Author’s Note: This article was published on iREIT on Alpha in late January of 2023.

StefaNikolic/E+ via Getty Images

Dear subscribers,

Investing in various types of “home” REITs is something I’m quite fond of. The combination we can get of fulfilling a very basic need coupled with very attractive and relatively timeless (mostly) assets is in many ways far more appealing than less recession-resistant sub-segments in the REIT sector. When I started reading up on Invitation Homes (NYSE:INVH) a few weeks ago, I knew very early on that I would be investing in the company – and slowly starting to build a position.

Now why is that?

Let me show you in this article, where we go through why INVH is a solid “BUY” here on IREIT and why we cover the company at this time.

Invitation Homes – initiating coverage

So, Invitation Homes – what is it? The company prides itself on being the nation’s “premier single family home leasing business”, with a focus on what they call resident experience. Math is far more interesting than verbiage or colorful language, of course, and when I saw the numbers in this company, I became more interested.

INVH has an average 3Q22 occupancy of over 97%, a blended growth rate of over 10%, the same with renewal rate growth, and a new lease rate of 9.6%. Those are not just solid foundational numbers, but solid growth numbers as well.

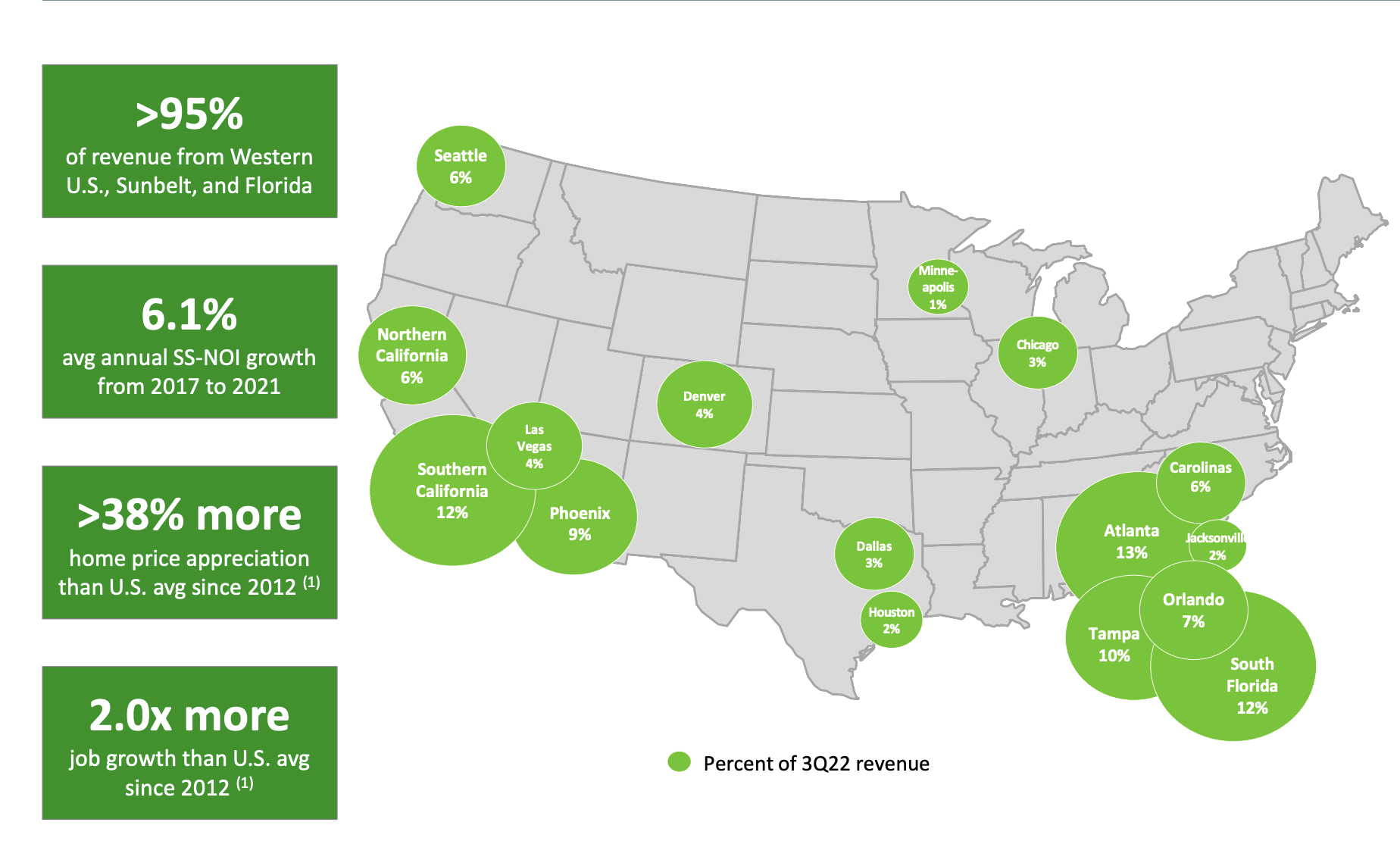

Unlike some of the home leasing REITs I’ve written about earlier, the company’s exposure is not just west or east-coast, but growth areas, such as Dallas, Nevada, Arizona, Florida, the Carolinas, and areas like Chicago and Minneapolis.

