Edwin Tan/E+ via Getty Images

A Quick Take On Belite Bio

Belite Bio, Inc. (BLTE) intends to raise $36 million from the sale of American Depositary Shares representing its common stock in an IPO, according to an amended registration statement.

The company is developing treatment candidates for eye diseases.

While I wish BLTE well, the IPO appears to be outside the typical biopharma IPO profile for U.S. markets, so I’m on Hold for the stock.

Company & Technology

San Diego, California-based Belite was founded to develop a pipeline of treatment candidates for age-related macular degeneration and autosomal recessive Stargardt disease (STGD1).

Management is headed by founder, Chairman and CEO Dr. Yu-Hsin Lin, who has been with the firm since inception in June 2016 and was previously founder, Chairman and CEO of Lin BioScience, a major investor in the company.

The firm’s lead candidate, LBS-008, or Tinlarebant, is a once-per-day oral treatment candidate for STGD1 designed to reduce the accumulation of toxic vitamin A by-products in ocular tissue.

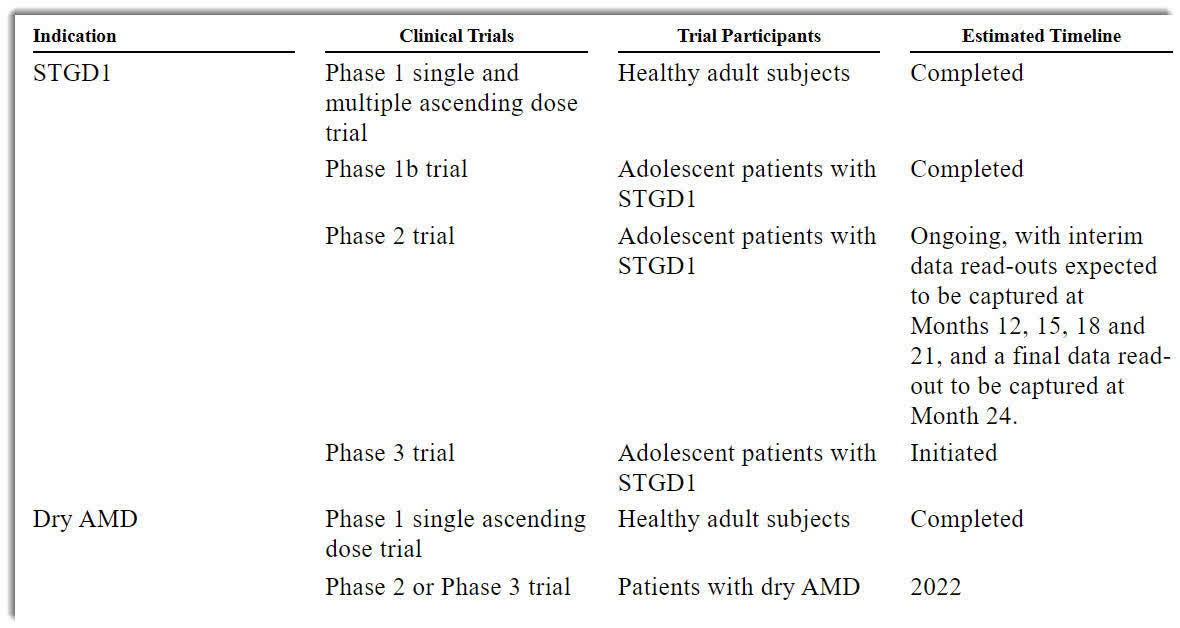

LBS-008 is currently in Phase 3 trials, with patient enrollment in Taiwan, the U.K., Hong Kong and Switzerland.

Below is the current status of the company’s drug development pipeline:

Pipeline Status (SEC EDGAR)

Belite has booked fair market value investment of $40.6 million as of December 31, 2021 from investors including Lin BioScience International Ltd.

Belite’s Market & Competition

According to a 2021 market research report by Coherent Market Insights, the global market for the treatment of Stargardt disease is expected to reach $1.7 billion in market size by 2028.

