Olemedia

Australia-based ioneer Ltd (NASDAQ:IONR) (OTCPK:GSCCF) received some good news a couple of weeks ago when the US Department of Energy conditionally committed to a loan of up to $700 million to develop the company’s Rhyolite Ridge project in Nevada. The addition of those funds towards the construction of its lithium-boron mine means that ioneer has locked down all the capex funding needed to complete the project.

The company had also previously secured several offtake partners for most of its lithium and boron output, and it has taken many steps to placate governmental environmental concerns. Ioneer has done most of the preparation work and is now looking to soon begin construction of the project. In this article, we’ll review the Rhyolite Project and discuss ioneer’s valuation.

Company Background

Rhyolite Ridge, which is located about halfway between Reno and Las Vegas, is ioneer’s only mining property. It’s also one of only two lithium-boron deposits in the world and will be the only lithium mining operation working with Searlesite; lithium is usually extracted from brine, clay, or pegmatite bodies (hard rock).

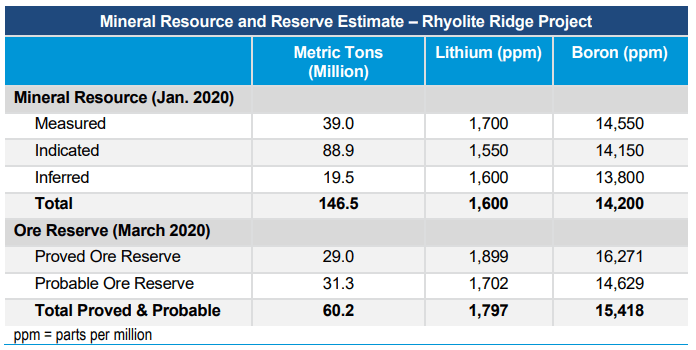

The property has an impressive Resource measuring 146Mt (M&I&I) as well as an impressive Reserve measuring 60Mt (P&P). The average grades for the lithium Ore Reserve averages ~1,800 ppm while Boron comes in at just under 15,500 ppm.

Ioneer DFS

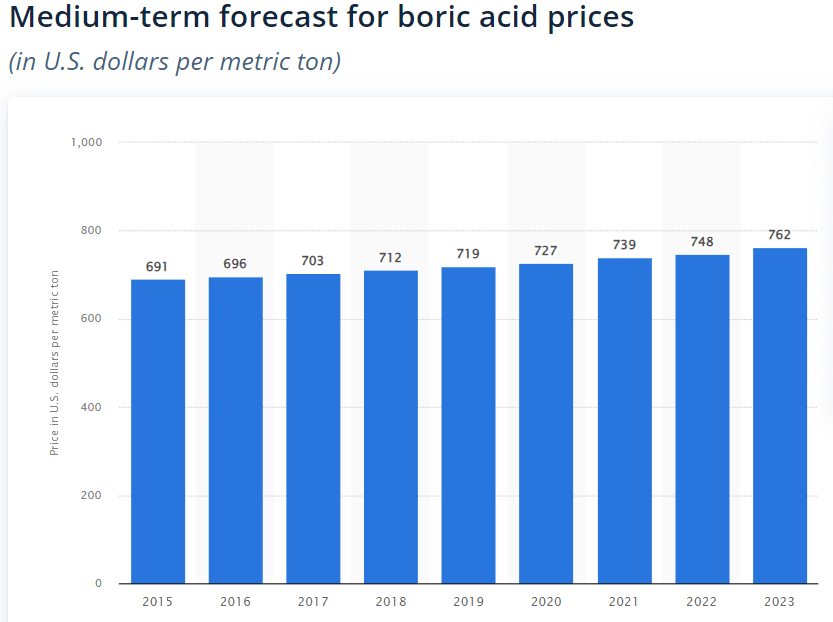

Ioneer published a Definitive Feasibility Study (‘DFS’) back in April 2020 stating that it intends to produce over 22ktpa of lithium carbonate for the first three years of the project. During that time, the company intends to build a hydroxide conversion facility that will replace the carbonate with 22ktpa of hydroxide beginning in year 4. The mine will have a 26-year lifespan, and during that entire period will also be producing 174ktpa of boric acid. Lithium is clearly the headliner on this project, but Boron sales will provide a substantial kicker; however, we should remember that boric acid prices have barely budged in decades, so we shouldn’t expect surging Boron prices to drive this stock to the moon.