INVH IR (INVH IR)

You know I’m not as negative on the west coast as some investors are – but I like to see a diversification away from the perhaps riskier north coasts both on the east and west sides of the nation, and the company is slowly doing that.

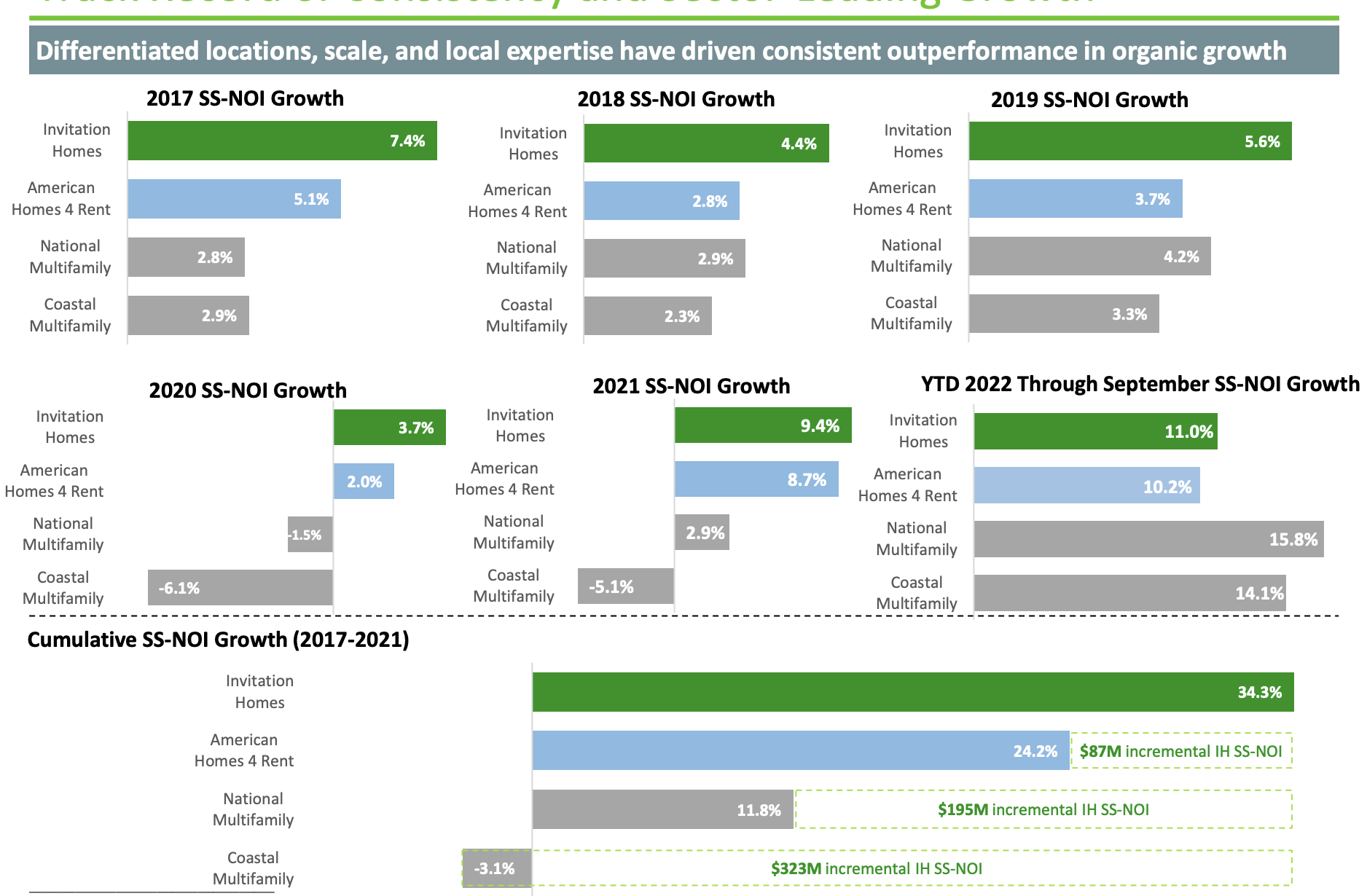

The company has a very solid history. What I say by this is that Invitation Homes have outperformed the sector average for several years at this point, in the metric of same-store NOI growth. What impresses me the most is the degree of outperformance during COVID-19. Take a look at some of these numbers the company is reporting.