This represents a forecast CAGR (Compound Annual Growth Rate) of CAGR of 31.7% from 2020 to 2027.

Key elements driving this expected growth are an increase in the number of treatment options for patients.

Also, the current primary treatment option for Stargardt disease is Emuxistat.

Major competitive vendors that provide or are developing related treatments include:

Kubota Pharmaceutical Holdings Co., Ltd., Stargazer Pharmaceuticals Inc, Iveric Bio, Sanofi S.A., Alkeus Pharmaceuticals, Astellas Pharma, CHABiotech Co., ReVision Therapeutics, Biogen, and F. Hoffmann-La Roche AG.

Belite Bio Financial Status

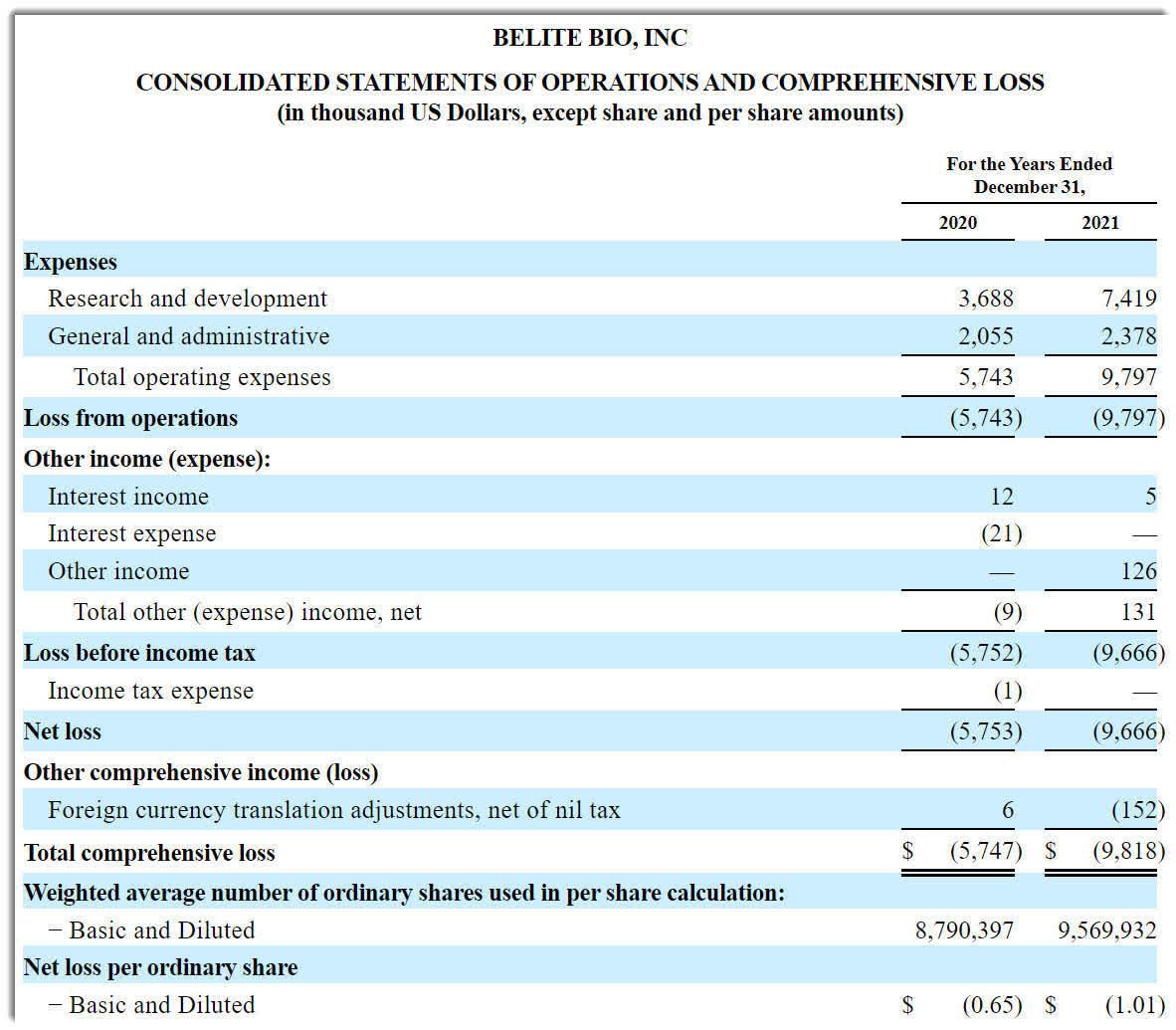

The firm’s recent financial results are typical for a clinical stage biopharma firm in that they feature no revenue and significant R&D and G&A expenses associated with its pipeline development efforts.

Below are the company’s financial results for the past two calendar years:

Statement of Operations (SEC EDGAR)

As of December 31, 2021, the company had $17.3 million in cash and $1.6 million in total liabilities.

BLTE’s IPO Details

BLTE intends to sell 6 million ADSs representing underlying ordinary shares at a proposed midpoint price of $6.00 per share for gross proceeds of approximately $36 million, not including the sale of customary underwriter options.

The firm’s existing principal shareholder, Lin Bioscience International, has indicated a non-binding interest to purchase up to $15 million in ADS.

Assuming a successful IPO at the midpoint of the proposed price range, the company’s enterprise value at IPO (excluding underwriter options) would approximate $97 million.

The float to outstanding shares ratio (excluding underwriter options) will be approximately 24.9%. A figure under 10% is generally considered a ‘low float’ stock which can be subject to significant price volatility.

Per the firm’s most recent regulatory filing, it plans to use the net proceeds as follows:

approximately 2.5% for our Phase 3 clinical trial of LBS-008 for STGD1,

approximately 68.2% for further clinical development of LBS-008 for dry AMD, such as Phase 2 or Phase 3 clinical trials, and

the remainder for working capital and other general corporate purposes.

