Oscar Gutierrez Zozulia

Banking is very good business if you don’t do anything dumb. – Warren Buffett

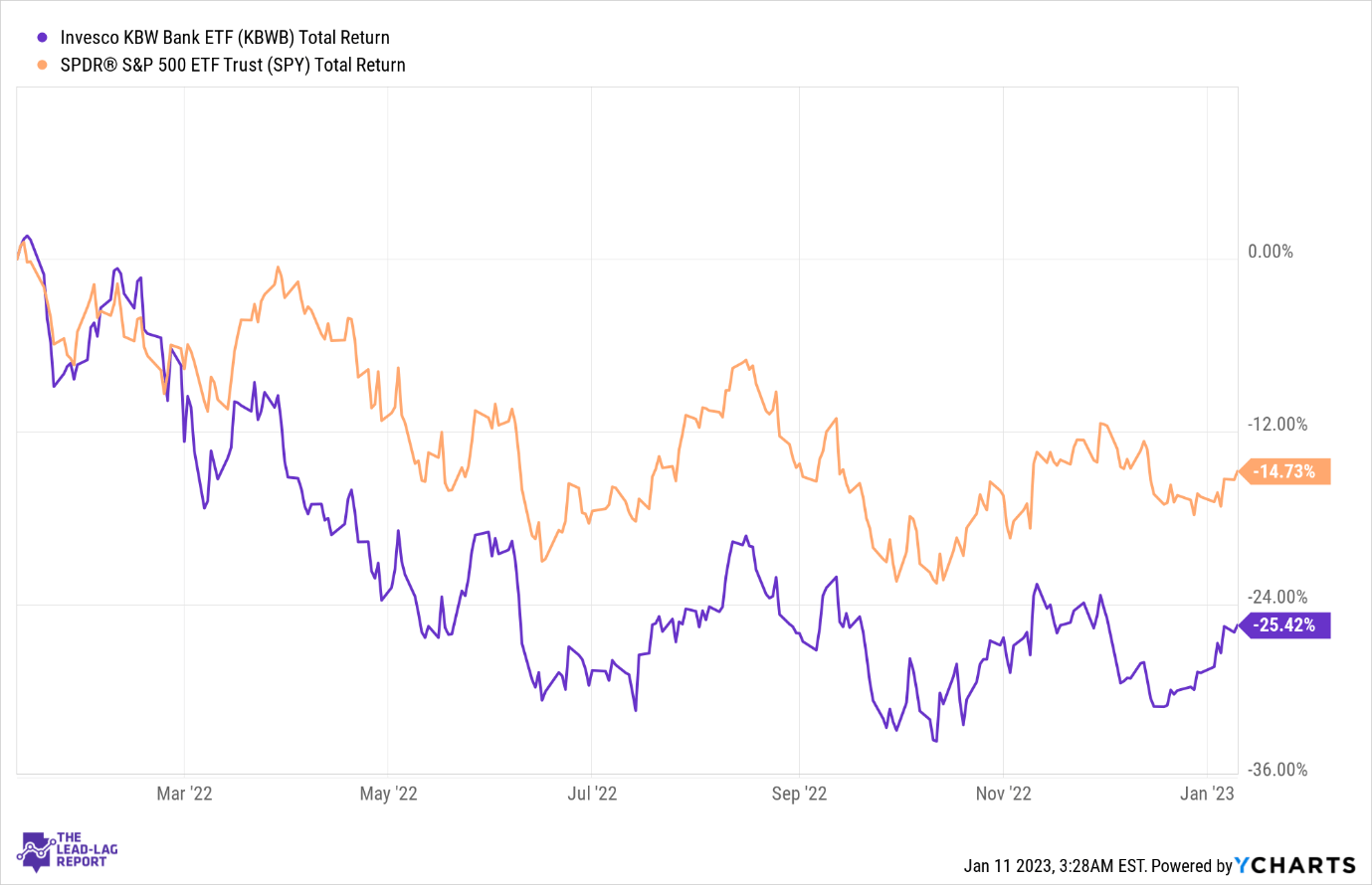

The Invesco KBW Bank ETF (NASDAQ:KBWB) tracks a small portfolio of large-cap stocks (~25) that are exposed to the business of banking in the US. This portfolio consists of companies ranging from regional banks, money centers, diversified institutions, and thrift institutions. KBWB’s performance over the past year hasn’t been great. Admittedly, while there was no money to be made with the benchmark either, KBWB fared a lot worse, losing one-fourth of its market cap.

