trach Biotechnology.

Structure’s Market & Competition

According to a 2022 market research report by Allied Market Research, the global diabetes therapeutics market was an estimated $118 billion in 2020 and is forecast to reach $318 billion by 2030.

This represents a forecast CAGR (Compound Annual Growth Rate) of CAGR of 10.4% from 2021 to 2030.

Key elements driving this expected growth are the growing incidence of diabetic conditions among an aging global population.

Also, the International Diabetes Federation reported that an estimated 537 million adults are currently living with diabetes.

That estimate is expected to reach 643 million by 2030 and 783 million by 2045.

Major competitive vendors that provide or are developing related treatments include:

-

Pfizer

-

Eli Lilly & Company

-

Qilu Regor Therapeutics

-

Jiangsu Hansoh Pharmaceutical Group

-

Boehringer Ingelheim

-

Altimmune

-

Carmot Therapeutics

-

Sciwind Biosciences

-

CohBar

-

Apie Therapeutics

-

BioAge Labs

-

Others

Structure Therapeutics’ Financial Status

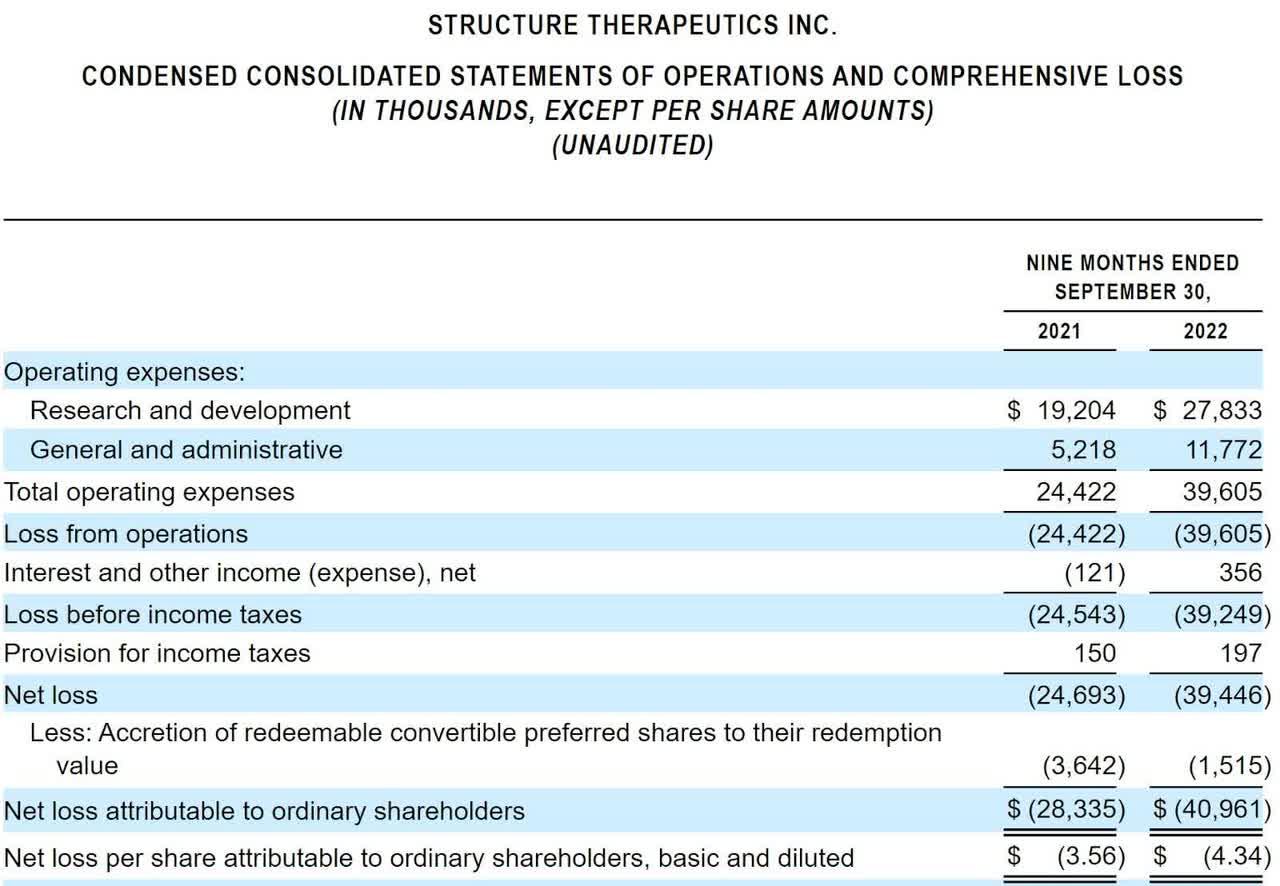

The firm’s recent financial results are typical of a clinical-stage biopharma in that they show no revenue and significant R&D and G&A costs associated with its drug development efforts.

