AndreyPopov

Investment Thesis

Intuit’s (NASDAQ:INTU) products mainly target smaller businesses and the self-employed. Given the changing interest rate environment and a possible recession, growth could be much weaker than previously assumed. In that case, the stock likely offers little margin of safety, as the valuation is already quite high. Moreover, the company spends 10% of its revenues on SBC, which is not shown in the non-GAAP numbers. Therefore, I consider the risk in this stock to be too high in relation to the potential gains.

Company Overview

Founded in 1984, Intuit is a software company that aims to make accounting easier for small business owners and freelancers. The company offers a wide range of financial tools to simplify managing finances. Including TurboTax (tax software), Credit Karma (credit card service), Mint (personal budget planner), QuickBooks (accounting software), and Mailchimp (email marketing platform). The company acquired Mailchimp in November 2021 for $12 billion and Credit Karma in 2020 for $8B

With these and many other tools, Intuit empowers its users to take control of their finances, reach new customers, plan loan repayments, and complete tax returns. In 1990, the company had 1.3M customers. Today, thanks to organic and acquired growth, customers have grown to 103M. Of these, 93M are private consumers, and 10M customers are either small businesses with up to 100 employees or self-employed. Thus, the company has built an impressive track record, strongly outperforming NASDAQ.

Investor presentation

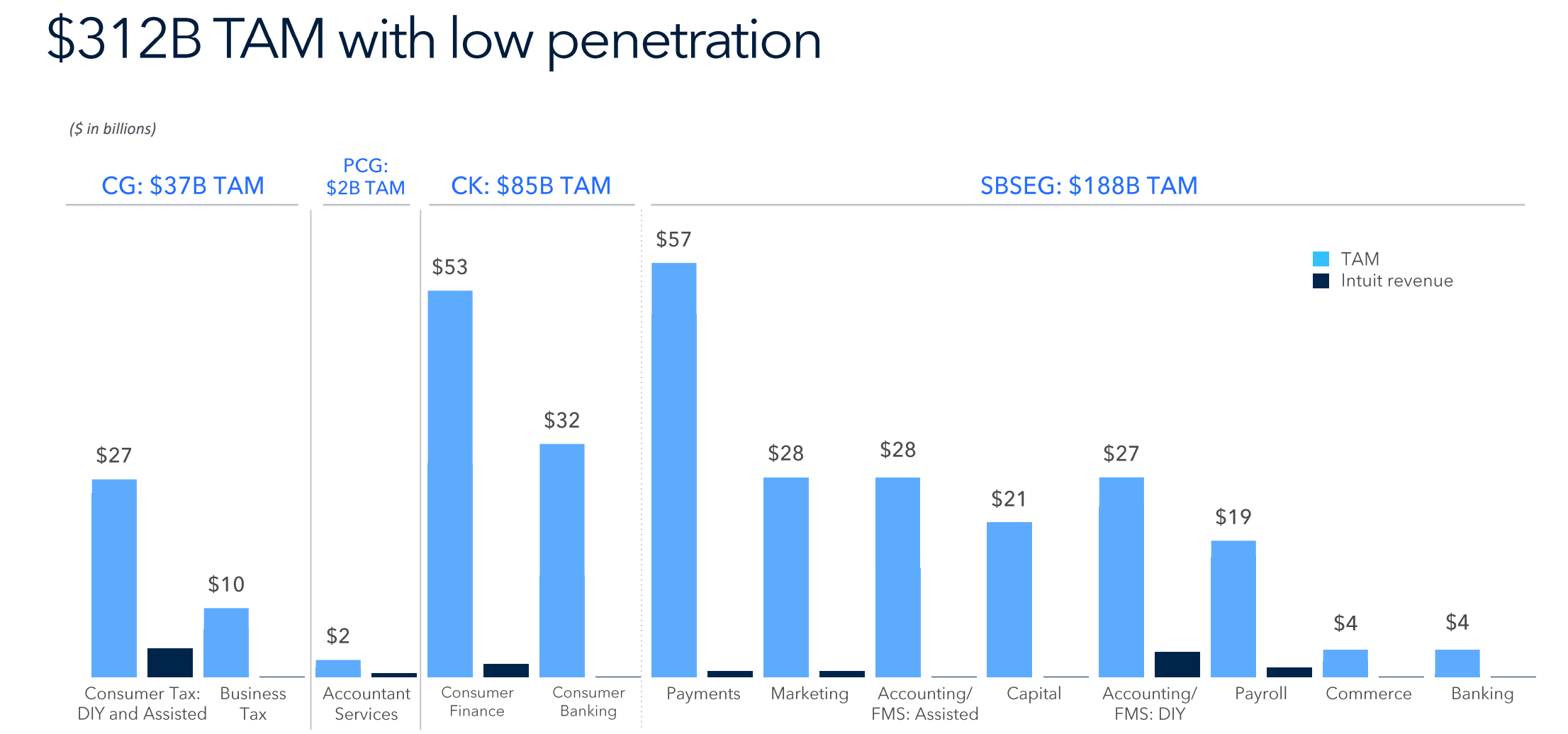

Additional Opportunities

Given that there are already 100M customers, the question arises about how much potential there still exists. In the meantime, however, the company is active in so many areas that it just scratches the surface in most of them. But you always have to be cautious; the potential market size sounds very high for any company, but it virtually never happens, and this potential might not be reached.