YCharts

Could the tide change in the new year? Here are some big-picture thoughts for your perusal.

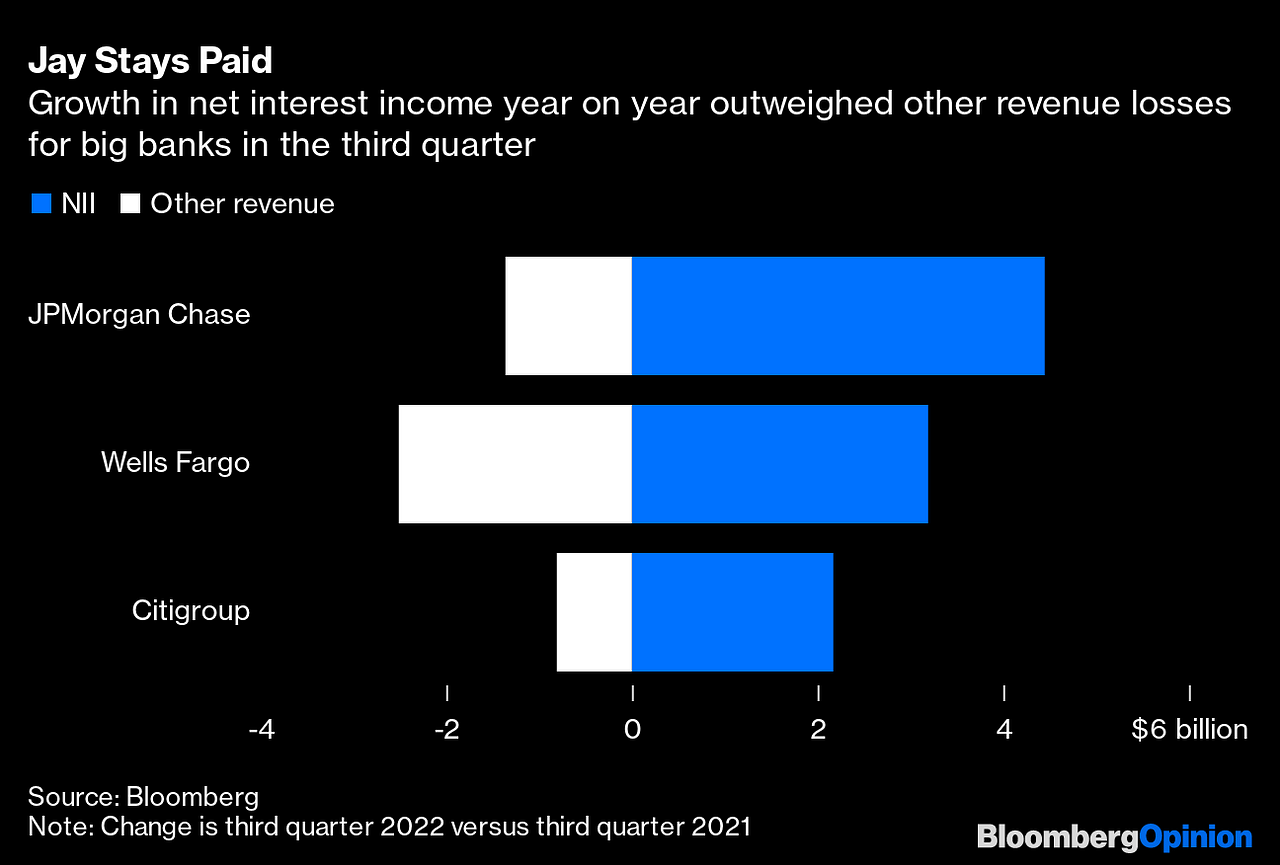

Subscribers of The Lead-Lag Report would note that in this week’s ‘Leaders-Laggards’ section of the report, I’ve highlighted how a ratio that measures the strength of the financial sector as a function of the S&P 500, has just recently broken past a 3-year resistance. This speaks to the interest that this sector has been seeing over the past month, and much of this is down to the “higher for longer” theme on rates. This feeds in very well to these institutions’ bread-and-butter, which is the net interest income line. For instance, in Q3, note that some of KBWB’s dominant holdings saw NII growth surge annually by 20-33%, even as the “other income” component proved to be underwhelming.