INVH IR (INVH IR)

What we’re seeing here is a track record of experience and expertise, coupled with very good diversification. The company focuses on the main differentiating factors for real estate namely – location (location, location), scale, and expertise. INVH has 20 in-house investment professionals with various market expertise and 1,000 operations personnel across multiple markets. They combine this with in-house control of the resident experience. In terms of scale, the company has 5,200 per market, and 98% of the company’s revenues come from markets with over 1,900 homes. INVH focuses on markets with:

- In-fill neighborhoods

- High barriers to homeownership

- Good growth prospects

Because I have some personal experience in this, investing in infill locations. Infill locations in real estate are development sites that exist within a mostly built-out market, which means the potential for competition is relatively limited.

The company’s resident statistics are also extremely attractive. The typical INVH resident has an annual income of over $135k, with an average income-to-rent ratio of 5.3x, and this as of 3Q22, with an average resident turnover of 21.3%, which for TTM remains low. The average tenure of a resident in INVH is 32 months.

In every INVH market, it’s more affordable to lease compared to owning the home going by today’s interest rates, with savings of over 20% as of 3Q22 data.

Fundamentally speaking, INVH has a very solid balance sheet with plenty of liquidity as of September, and no debt maturing before 2025. The absolute majority of company debt is unsecured and either at fixed or swapped-to-fixed rates.

Overall fundamentals of the markets where the company operates are expected to remain very favorable, especially with the millennial age just reaching the average resident age, which for INVH is around 39 years old. The company also believes that its portfolio of single-family rental homes with shorter-duration leases provides an effective hedge in an inflationary environment.

The company also has excellent relationships with homebuilders and other players in the market – such as participating in municipal and county auctions, sale-leaseback deals, and partnerships with builders to make sure new build supply in targeted neighborhoods is allocated to INVH.

INVH IR (INVH IR)

