VioletaStoimenova

International General Insurance Holdings Ltd. (NASDAQ:IGIC) may be a stock market newbie, but it is one of those small-cap companies investors may consider. In the last two years, International General Insurance Holdings has expanded amidst pandemic disruptions. Today, it remains durable and well-positioned against market volatility. Revenues and bottom-line income are stable. Cash and securities allow them to cover insurance liabilities and dividends. Indeed, it is a secure stock with balanced growth, risks, and sustainability.

Meanwhile, dividends are continuous, but future growth and yields may not be enticing. Dividend payouts may be too little compared to the company’s income and stock price. Nevertheless, the stock price stays bullish yet reasonable with upside potential.

Company Performance

Amidst market volatility, International General Insurance Holdings Ltd. remains durable. It may be a market newbie, but it strategically navigates a rugged environment. It balances growth and returns with risk and cost-reduction strategies. International General Insurance pays off by maintaining a robust performance thanks to its prioritization of viable growth and prudent portfolio diversification.

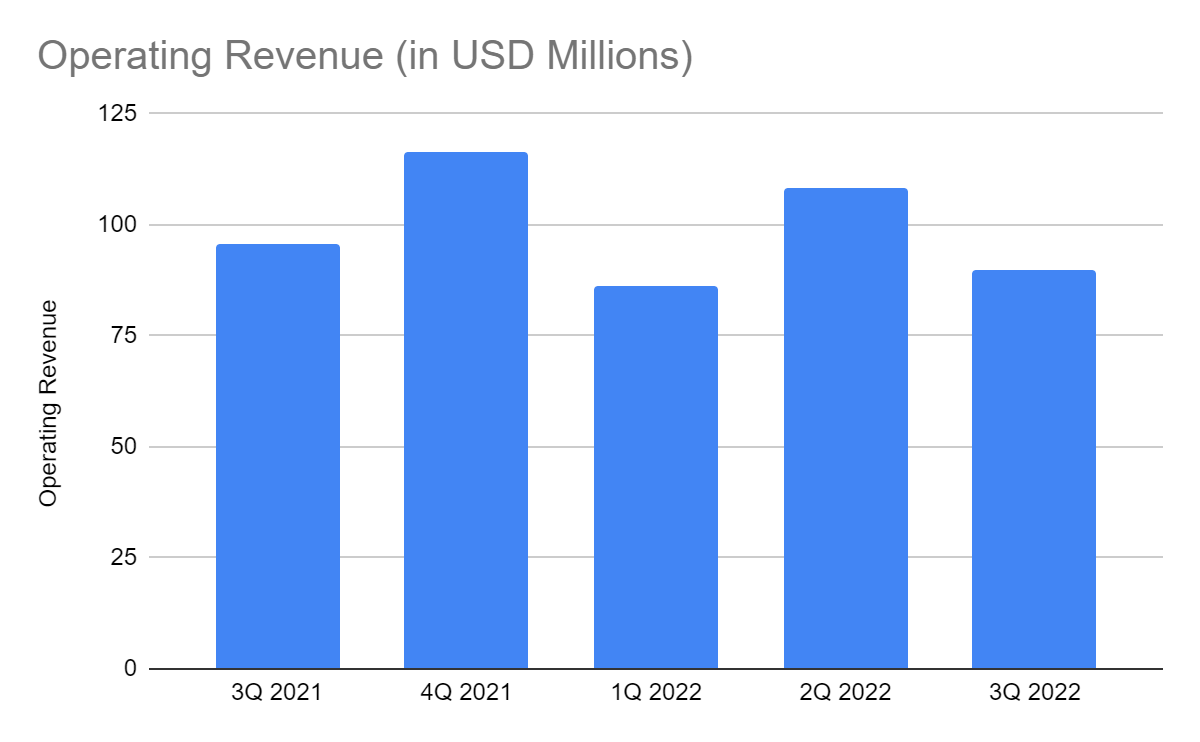

The core operations of IGIC remain robust and stable. The core operating revenue amounts to $90 million, a 5% year-over-year decrease from 3Q 2021. Yet, we can see that all revenue components are growing. These mixed results can be attributed to three factors. First, the core operations continue to expand. It allows the company to fortify its domestic and international market presence. The larger operating capacity can cater to more customers. Also, it maintains agile pricing to cope with changes in policyholders. It supports the execution of an underwriting strategy focusing on growth and viability. With its well-managed market demand, premiums earned keep growing.

Operating Revenue (Yahoo Finance)

Moreover, it focuses on where it is at its best. It is most evident in steady short-tail line growth, particularly property, construction, and energy. Likewise, reinsurance and short-tail segments remain impeccable. Hence, its premiums earned amount to $96.3 million, a 5% year-over-year growth.