Investor presentation

The company aims to have 200M customers by 2025. On a positive note, the company’s investor presentation is quite specific about its goals, breaking them down into different areas. For example, it wants to increase the number of monthly active users and improve customer retention. In terms of shareholder value, the company intends to increase revenue per user and achieve double-digit growth per year until 2025. The “Growth Flywheel” illustrates how these goals should be achieved. Intuit’s self-learning systems are fed $2.0T of invoices annually and make “58B daily AI predictions creating personalized customer benefits”.

Investor presentation

A possible growth driver for the future is also international expansion. So far, the company has almost only been active in the United States. However, the addressable market would probably increase greatly with further expansion. Some services, such as consumer tax, are already available in other countries, and of course, Mailchimp also works internationally.

Impressive Growth

Given the current 103M customers and the target to have 200M customers by 2025, this corresponds to an annual growth of about 25% which has to be achieved in the next three financial years to reach this target. Is this realistic? Given the low level of debt, it is likely that the company will continue to make acquisitions, as it has done many times in the past.

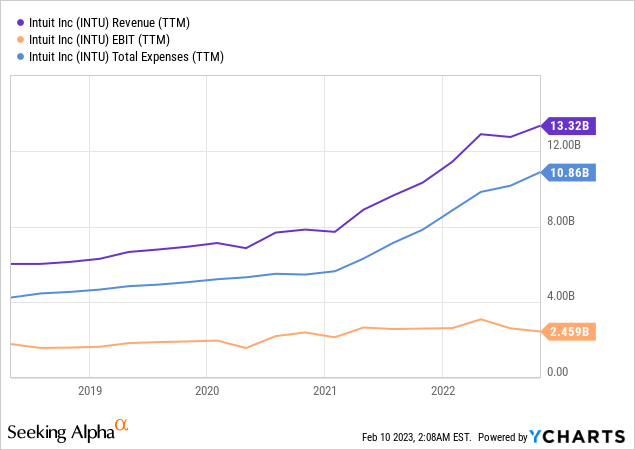

As far as revenue is concerned, the average growth over the last five years is 20% pa. However, costs have risen almost in the same proportion, so EBIT has not improved nearly as much.

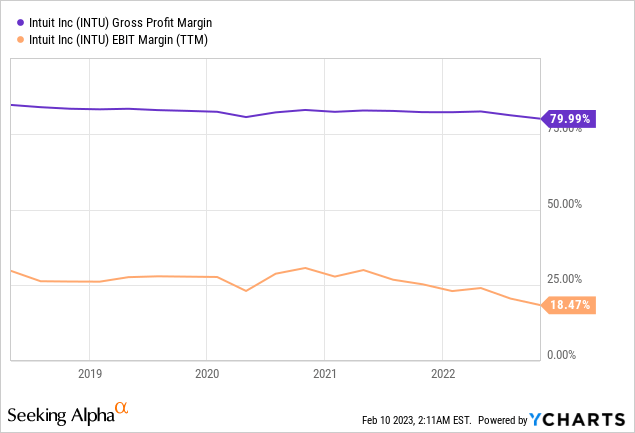

Nevertheless, it is a highly scalable business with solid margins. Accordingly, the company also receives an A+ rating for profitability in the Seeking Alpha Quant rating.