We estimate the net proceeds of this offering would enable us to complete our ongoing Phase 2 and Phase 3 clinical trials of LBS-008 for STGD1, and to obtain interim results of our anticipated Phase 2 or Phase 3 clinical trials of LBS-008 for dry AMD.

(Source)

Management’s presentation of the company roadshow is available here until the IPO is completed.

Regarding outstanding legal proceedings, management says the firm is not currently a part of any legal proceedings that it believes would have a material adverse effect on its financial condition or operations.

The sole listed bookrunner of the IPO is The Benchmark Company.

Commentary About Belite

Belite is seeking U.S. public market capital to fund its pipeline advancement efforts.

The firm’s lead candidate is LBS-008, a once-per-day oral treatment candidate for STGC1 designed to reduce the accumulation of toxic vitamin A by-products in ocular tissue.

LBS-008 is currently in Phase 3 trials for STGD1, with patient enrollment in Taiwan, the U.K., Hong Kong and Switzerland and is also being trialed for the treatment of AMD.

The market opportunities for these treatments are large and are expected to grow significantly in the year ahead.

Management has not disclosed any major pharma firm collaborations.

The company’s investor syndicate includes primary shareholder Lin Bioscience.

The Benchmark Company is the sole underwriter and IPOs led by the firm over the last 12-month period have generated an average return of negative (35.9%) since their IPO. This is a lower-tier performance for all major underwriters during the period.

While the company does not operate within a variable interest entity or ‘VIE’ structure, it does have a subsidiary in mainland China and in Hong Kong and its ‘financial reports and other filings with the SEC may be subject to enhanced review by the SEC and this additional scrutiny could affect our ability to effectively raise capital in the United States.’

As for valuation, management is asking IPO investors to purchase ADSs at an enterprise value of around $97 million, which is far below the typical range for a clinical stage biopharma firm at IPO.

While I wish BLTE well, the IPO appears to be outside the typical biopharma IPO profile on U.S. markets, so I’m on Hold for the stock.

Be the first to comment