Bloomberg

The CEO of KBWB’s top holding JPMorgan – Jamie Dimon – has recently stated that rates may well have to cross the 5% landmark and even hit 6%! Also consider that the short-end of the yield curve continues to inch up (reflecting conditions in the labor market) and suggests that the Fed may keep rates high for long enough. Regardless, NII growth should continue to stay resilient for the foreseeable future and KBWB’s top holding looks poised to deliver another strong quarter of NII growth to the tune of ~37%.

While the NII line may stay buoyant, one ought to question the business appetite for credit when the US economy is struggling to cope with recessionary pressure. For a long time now, conditions in the services sector have been perceived to be sanguine, but the recent ISM services PMI number proved to be a shocker coming in below the dreaded 50 mark for the first time since the pandemic kicked off.

Then there’s also the dynamics within the housing and real estate sector. Granted, some of the largest holdings of KBWB have done well to scale back exposure to commercial real estate but one shouldn’t play down the cascading impact of a slowing housing market on general economic buoyancy, given how integral this is to the average US citizen’s net worth. As discussed in a Lead-Lag Live podcast episode with Melody Wright, decelerating rents are leading to anxiety amongst investors. Meanwhile, home builders are also seeing a record number of contract cancellations, even as inventory remains incomplete and under-constructed.

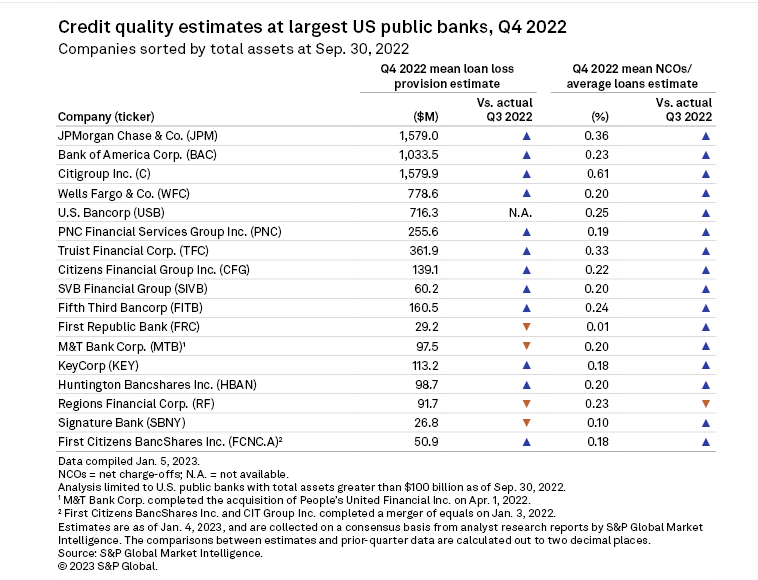

In effect, expect these banks to devote a lot more attention to asset quality challenges this year, and this could weigh on profitability. Jefferies believes that provisioning will be heavily front-loaded and expects the average allowance coverage ratio for the large banks to surge from just 0.53% as of Q3-22 to levels of over 2% by the end of this year.

S&P Global

In the coming earnings season, investors should also expect a sharp spike in the net charge-off ratio. With the exception of 1 bank (RF), the 16 large banks will likely see NCOs trend up sequentially.