Below are the company’s recent financial results:

Statement Of Operations (SEC)

As of September 30, 2022, the company had $28.1 million in cash and $12.3 million in total liabilities.

Structure Therapeutics IPO Details

GPCR intends to sell 8.95 million American Depositary Shares representing underlying common stock at a proposed midpoint price of $14.00 per share for gross proceeds of approximately $125.3 million, not including the sale of customary underwriter options.

No existing or potentially new shareholders have indicated an interest in purchasing shares at the IPO price.

Assuming a successful IPO at the midpoint of the proposed price range, the company’s enterprise value at IPO (excluding underwriter options) would approximate $270.8 million.

The float to outstanding shares ratio (excluding underwriter options) will be approximately 25.7%. A figure under 10% is generally considered a ‘low float’ stock which can be subject to significant price volatility.

Management says it will use the net proceeds from the IPO as follows:

to advance the development of our GLP-1R franchise, including the completion of a Phase 1b MAD study and Phase 2a proof-of-concept study, and next generation GLP-1R candidates including dual GLP-1R/GIPR agonists;

to advance the development of our [i] APJR agonist program, including through the initiation of a Phase 1 formulation bridging PK study as well as additional preclinical development studies in IPF and PAH, and [ii] LPA1R antagonist program, including preclinical development and initiation of our first-in-human study in IPF; and

the remaining proceeds to fund other research and development activities and general corporate purposes, which we expect will include the hiring of additional personnel, capital expenditures and the costs of operating as a public company.

(Source – SEC)

Management’s presentation of the company roadshow is not available.

Regarding outstanding legal proceedings, management says the firm is not subject to any material legal action or governmental investigation.

The firm has a number of wholly-owned subsidiaries in Australia ‘to conduct various preclinical and clinical activities for our product and development candidates in Australia.’

Structure also has material operations in China.

Listed bookrunners of the IPO are Jefferies, SVB Securities, Guggenheim Securities and BMO Capital Markets.

Commentary About Structure Therapeutics

GPCR is seeking U.S. public capital market funding to advance its lead and other programs through and into clinical trials.

The firm’s lead candidate, GSBR-1290 is being developed for the treatment of Type 2 diabetes and has initiated a Phase 1b proof-of-concept study for this form of diabetes and obesity.

Management expects topline data from its Phase 1b and Phase 2a study to be available in 2H 2023.

The market opportunity for treating diabetes is large and expected to grow at a reasonably high rate of growth in the coming years.

However, the industry has strong competition among major pharmaceutical firms.

Management hasn’t disclosed any major pharma firm collaboration but does have a discovery collaboration with contract manufacturer Schrödinger.

The company’s investor syndicate includes a number of institutional venture capital firms, so the firm is well-capitalized.

Jefferies is the lead underwriter and its sole IPO led by the firm over the last 12-month period has generated a return of 16.2% since its IPO. This is a mid-tier performance for all major underwriters during the period.

A potentially significant risk to the company’s outlook is the uncertain future status of Chinese company stocks in relation to the U.S. HFCA act, which requires delisting if the firm’s auditors do not make their working papers available for audit by the PCAOB.

While the firm’s current auditors have made their working papers available for audit by the PCAOB, as the company says, ‘there is no guarantee that future audit reports will be prepared by auditors subject to inspection by the PCAOB…’

Prospective investors would be well advised to consider the potential implications of specific laws regarding earnings repatriation and changing or unpredictable Chinese regulatory rulings that may affect such companies and U.S. stock listings.

As for valuation, management is asking investors to pay an enterprise value of approximately $271 million at IPO, which is at the lower end of the typical range for clinical-stage biopharmas at the time of IPO.

While the firm is backed by well-known venture capitalists and has shown promising clinical trial results, its principal location in China presents a number of risks to prospective investors, as outlined above.

Also, given its very early stage of development, it is very difficult to determine its chances of success in clinical trials ahead.

Accordingly, I’m on Hold for the IPO.

Expected IPO Pricing Date: February 2, 2023.

Be the first to comment