miniseries/E+ via Getty Images

Many behaviors prevalent during the height of the COVID-19 pandemic in 2020 are now experiencing a mean reversion. U.S. air travel in 2020, for example, dropped 60% as wary travelers hunkered down in their homes or opted for greater travel by road.

The dramatic drop in demand at the time instilled doubt in some regarding the future of the industry. Travel demand, nevertheless, roared back in 2022 as pent-up demand led many to take to the skies, despite soaring inflation.

Likewise, e-commerce took off in 2020 and reached a high of 18.8% of all retail shopping. This sent shares of many retail-focused real estate investment trusts (“REITs”) to record lows. Simon Property Group (SPG), for example, collapsed to share price lows in the $50/share range.

The stock has since gained back over 100% of their lows and has been steadily restoring their dividend payout. This has come at the expense of e-commerce, which has seen its share of total retail sales fall to 16.4%.

EPR Properties (EPR) is another REIT whose existence was called into question in 2020 due to their outsized exposure to movie theatres. Yet demand eventually returned in 2022 following several blockbuster hits that were, simply, best seen in a theatre. While the stock was down significantly in 2022, it is still well above its pandemic lows.

As normalcy returns, the office sector is one of the last remaining holdouts. YTD, occupancy levels are still slumping. Indeed, the industry faces secular risks resulting from the increased permanency of hybrid working arrangements, but these risks appear to be overly baked into the overall sector.

Despite improving occupancy levels and positive leasing activity, many components are trading at or below multiples commanded during the worst months of 2020. For investors seeking both high yielding dividend income and material upside potential, office REITs offer some of the greatest risk/reward propositions.

Current State Of Offices

The current outlook for offices doesn’t appear to be good. Companies are continuing to downsize their spacing needs as they increasingly adopt hybrid working arrangements.

Meta Platforms (META) is one company that has announced plans to shrink their number of offices. And there is a long list of other companies across various industries that have publicly announced downsizing plans.

Among these companies are global audit and consulting firm, KPMG, who recently announced that they would be shrinking their New York office space by 40%. Lyft, Inc (LYFT), meanwhile, said that they will sublease a significant part of their biggest U.S. offices. Even Exxon Mobil (XOM) is considering leasing or selling unused office space after finding that on a typical day it uses less than 50% of available space in their Houston-area campus.

The list of companies parting with their offices only goes on. And while this is certainly headline worthy, it’s also worth noting that overall occupancy levels continue to tick higher, albeit at a pace that is currently slower than desired.

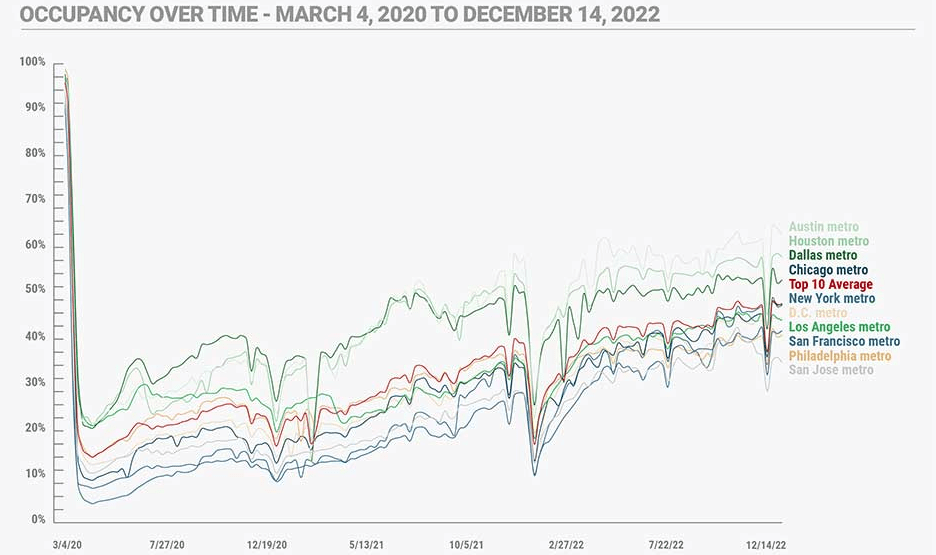

Kastle Systems – Physical Occupancy Trends In Tracked Markets From 2020 Through 2022