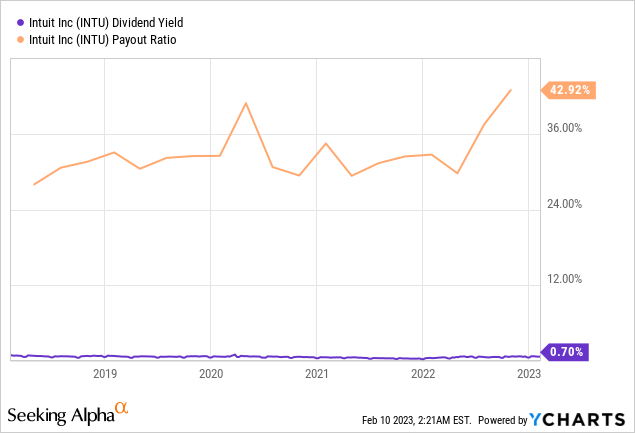

The dividend yield is meager and currently stands at 0.7%. The average increase over the last five years was 15%. This growth rate is unlikely to be sustained long-term as the payout ratio tends to rise slowly.

Valuation

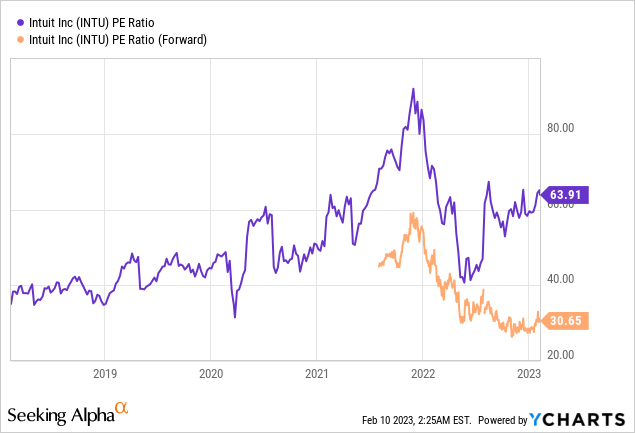

The company is currently valued at an enterprise value of $123B. The market cap is $118B, and the total debt is $7.6B. If the analysts’ estimates for the next 12 months are correct, the future P/E ratio is around 30. However, this is the adjusted profit, which does not include the very high stock-based compensation; more on this further below. In addition, the analysts could, of course, be wrong. Here, the company does not have a fantastic track record. So far, there have been 13 earnings revisions downwards and only five upwards.

Going back to GAAP vs. non-GAAP to illustrate the huge differences that exist here. Non-GAAP disclosures have their justification, but I also disagree with some elements. For me, SBCs are part of employee salaries because cash salaries would be higher if they did not exist. Therefore, this is a popular way for companies to disguise the actual employee salaries, in my opinion.

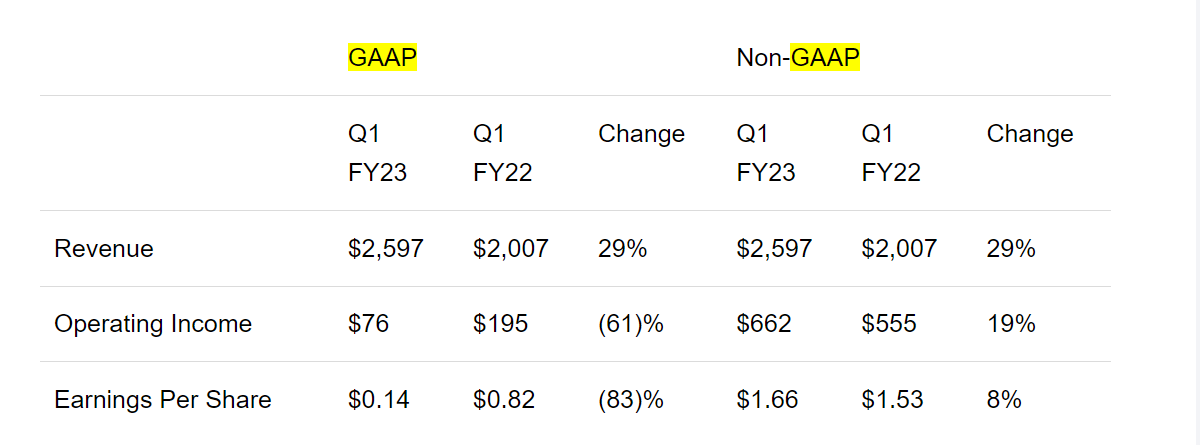

Intuit FY2023 Q1

For the full fiscal year 2023, Intuit updated revenue guidance and reiterated GAAP and non-GAAP operating income and earnings per share guidance. The company now expects:

- GAAP operating income of $2.794 billion to $2.899 billion, growth of approximately 9 to 13 percent.