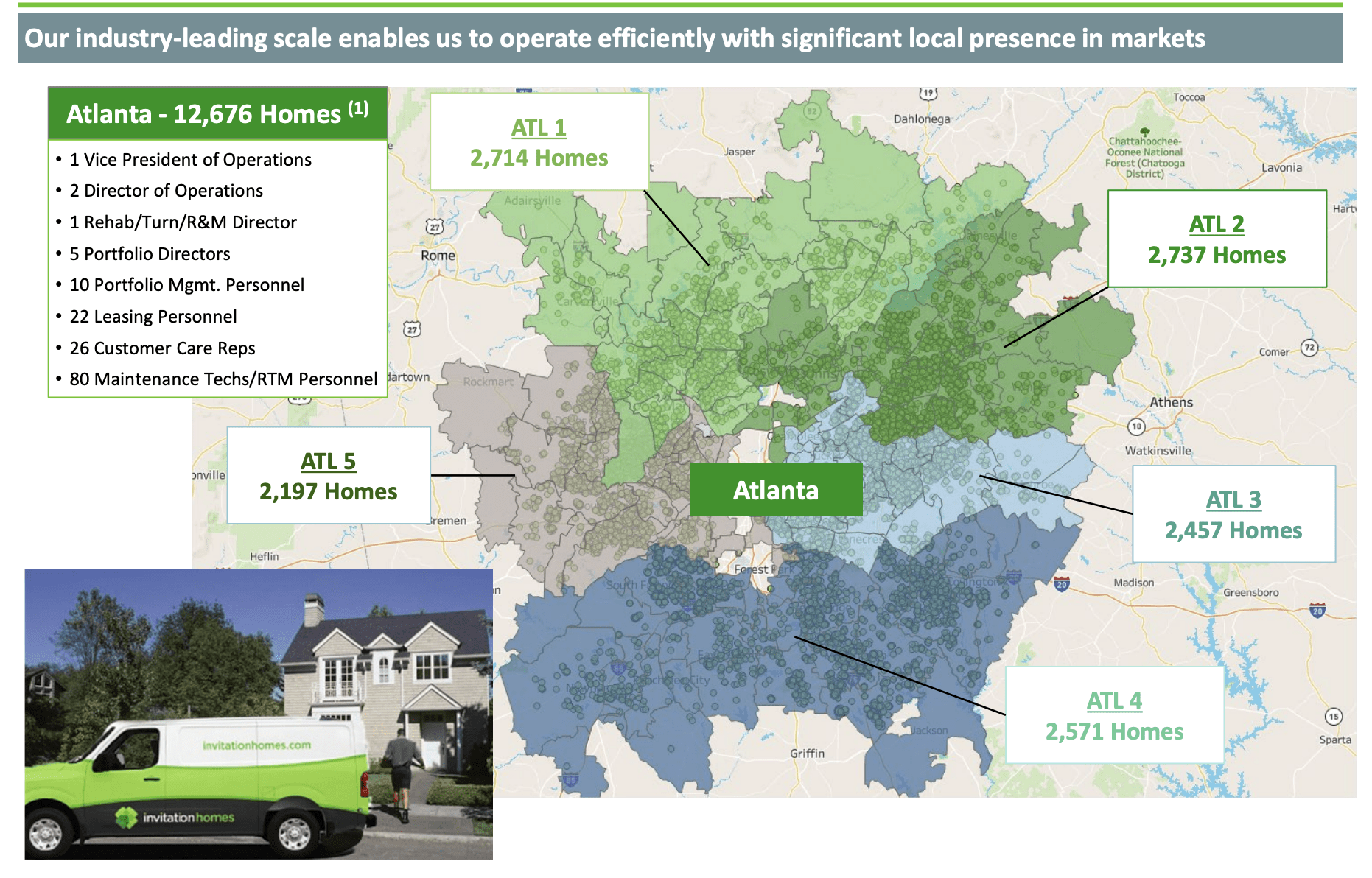

We can also showcase examples of the company’s scale in specific areas. INVH focuses on cities and neighborhoods and makes sure that they own homes to a degree that makes scale and efficiency worth it. Here are the company’s properties in Atlanta.

INVH IR (INVH IR)

The company is also growing its ancillary service segment, including things like smart home updates, HVAC filter program updates, and other things, which further increases the company’s import to its residents. Obviously, home ownership is the dream for most families – but there are many reasons and situations why/for which this may be less ideal than renting, but you may still want a single-family home. This is what INVH targets – and they do it well.