Most recently, average occupancy in 10 cities tracked by Kastle Systems was 48.2%. This is down 20 basis points (“bps”) from the prior week of tracking, most likely due to lighter staffing ahead of the long year-end holiday season. In addition, levels are down from their recent peak of 49% on November 30. And this, again, could be due to greater time off due to vacations or employee illness.

Still, occupancy levels are currently hovering at their highest levels since late March-2020. Furthermore, some cities, particularly in the Sunbelt region of the U.S., continue to see stronger return rates.

In Austin, Texas, for example, current occupancy levels are at 65.1%. This is up 140 bps from the prior reporting period. Two other cities in Texas, Dallas and Houston, are also reporting stronger occupancy rates, at 59.6% and 53%, respectively.

In addition, Chicago reported an occupancy rate of 48.5%, which is notable because it’s the first time since the start of the pandemic that the city’s occupancy level rose above the 10-city average.

While sub-50% occupancy levels aren’t particularly encouraging, the trend higher is. And it’s also important to note that some sectors are returning faster than others. Occupancy in law firms, for example, currently stands at 64.4%.

This is well above the average of all other industries. Even in lower occupied cities, such as Chicago, legal occupancy is at 69.2%, which is essentially even with the 69.8% occupancy rate of law firms in Houston.

Employers Want Their Employees Back

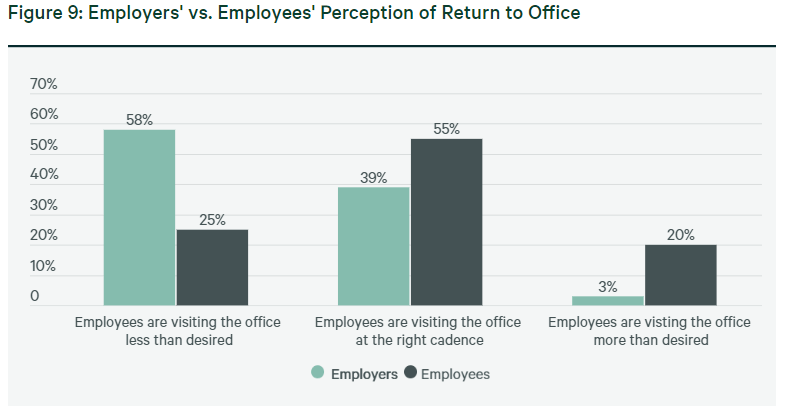

Aside from the positive trends in physical occupancy levels, there is a growing disconnect in the perception between employers and employees on time spent in the office. While over half of employees feel they are visiting the office at appropriate rates, according to a recent survey by CBRE, just 40% of employers feel the same way. The contrast is even starker when assessing perceptions on whether employees are spending too little time in the office, with nearly 60% of employers responding in the affirmative.

CBRE – 2023 Real Estate Market Outlook – Office Sector

Fresh into the new year, this disconnect has resulted in some companies taking a harder line approach to in-person work, according to a recent report in The Wall Street Journal, citing memos from investment firm Vanguard Group.

If physical occupancy levels continue to increase through the year, the sector at-large could be due for a sizeable reassessment, resulting in yield compression on many quality names who are trading at historically low valuations.

High Yielding Office Pick# 1: Piedmont Office Realty Trust (PDM)

PDM has an operating presence in seven primary markets, 24 of which are in Atlanta, Georgia and Dallas, Texas. These are two top markets in the country for inbound migration and employment growth, with solid return rates for in-person work.

The company’s YTD performance in 2022 reflects the robust continuing demand for quality office space in the region. Through nine months of the year, PDM has completed over 1.7M square feet (“SF”) of leasing at cash spreads that are higher now than they were in 2019. In addition, these signings are coming in at terms of over five years.