Twitter

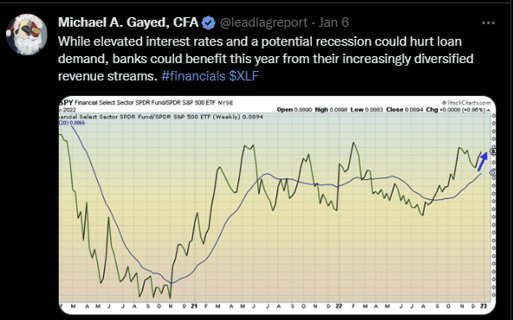

Conversely, as noted in a tweet, it’s somewhat comforting that these large banks have also built-up other streams of income enabling them to exploit conditions in the market. For instance, the ambiguity surrounding higher interest rates has enabled the currency and bond trading departments to stay relatively healthy.

Conclusion

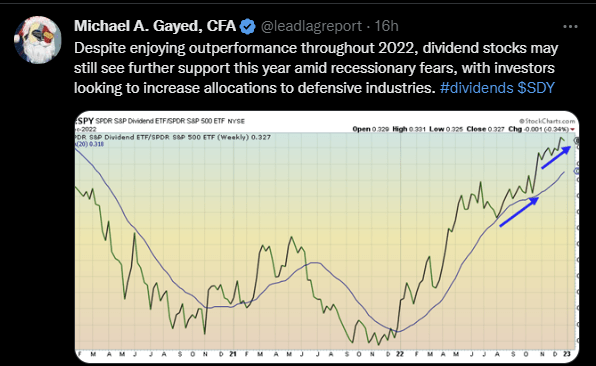

Investors shouldn’t also forget the useful dividend angle that comes with this sector. As noted in this week’s report, dividend stocks have proven to be one of the most consistent alpha generators over the last half year or so, with the dividend to SPY ratio hitting its highest level in around 3 years.

Twitter

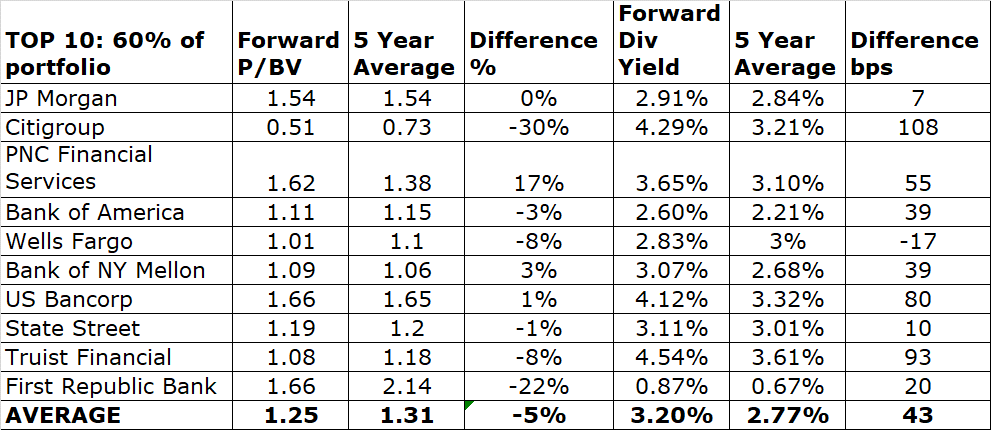

If one looks at KBWB’s top 10 holdings which account for the bulk of the portfolio (over 60%), the current dividend credentials look quite tasty. We can see that nine out of the top 10 names are all currently trading at forward yields that better than their historical averages. On average, the differential works out to almost 50bps! Note that on a forward Price to book value basis, these top 10 names are also available at a 5% discount to the historical average multiple of 1.31x.