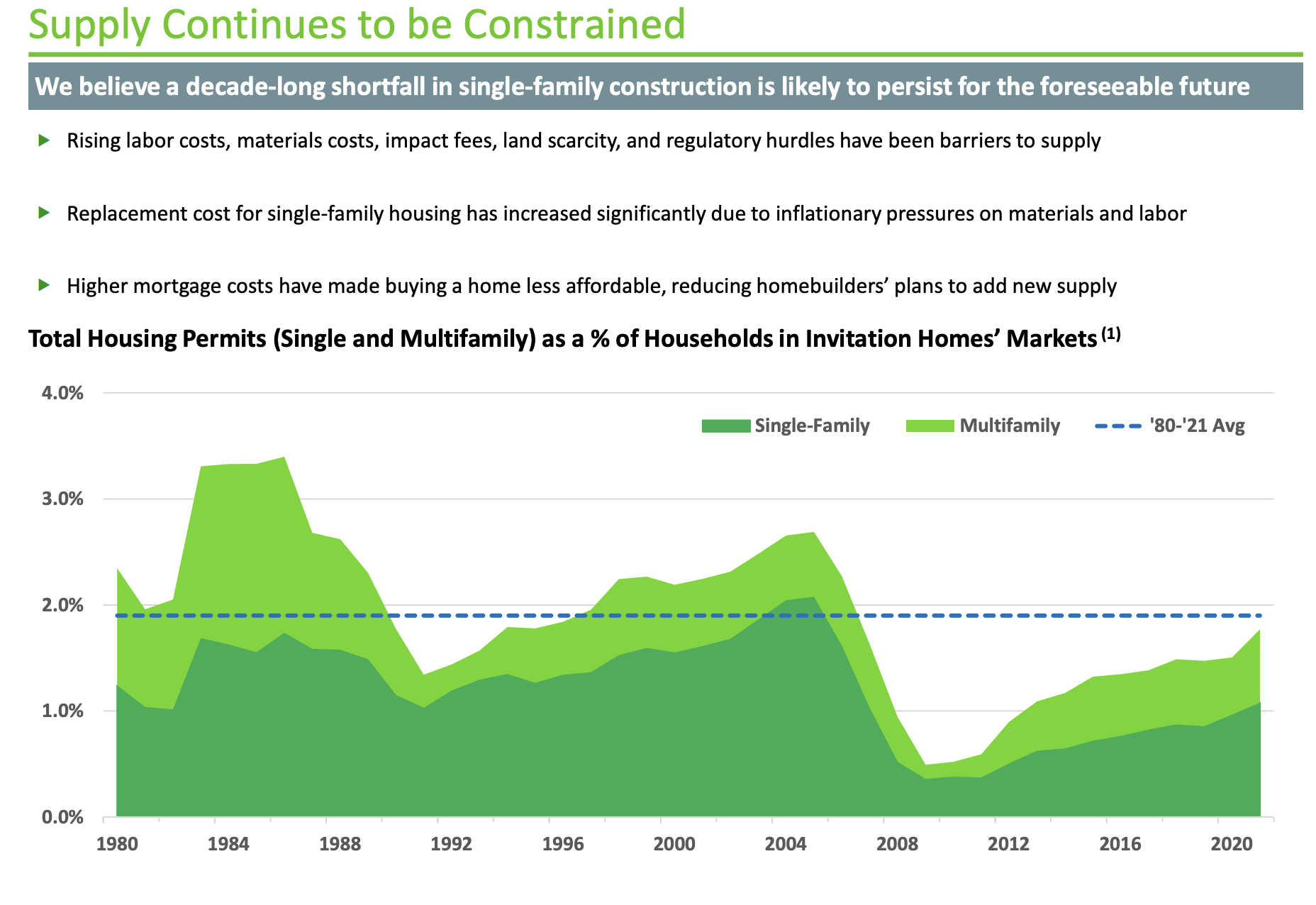

You know by now, if you follow the work on iREIT, that US housing is in an attractive situation for companies like this. Out of 130 million households (35% rented), single-unit rentals are 36%, or 16M units – and this goes very well with the potential future demand in relation to resident age. There is a time in a resident’s life, when you may want single-unit rentals as opposed to 10+ or 2-9 unit rentals (a house, in simple terms) – and the supply for new housing here is likely to continue to be constrained rather significantly.

INVH IR (INVH IR)

INVH is a relatively new listing. The company has only been around on the market for about 4-5 years. Its rating is investment-grade, but it’s a BBB-, which takes away some of that shine. The company’s yield can also be said to be somewhat sub-par, at around 2.74%.

However, where the company shines further is, I believe, growth prospects. The fundamentals of the housing market dictate that the possibilities for growth in supply are limited. Further, with the spread in homeownership cost in relation to leasing – and I believe this to be relatively unlikely to change in the near term, we’re going to see companies like these continue to do.

Yes, management did lower near-term guidance, but only by a few cents, and the overall goal here is around or just below double-digit growth in FFO and same-store NOI. This is a compelling longer-term thesis, given the conservative manner this market develops, and the underlying safety that these companies do operate with.

Invitation Homes – the valuation

Now, the clincher here is if you believe that the company is worth a premium despite the BBB- and the relatively low yield, and the somewhat-less-than-proven 100% growth “guarantees”. Nothing is guaranteed of course, as such, but I believe it fair to say that residential REITs have a somewhat higher degree of safety than other types of REITs – indeed than most others, perhaps with the exception of triple-net.