- Non-GAAP operating income of $5.258 billion to $5.363 billion, growth of approximately 17 to 19 percent.

- GAAP diluted earnings per share of $6.92 to $7.22, a decline of approximately 5 to 1 percent.

- Non-GAAP diluted earnings per share of $13.59 to $13.89, growth of approximately 15 to 17 percent.

FY23 Q1 results

Overall, the valuation is high even with the non-GAAP figures. If one were to take GAAP figures, things would look quite grim. EPS growth figures between 10% and 15% result in a PEG ratio of 2, which is considered very expensive.

According to Fastgraphs, the company has a potential annual return of 25% until the end of 2024 if it returns to its average historical valuation (P/E ratio of 38). But even at a still high P/E of 27, the annual return would be only 4%. That is the problem with already high valuations; the margin of safety is minimal. If the share were trading at a P/E of 19 at the end of 2024, the annualized return would be -12%.

Risks

Considering that the company provides accounting software and other services mainly for small businesses and self-employed people, you likely already realize how cyclical the business model is. Or, to put it another way, it is also very dependent on interest rates because when capital becomes more expensive, fewer companies are founded, and fewer companies survive. Although Intuit has a platform for granting loans (Credit Karma), it also runs into problems when potential customers generally have to be more careful with their money. In Q3 FY22, Credit Karma recorded growth of 48% YoY. However, in Q4, the revenue of $425M was down for the first time. According to management, lenders on the platform are worried about the creditworthiness of their borrowers due to high inflation and potentially rising unemployment in the wake of a possible recession. At the same time, consumers are also asking for fewer loans for major new purchases due to rising living costs. Overall, it can be said that Intuit is benefiting greatly from low-interest rates. Given the current change and difficult market conditions for small businesses, it is questionable whether the company can achieve its ambitious goals.

Furthermore, the market for accounting and tax software is highly competitive. There are some larger competitors. Intuit specializes in small and medium-sized enterprises and self-employed individuals, whereas competitors such as Oracle (ORCL) or ADP (ADP) target bigger corporations. The growth of recent years has shown that Intuit has strong products on the market and can hold its own despite the competition.

Share dilution and insider selling

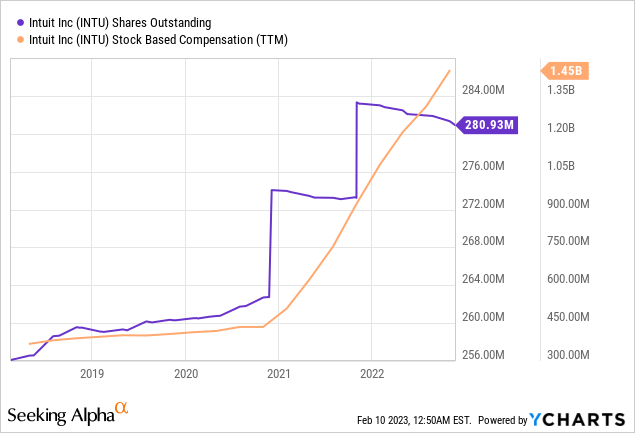

I always pay attention to share dilution and whether there is insider selling. In addition, it’s important to look at stock-based compensation. These are all insider sales since September 2022. Given the market capitalization, this is not much.

openinsider.com

The number of outstanding shares is increasing due to many acquisitions, such as MailChimp, in 2021. This is usually not a problem as acquisitions also increase revenues. In addition, there has been a return to share buybacks since the end of 2021 (around 1% in the last 12 months). However, share-based compensation is significant. It is always important to remember that non-GAAP figures exclude SBCs. In the case of Intuit, SBCs account for 10% of revenue. Since I check this on every article, I can say this is a lot compared to other companies. The shareholder also gets a small dividend and a bit through share buybacks, but that is nowhere near 10% of revenue. I think it’s fair that people are well rewarded for a good job, but some companies overdo it, in my view.

Conclusion

Intuit has received a premium valuation from the market for years, partly because of its high-margin business model and partly because it is a sticky business model with high switching costs for existing customers. Compared to its peers, it has tended to focus on small businesses and the self-employed, who do their accounting and need other tools such as email distribution and loans. With the changing interest rate environment, the business could grow much more slowly than previously thought, resulting in a sharp re-rating of the company. In this case, the downside is high; I estimate at least 30%. For my taste, the risk is too high in relation to the potential gain. And I do not expect the company to return to its previous average valuations. I give the stock a hold rating as it is not a company I would short either; the company is in too good a financial position and has too big a moat with existing customers.

Be the first to comment