Seeking Alpha

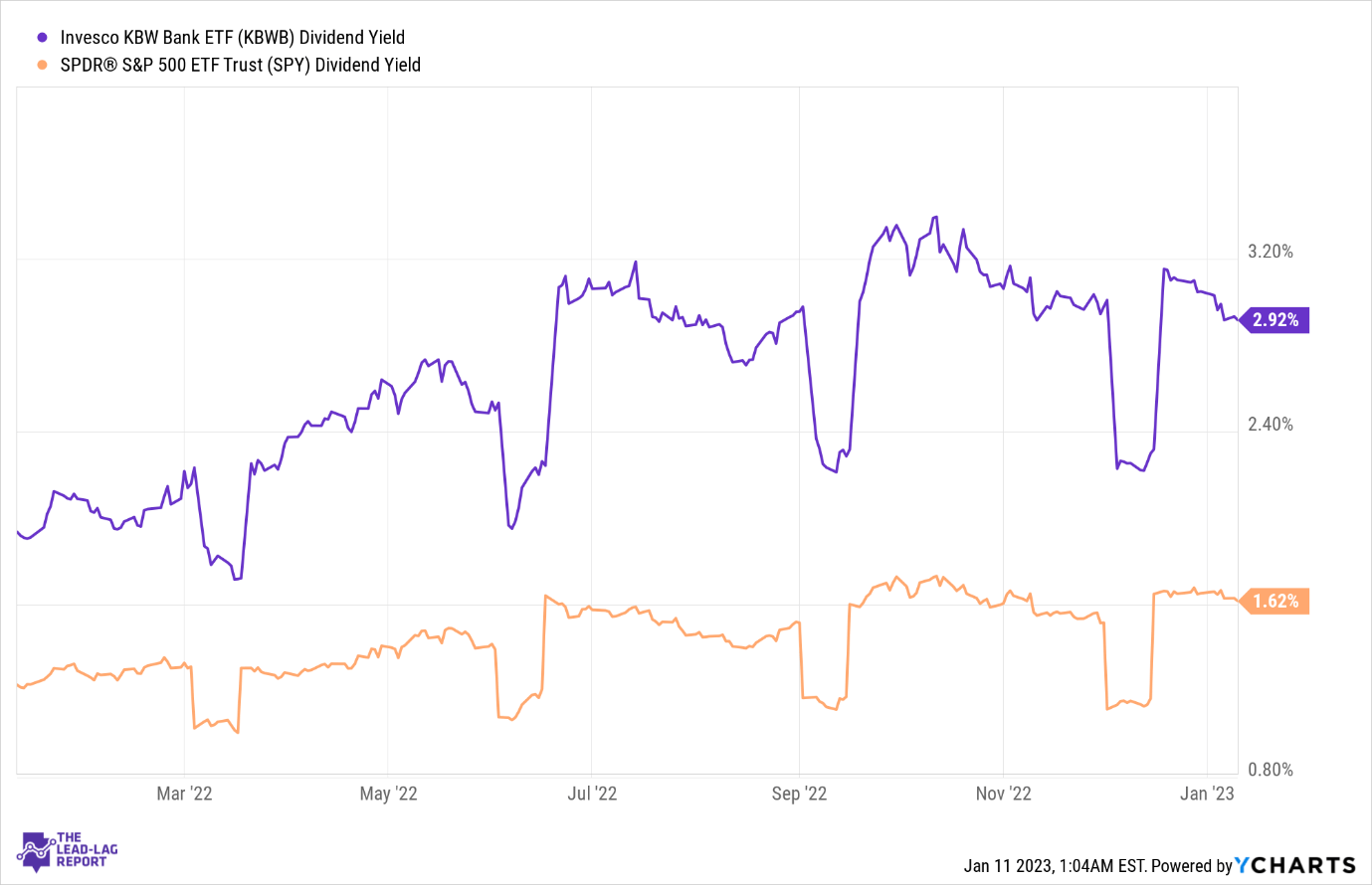

Meanwhile, it also helps that KBWB’s yield differential with the S&P 500 is a good 130bps higher than what you get from the S&P 500.

YCharts

As far as P/E valuations go, KBWB as a whole comes across as dirt-cheap with a multiple of just 8.4x, which translates to a 50% discount relative to the S&P 500.

Anticipate Crashes, Corrections, and Bear Markets

Sometimes, you might not realize your biggest portfolio risks until it’s too late.

That’s why it’s important to pay attention to the right market data, analysis, and insights on a daily basis. Being a passive investor puts you at unnecessary risk. When you stay informed on key signals and indicators, you’ll take control of your financial future.

My award-winning market research gives you everything you need to know each day, so you can be ready to act when it matters most.

Click here to gain access and try the Lead-Lag Report FREE for 14 days.

Be the first to comment