Statista.com

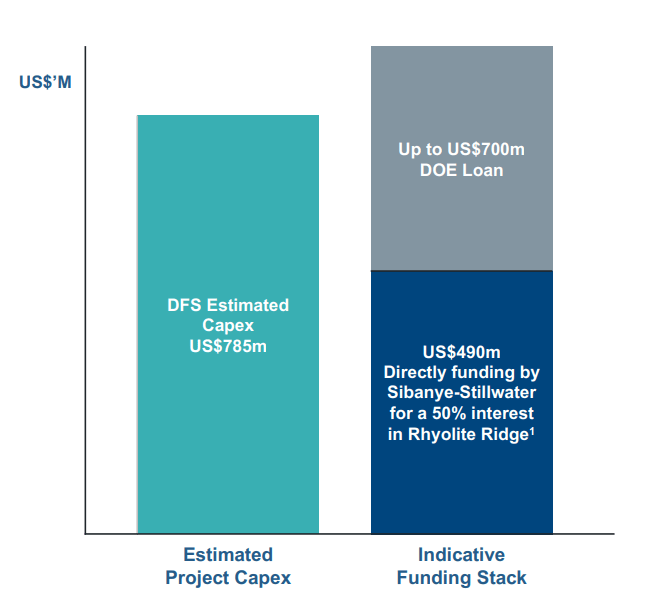

The lithium component of the project is what opened the door to government financing. And although final approval of the loan is still subject to multiple conditions, such as successful permitting and continued observance of environmental regulations, the outlook is good. If and when ioneer does receives those funds, the cash will be combined with $490 million of funding to be contributed by the South African miner Sibanye Stillwater Limited (SBSW). That’s because ioneer has a deal that will see the South African company provide almost two-thirds of Rhyolite’s $785 million CapEx cost in exchange for a 50% interest in the project.

Ioneer’s Capex Funding (Investor Presentation)

Deals such as these have their advantages and disadvantages with the obvious disadvantage being that ioneer had to give up half the project. However, bringing in Sibanye did allow ioneer to raise a substantial amount of the project’s required capital quickly and in a manner that didn’t require it to continually raise cash through multiple rounds of dilutive equity offerings. Locking down such a large tranche of the project’s capex requirements also allows construction to start that much sooner.

That’s good news because once the project is completed, it’s expected to generate some pretty decent returns. The DFS, which assumed all-in sustaining costs of $2,510/t, listed an after-tax NPV8% and IRR of $1.26 billion and 20.8%, respectively. The project’s lifetime revenue was estimated to be $10.7 billion while it’s lifetime EBITDA came in at $7.3 billion, or $288 million per year.

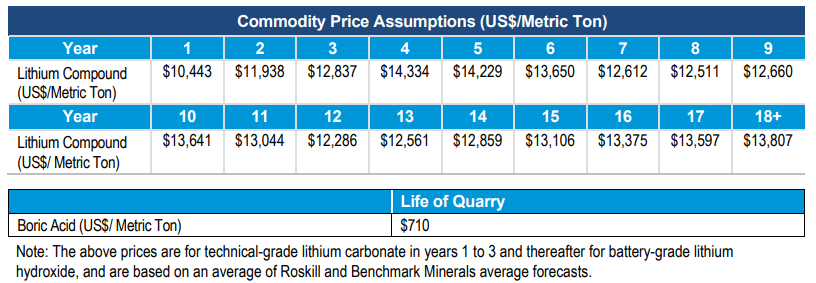

However, those calculations are based on relatively conservative price assumptions for both carbonate and hydroxide which can be seen in the exhibit below. The average carbonate price assumption used in the DFS was $11,740/t while the average hydroxide price was $13,423/t; meanwhile, the boric acid price assumption of $710/t seems quite reasonable.

Ioneer DFS

The reason for these seemingly conservative assumptions stems from the fact that the DFS was published in April of 2020, back when lithium was trading at much lower price points. Needless to say, if lithium prices remain at today’s levels by the time the project starts production, the NPV and IRR calculations will have to be revised upwards.