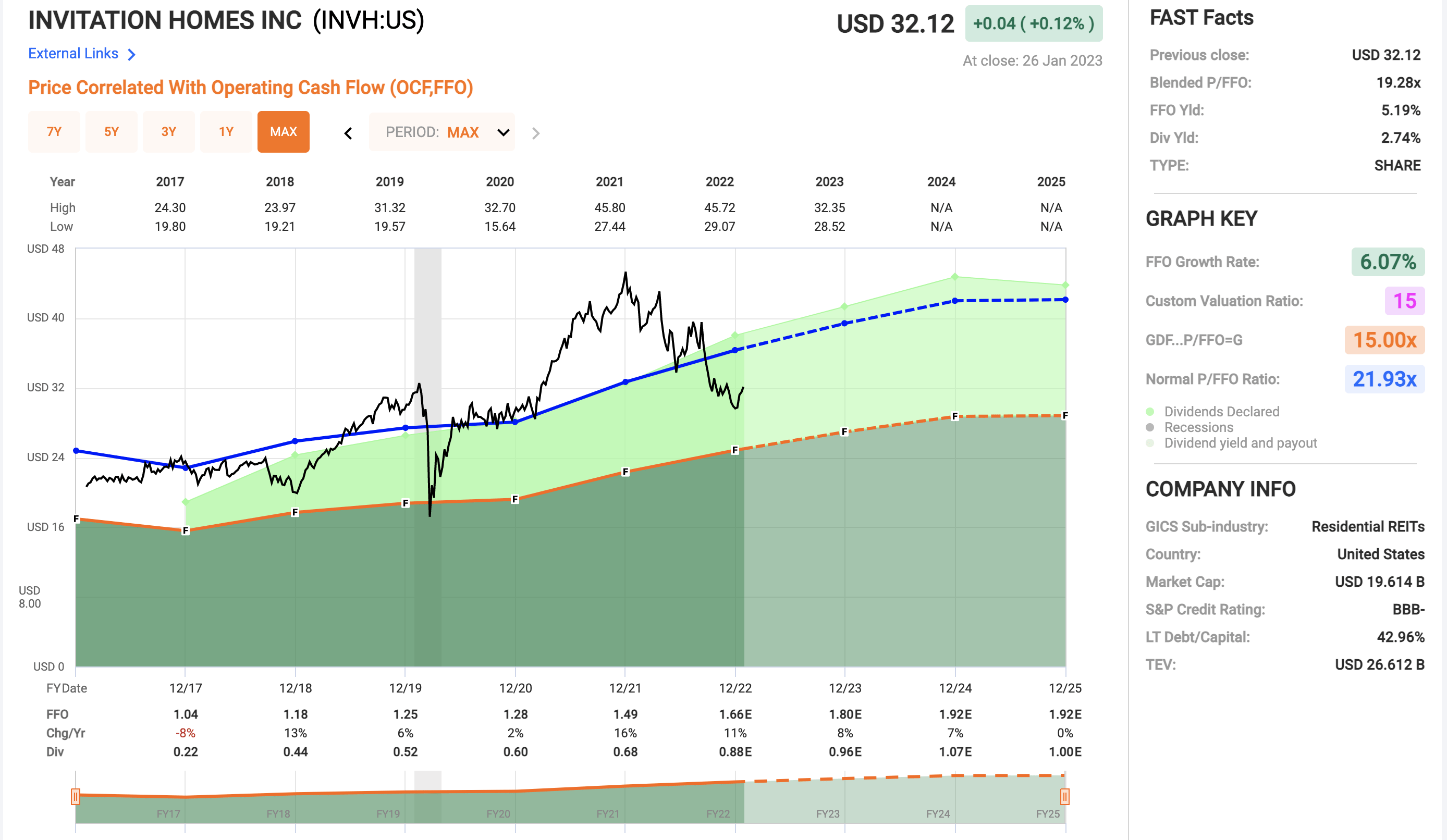

Here is how the company has traded since just before 2017.

Invitation Homes Valuation (F.A.S.T graphs)

So, if you consider a premium valid, this company isn’t that unattractively valued here – which is by the way also why we have a solid “BUY” recommendation, even a “Strong BUY” as it happens, with an overall PT of $36, representing the full premium normalized at over 20x P/FFO.

The two only challenges with INVH is the modest credit rating and the company’s relatively limited public history, though this can be an advantage as well if you managed to pick up the company before valuation settled into the levels we saw today.

While INVH has traded below 15x P/FFO once before, that was during the worst of COVID-19, and it did not last long. I wouldn’t have touched it above 23x P/FFO, but now that it’s below 20x P/FFO, I’m starting to be interested and considering this company a pretty decent “BUY”.

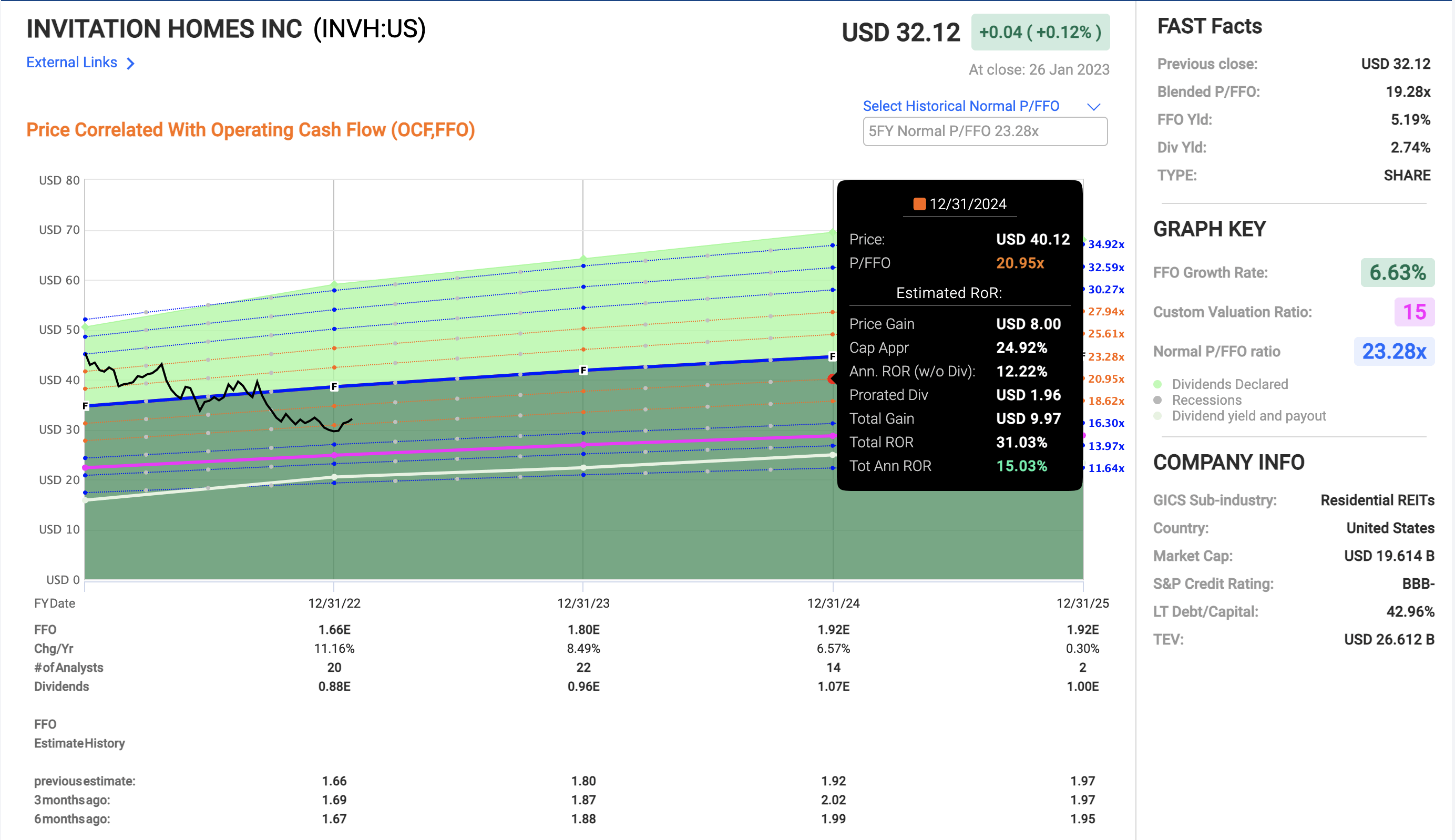

Frankly, INVH won’t make you rich. I don’t believe that’s the point of an investment like this, where you’re putting money to work in residential with a low, sub-3% yield, even with that double-digit growth rate.

But you can generate a very appealing combination of safety and profit here, by buying INVH – which is set to generate conservative returns in the double digits even if we only consider 19-21x to be valid here.

INVH Upside (F.A.S.T graphs)

The company has very few REIT peers – at least ones that we cover and that are publicly traded. The only one that can come up is American Homes 4 Rent, and that one is considered a Spec Buy with a significantly lower overall upside than INVH. Its P/FFO is significantly higher, it’s yield lower, and it’s market cap is smaller. That is not to say that AMH is a bad company – it has better credit at BBB, for instance, but based on valuation, I would favor INVH over AMH at this time from a peer perspective.

Invitation Homes are otherwise, a very well-covered and analyzed company. Over 20 analysts follow the company, and while their targets have mostly been off, they do update them in intervals. The current target range goes from a low of $30 to a high of $40, coming to an overall average of $35.5, which would suggest an upside of around 10.4%. The price that we’re seeing also represents a 0.89x to NAV, which isn’t something I consider valid for a company with these sorts of assets, which are relatively easier to value next to say, industrial or office properties.

These targets also mean that 14 analysts out of 22 have either a “BUY” or outperform rating on the stuck at this time. In terms of forecast accuracy for the limited period of time that we do have, that is so-so. With a 14% negative miss ratio, the analysts aren’t as flawless as I would like them to be with a company like this – but many of those misses were early on in 2014 and 2015 when the company was new. Data from FactSet goes back to 2013 – after 2015, there hasn’t been a single miss of more than 8% negatively in terms of the company’s FFO.

So, I think it’s fair to characterize Invitation Homes as a REIT that’s growing and expanding, and relatively new (compared to other multi-family and other REITs) on the market. This provides us the opportunity to invest in a very conservative set of assets – should we choose to do so – at a good price.

I argue that the combination of the tailwinds from the housing industry, the macro, the geographical areas where the REIT is working, and the way this REIT does business. I could go on more about the demographic trends and the way the company is structured or where its markets are – but I’m a firm believer in giving the hard data, and then going into what makes the company a good investment.

So – Invitation Homes is a good investment because it combines undervaluation, attractive growth potential, and good fundamental tailwinds with a superb operating model.

INVH IR (INVH IR)

If I were in the market for a US-based home, I would more look at properties from the AvalonBay (AVB) or Essex (ESS) segment of things, but if I had a family or the circumstances where I wanted a single-family sort of home, then Invitation Homes would be an excellent choice – and that’s just as a customer.

Despite the BBB-, I don’t see any immediate worries for the business. Funding is secured maturities are not worrying, and this company has pricing and market power in its chosen markets to do what it does efficiently and positively. If anyone here is able to find a serious, fundamental risk to this company in the near, medium, or long-term, I’d be very curious to hear it.

Because while this company won’t, as I said, make you rich, I see no reason why it shouldn’t protect and grow your capital in a slow and steady manner. And such companies always have a spot in my portfolio.

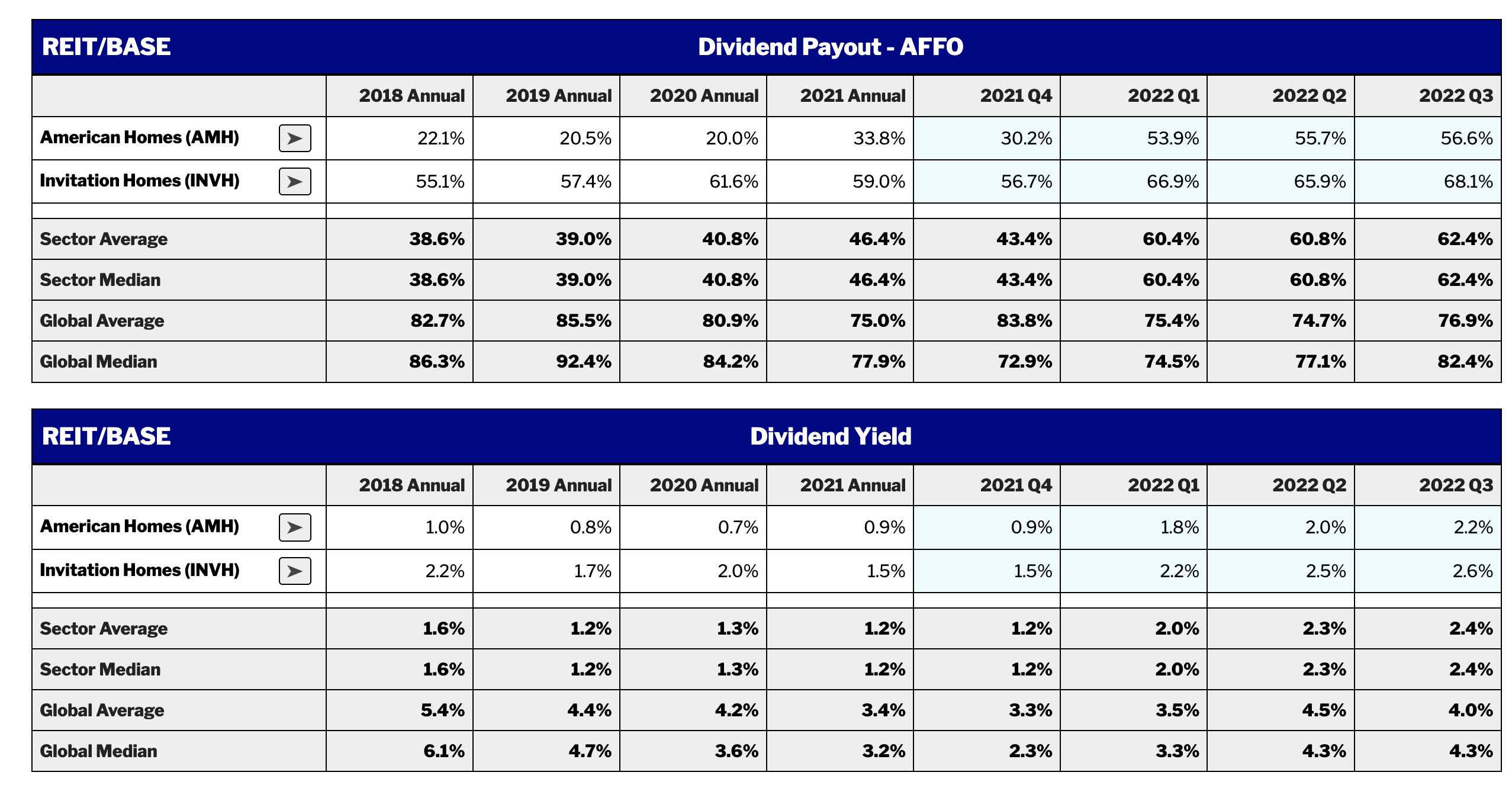

It’s a small sector of public REITs as I said – 2. But INVH beats AMH in almost every sector, except that it has more debt and lower interest/fixed charge coverage -though still not at any worrying level. INVH is at 3.6x, AMH is at 3.1x. For EBITDA, it’s at an interest coverage of 4.2x, AMH at 5.2x. INVH has 4% more debt in terms of debt/Book, but around the same net debt/EBITDA as AMH does. AFFO payout ratios are sold, and dividend yields are similar – where INVH clearly wins in size, yield, and capital because it’s almost double AMH.

REIT/Base Data (REIT/Base)

I view this company as a solid “BUY” here, even if it’s not one of the cheapest REITs currently available. However, It’s a company I consider worth the following thesis.

Thesis

- Invitation Homes is one of two publicly traded REITs in the very attractive sector of single-family. They manage a portfolio that stretches across multiple states and have proven an ability to outperform the broader market, as well as peers over time.

- The company doesn’t have the best yield or the best credit rating – but it makes up for it with solid growth estimates and conservative business practices, with levers to pull for future growth.

- I consider this company a “Buy” and would give it a PT of $35/share. The iREIT target here is $36/share, and this implies an upside of at least 15% here.

I’ll be buying INVH for my portfolio.

Questions? Let me know!

Be the first to comment