And with portfolio rents 5-10% below market rates, the company has ample room for further rate increases in future periods. Furthermore, their most recent trophy acquisition that is 95% leased with a remaining term of over seven years has in-place rents that are 20% below market. Moving forward, this property itself is likely to be a key driver of future earnings growth.

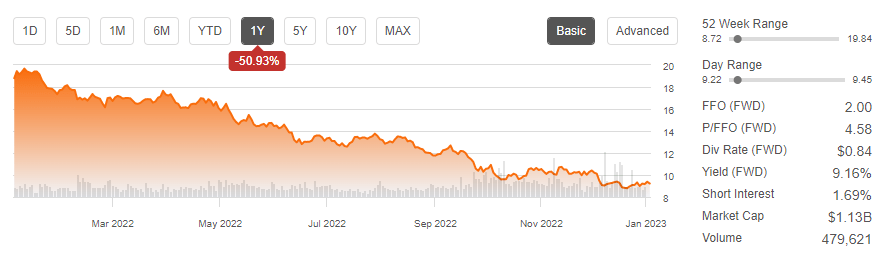

Despite the positive activity during the year, shares are down about 50% over the past year and are trading at a significantly discounted valuation. The company, as such, is a personal top pick for 2023.

Seeking Alpha – PDM Basic Trading Data

For income investors, the current payout yields over 9% at current pricing and is backed by solid coverage levels and a conservatively positioned balance sheet with ample liquidity.

High Yielding Office Pick# 2: Highwoods Properties, Inc (HIW)

HIW’s operations are concentrated in what is characterized as the best business districts (“BBDs”) in the country. Similar to PDM, these districts are heavily weighted toward the Sunbelt region of the country. More specifically, Raleigh, Nashville, Atlanta, and Tampa account for the majority share of their total net operating income (“NOI”), at about 75% of the total.

These four regions all have benefitted from favorable economic tailwinds and state rankings. North Carolina, for example, was ranked as the top state for business, according to CNBC’s annual 2022 survey.

In addition to a strong operating presence in key market regions, HIW also serves a diversified group of tenants that operate in sectors that are generally more centered on in-person work. Their top three tenants, for example, are Bank of America (BOA), Asurion, and the U.S. Federal Government.

With a current dividend yield of just above 7%, HIW’s payout is less attractive than that offered by PDM. But the lower payout is compensated by their strong track record of continuous increases. Over the past five-years, the payout has grown at a compound rate of about 2.6%.

While that may not sound impressive, it is a better record than many other components within the office sector. The dividend streak also lends credence to the company’s financial positioning and stability of their reoccurring cash flows.

Takeaway

The office sector is heavily beaten down with numerous components trading at multi-year lows. With physical occupancy levels still hovering around 50%, the underperformance is perhaps warranted. But the extent of investor flight away from the industry appears to be overdone.

Though down, physical occupancy levels are continuing to improve. And many top tier companies with interests in Class A properties are still posting robust leasing figures on a quarterly basis with positive terms on both new and renewed signings. PDM and HIW are two such companies whose share price performance is disconnected with their operating activity.

Another disconnect is the perception between employees and employers regarding time spent in the office. As one would naturally expect, employees generally believe they are spending enough time in the office while their employers feel differently.

With the onset of the new year, some employers have begun taking a harder line approach on in-person requirements. If others take up the trend, the office sector at-large could be due for a sizeable reassessment higher.

This is not to say that offices aren’t at risk of closure. On the contrary, many offices are likely to succumb to the effects of the current glut of space. This will, however, be more pronounced with the lower tier offices as opposed to the Class A properties held by many existing publicly traded REITs.

And while this may pressure valuations in the near-term, over the medium-long term, values are likely to be higher due to the lack of investment in the current period on the high-quality space sought by companies seeking to return their workforce to in-person work.

Though it has been a punishing road for existing shareholders of office REITs, the future outlook appears promising.

Be the first to comment