Project Progression

Construction at Rhyolite Ridge has not yet begun, but that should soon change. Management has stated that it intends to take a Final Investment Decision in the first half of calendar year 2023. Construction would start soon afterwards and is projected to take 24 months. Completion of the build out is targeted for the first half of calendar year 2025, which is also when first production would occur; that would be followed by a gradual ramp to full production over a 6-month period.

A lot of the groundwork has already been done. On the environmental side, ioneer has invested significant amounts to protect Tiehm’s buckwheat, an endangered plant that grows in the area.

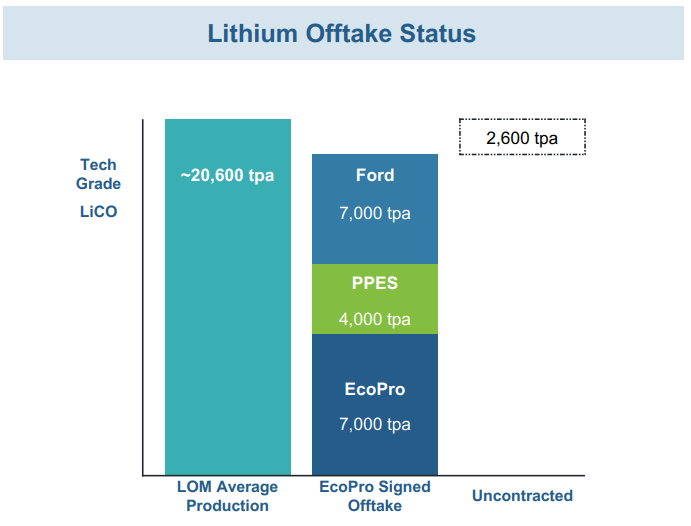

It has secured lithium carbonate offtake with EcoPro Group, a Korean battery manufacturer, for 7ktpa; a binding 5-year contract with The Ford Motor Company (F) for another 7ktpa; and a binding agreement with Prime Planet Energy & Solutions, Inc., a JV between Toyota Motor Corporation (TM) and Panasonic Holdings Corporation (OTCPK:PCRFY), for 4ktpa.

Ioneer Offtake Partners (Investor Presentation)

As far as the Boron goes, the company has secured offtake through agreements with Dalian Jinma Boron Technology Group Co. Ltd, Kintamani Resources Pte Limited, and Boron Bazar Limited. These agreements will cover 100% of first-year production and over 85% of production in years two and three.

And while ioneer must still secure several more minor federal, state, and local permits, it’s in the process of obtaining the final key permit necessary to start construction, that being the Environmental Impact Statement and Record of Decision.

Valuation

The company currently trades at a market cap of about $700 million and has about $77 million of cash on its balance sheet. Ioneer has no debt, but that will change once the $295 million government loan is issued (Assuming they only borrow enough to cover their capex needs). We can therefore put its Enterprise Value at about $918 million, or about 73% of its NPV.

However, we have to remember that the $1.26 billion NPV was calculated using a carbonate price assumption of only $11,740/t, or about one-sixth of carbonate’s current price of ~70k/t. As lithium prices continue to hold up and as demand continues to strengthen, that price assumption is beginning to look a little overly conservative; but by the same token, assuming that carbonate’s price will continue to trade at over $70k/t for years and decades into the future may be a little overly ambitious. We’ll therefore use a $35k/t price assumption, or a tripling of the NPV price assumption; that would put the adjusted NPV at about $3.8 billion.

But we also have to factor in that ioneer will only receive half of that NPV, given that Sibanye will take a 50% share of the project. This puts ioneer’s share of the adjusted NPV at about $1.9 billion or just over double the $918 million Enterprise Value listed above.

Takeaway

Taking all of this into account, ioneer appears to be fully valued at these prices. We have to remember that the analysis above doesn’t adjust construction costs for the current higher rates of inflation, and it also assumes the build gets done on budget and on schedule, a rarity in the mining world. Although ioneer’s project is promising and the company has had a lot of good news to report, the stock at these prices does not have enough potential upside.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment