Charday Penn

My followers may recall I recently re-initiated coverage on Intrusion (NASDAQ:INTZ), a cybersecurity threat detection company, with an article in early June. For those who do not wish to read the entire article, let me sum up my thesis: a professional with the pedigree of new CEO Tony Scott (formerly CTO at GM; CIO at DIS, MSFT, VMW, and the Federal Government under Obama Administration) does not come to run a small, beleaguered company unless he truly believes in the company’s technology. In other words, an investment in INTZ is essentially an investment in Tony Scott. And as someone following small-cap companies for some time now, let me tell you: we rarely get to invest in CEOs like Tony Scott in the small-cap space.

Granted, my investment thesis is a little more nuanced than how I summarized it above, but my basic point remains. During Tony Scott’s short tenure, the company has made several key changes. First, the messaging surrounding their Shield product changed. This messaging makes sense. Instead of advertising Shield as the “be all, end all,” INTZ now properly markets the product as one among several that companies can use to enhance their protection against destructive cyber attacks. Second, the company quickly changed its go-to-market strategy. Instead of hiring dozens of salespeople to sell a product that, frankly, was not yet fully ready for market, Scott invested in improving Shield and is focusing on partnering with major players in the technology space.

In this article, I will update on INTZ’s progress over the past three months. All of these changes and updates indicate to me that INTZ is soon to reach a pivot point. Specifically, the company is nearing a point where Shield’s family of products is ready for primetime. This should result in the company materially increasing its revenue and EPS in 2023 and beyond. Because of this, I believe investors in the stock now will be handsomely rewarded.

Shield Cloud & Endpoint Ready for Primetime

INTZ currently offers one form of Shield. This initial version is an on-premise device. The problem with an on-prem device is that it requires hardware installation. While this might not be a major issue for a big-name player in cybersecurity, it does handicap Shield salespeople. In order to currently sell Shield, the company must convince prospective customers to install hardware as part their network; hardware from a company they had not heard of previously. That is a heavy lift.

Fortunately, INTZ is about to remedy this scenario with the release of Shield Cloud and Shield Endpoint. These products will allow prospective companies to use Shield on a more limited basis, ensuring the product works and does no harm. If the customer is satisfied with Shield at that point, it greatly increases the chance of the customer installing Shield on-premise. Regardless, even with the Cloud and Endpoint solutions, INTZ profits and protects a significant portion of a customer’s infrastructure.

Intrusion Website

According to the most recent guidance on the 2Q22 earnings call, the Cloud and Endpoint solutions should be ready for general availability by EOQ3–within the next few days. When I spoke to people familiar with the company, they indicated INTZ remains on track to meet this target, so I expect to see an announcement and/or an update to the company’s website soon. The availability of these solutions greatly increases INTZ’s TAM and sales opportunities.

Strategic Partnership Opportunities Nearing

In addition to, and likely dependent upon, the Cloud and Endpoint releases, INTZ continued to guide on the 2Q22 earnings call for a major strategic partnership to be finalized by EOQ3. My own research indicates the company continues to progress in reaching the finish line on a first strategic partnership for its Shield product. However, it may be in October or early November before that deal is fully finalized and announced. As is so often the case, massive companies move at a slower pace than smaller companies like INTZ. But, in the end, whether INTZ finalizes the deal in September or October is rather irrelevant to the bigger picture.

Speaking of the bigger picture, you may notice I mentioned INTZ is close to signing its “first” strategic partnership. That is because the company has hinted they expect to sign at least one, if not two, additional strategic partnerships over the next 6-12 months. Each of these partnerships would address various aspects of the cybersecurity market.

While I am not aware of the identity of any of these partners, I am under the distinct impression they will be major players in their space and will, thus, validate the Shield product. With Scott’s resume (again: MSFT, VMW, Federal CIO), one can imagine the possibilities. In any case, based on Tony Scott’s commentary on the Q2 call, it sounds like INTZ expects their strategic partners to make a financial investment in the company. Based on all these factors, I believe the stock could rally if and when a strategic partnership is announced.

Opportunities Abound

In addition to the strategic partnership opportunities, INTZ already formed and announced smaller partnerships. For example, in June the company announced a reseller deal with InnerCore Technologies. And in August they entered an agreement with OneSmartLaboratory, a deal that required Shield to meet and exceed HIPAA regulations for Electronic Protected Health Information. But there are three other near-term opportunities I want to highlight in more depth. These include a new relationship with Super Micro Computer (SMCI), the possibility of being added to the GSA Schedule, as well as the approved list of the Department of Homeland Security (“DHS”), and an upcoming exhibit at the Association of the United States Army (“AUSA”).

Super Micro Agreement

On the Q2 call, Tony Scott announced an agreement with SMCI as INTZ’s primary global supplier of hardware. He then highlighted how SMCI supports INTZ’s expected growth. “First, Super Micro helps us improve the performance of our existing technology through its excellent engineering capabilities. Second, it serves as a reliable hardware partner, with the ability to get us products promptly as we strive to satisfy global customer demand. Third, Super Micro has a global presence with operations in over 100 countries, which will accelerate our hardware deployment and provide international technical support to our global customers at a local level.”

SMCI Website

While this agreement is important in its own right, one has to wonder if the INTZ-SMCI relationship will deepen over time. To this point, fellow Seeking Alpha author Shareholders Unite recently wrote a piece about SMCI. In that article, Shareholders Unite stressed that SMCI “is undergoing a successful transformation from one that offers products to a company that offers solutions.” The author later noted: “[SMCI] is morphing from being a supplier of parts to a Total Solution Provider, basically acting as a one-stop shop for customers.”

I would further note that SMCI white labels other companies’ products, such as Office Depot computers and several cloud-related products. Based upon all of this, it seems plausible that the INTZ-SMCI relationship could blossom into something more down the road.

Government-Related Opportunities

With respect to government opportunities, I noted in my previous article that CEO Scott has a plethora of connections in this space due to his time as Federal CIO. But in addition to those opportunities, INTZ could benefit from much broader government programs.

One such program is the GSA Schedule. GSA Schedule is shorthand for the U.S. General Services Administration Multiple Award Schedule. The GSA Schedule simplifies what otherwise would be an extremely complex navigation for governmental entities through US law. Based upon that law, there are numerous requirements that need to be met for a government entity to purchase from a private enterprise. The GSA Schedule simplifies this by providing these government entities with a list of private enterprises, products, and pricing that satisfies US law. In other words, if you are listed on the GSA Schedule, you have already been vetted and approved to be used. An individual government entity, therefore, does not need to conduct their own due diligence or negotiate fair pricing. In short, being listed on the GSA Schedule provides a company with an enormous opportunity to earn government business.

According to people familiar with INTZ, the company’s Shield product will likely become listed on the GSA Schedule in tandem with a strategic partnership under negotiation. If that partnership falls through, INTZ would, of course, attempt to be listed under the GSA Schedule separately, but the quickest approach is to be adopted in through the strategic partnership. As important as this would be for INTZ, a source also hinted that the company could be approved by the DHS as well. This list is even more exclusive than the GSA Schedule, and could greatly bolster INTZ’s exposure to prospective government customers.

Association of the United States Army

The AUSA plans to host its 2022 Annual Meeting and Exposition on October 10-12 in Washington, DC. INTZ is listed as a “National Partner Member Organization” for this upcoming Exposition. While INTZ having an exhibit at this event would be significant any year, given that international military and government representatives regularly attend, it is most especially important this year. That is because the meeting’s theme is “Building the Army of 2030.” As part of this theme, the AUSA will specifically highlight the role of cybersecurity in the Army of 2030, meaning that INTZ will be one of the companies showcased at the center of the Exposition. I believe this opportunity with the AUSA will allow INTZ to make important connections with military and government representatives from around the world, entities increasingly concerned about specific cybersecurity attacks INTZ can uniquely help prevent.

Intrusion Website

Risks

In my re-initiation article linked in the intro, I cited INTZ’s biggest risk as its bad reputation from the circumstances surrounding their former CEO. I believe the advancements made and being made by Tony Scott are beginning to heavily mitigate this risk. Still, until the company receives major validation via a strategic partnership, some investors will likely want to stay away based on past concerns.

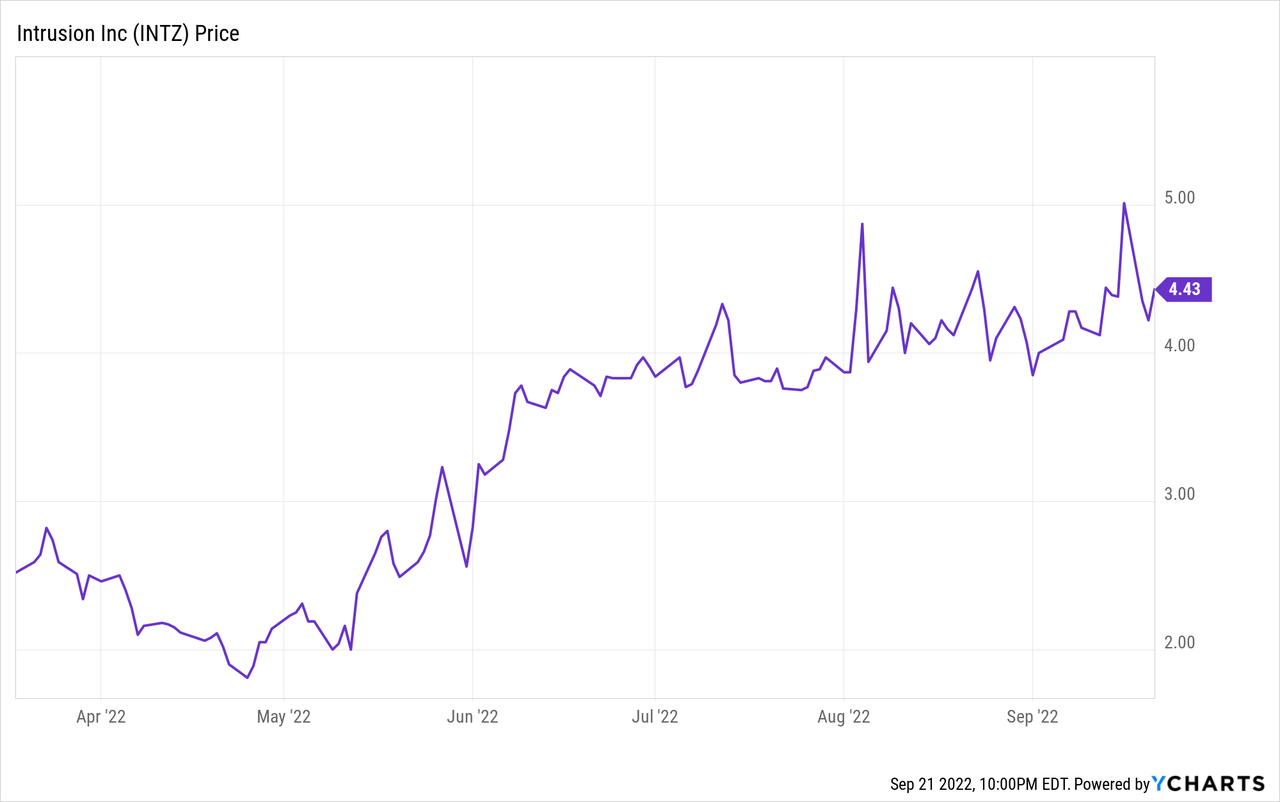

Another risk with INTZ is the obvious need for a capital raise. On the Q2 call, Tony Scott clearly indicated the company expects to raise $15-20M via equity offerings over the next year or so. This is to help support the continued investment in the Shield product offerings, as well as to eventually fund a sales team once the products are ready to be heavily marketed. The company, as I noted in my prior article, already gained access to around $10M of that money via short-term debt obligations. The proceeds of the equity raises, then, would be partially used to pay down that debt. The company chose that route—initially taking out debt to later be settled via equity—because they believed the stock was massively undervalued. That turned out to be a wise move.

Recently, INTZ filed a Form 8-K with the SEC, noting they entered a Securities Purchase Agreement for $5.9M of INTZ shares. The purchasers of the company’s stock paid market value for the shares plus warrants ($4.29). Notably, the purchase price was roughly twice the value of INTZ’s shares when they took on the short-term debt. Hence, my comment that the company handled this situation wisely.

Still, it seems clear the company will need to raise an additional $10-15M over the next year. Specifically, they have roughly $5M in the second tranche of debt to repay. In addition, they will probably need a little more to fund R&D and operations until they become cash flow positive. However, with material announcements likely to come soon, it is probable future raises will be done at higher prices and result in less dilution to current shareholders.

Valuation

As noted in my last article, valuing INTZ right now involves more art than science. Therefore, I wish to highlight a couple qualitative factors.

First, it appears to me that INTZ could obtain breakeven at roughly $20M in annual revenue. Once Shield revenue ramps, gross margins should be similar to other SaaS-type businesses, which is to say 70-80% for that portion of the business. With that structure, it is easy to see how INTZ can quickly go from a cash flow negative company to a cash-producing machine. For this reason, I have tried to stress and lay out the picture of how INTZ is now at a pivot point. Because once that pivot happens, momentum can build quickly.

Second, INTZ’s legacy business, which primarily consists of government consulting business, has never fully recovered from the double whammy of Covid disruptions and government budget delays. Given the passing of a federal budget, and based on management’s prior guidance, I think that INTZ’s government contracting business will return by EOY22 to more historical norms. That would mean by the middle of 2023 INTZ could be back to approximately $10M in annual revenue from these contracts alone.

Intrusion Website

Regardless, the multiple variables and uncertainties do not allow me to be as precise in my valuation as I normally prefer. For that reason alone, some investors may choose to pass on INTZ as an investment at this time. As for me, I do not believe Tony Scott came to INTZ to operate a $90M market cap company (current valuation). Moreover, I believe a strategic partnership with a major company will lead to shares rallying significantly from current levels. But, obviously, the details of that partnership, if and when announced, will give us a better picture of INTZ’s value. In any case, I believe such a deal will almost certainly justify a price of at least $6-8/share. That is because if a major company decides to partner with INTZ for their Shield product, I believe it validates that their intellectual property alone is extremely valuable.

Conclusion

I believe INTZ is nearing a pivot point. Since coming onboard, CEO Tony Scott continues to methodically build a base for the successful launch of the Shield Cloud and Endpoint solutions that will drastically increase the company’s TAM. In addition to what Scott has already accomplished, he has several opportunities ahead, including adding Shield to the GSA Schedule and DHS cybersecurity approved product list. Moreover, Scott has continued to signal that INTZ is on the brink of a strategic partnership—which could be the first of several—with a major company. Taken together, I believe INTZ has a bright future and investors would be wise to take a position prior to INTZ’s release of Cloud and Endpoint, and before a strategic partner validates the Shield offering.

Be the first to comment