Second, IGIC maintains prudent and conservative portfolio management. It diversifies its portfolio in line with macroeconomic headwinds. Most of its investments are composed of fixed-income securities with 48%. Even better, most of these securities are backed by the government. These are more flexible to inflation rate changes, leading to stable yields and ideal credit quality. Only 5% of its investments are equity. Regarding locations, it has balanced investments across different regions. These include North America, EMEA, and Australia. The countries in these regions have more stable economies and stronger currencies. It is no wonder IGIC’s investment income reaches $5.5 million, a 38% year-over-year increase.

However, the impact of forex hurts the core operations. It offsets the impressive growth in premiums and investments. Forex losses of -$10.4 million are more than twice as much as the losses in 3Q 2021. We must note that Jordan sets its currency at a fixed exchange rate and pegs it to USD. Despite the volatility, the U.S. economy remains relatively strong, reducing the relative value of the Jordanian Dinar this quarter. But overall, IGIC’s revenues show sustained growth while averting undue risk.

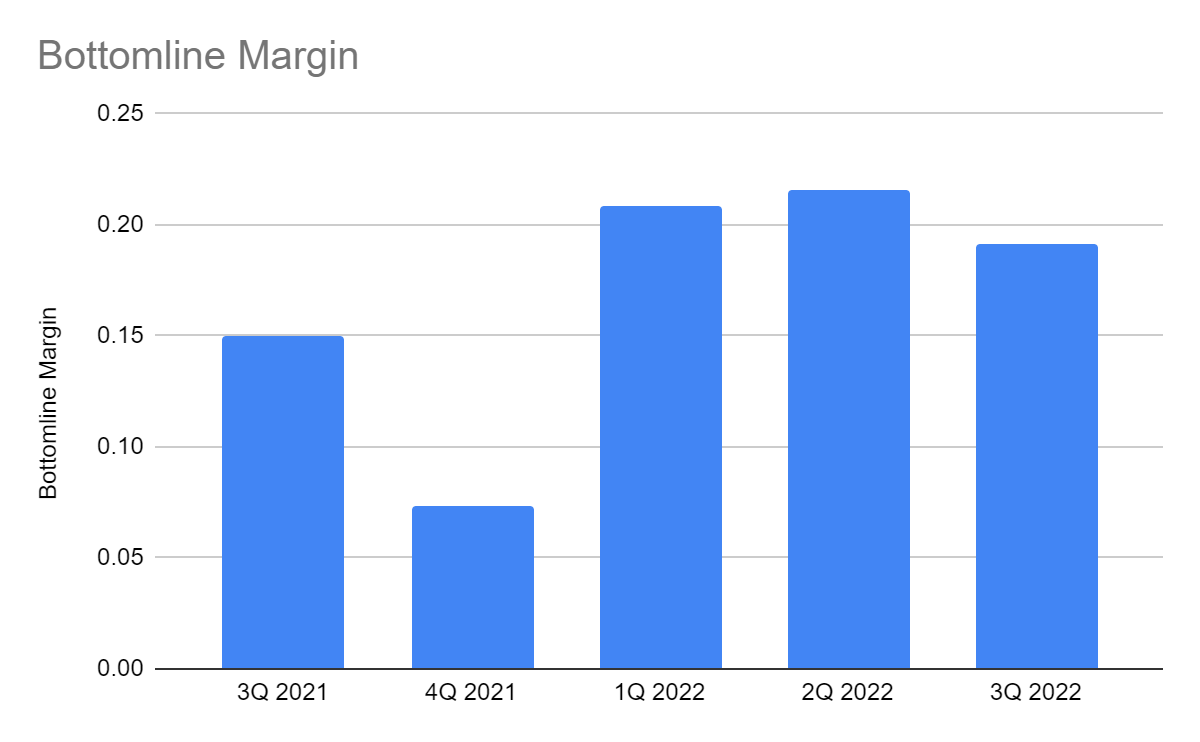

What makes IGIC a trustworthy company is its efficient asset management. It keeps its costs and expenses stable as it expands amidst the rising prices. So its combined ratio continues to decrease to 74% versus 84% in 3Q 2021. Indeed, revenue growth offsets operating costs and expenses. Its operating margin almost doubles to 31% from 17% in 3Q 2021.

Its non-core operations are also stable, showing consistency in the business. Net profit margin remains high at 19% versus 15% in the comparative quarter. It proves the continued success of its viable growth strategies.

Bottomline Margin (Yahoo Finance)

In the following years, the company may continue thriving since it remains well-positioned value creation opportunities. Aside from IGIC’s current strategies, it may expand further with its planned M&A in Scandinavia and increased market presence in Bermuda. It can sustain its current pace, given its adequate financial capacity. I will discuss it in the next section.

Market Risks, Opportunities, and Core Competencies

The potential challenge lies in rising energy commodity prices. Despite being near the Arabian Peninsula, Jordan has limited fossil fuel production. Fortunately, it has vast oil shale reserves of over 70 billion tons. Inflation rate changes are also another challenge. Jordan maintains impressive economic freedom, ranking thirty-second worldwide. But IGIC has a long way to go to match the US, the UK, and the Eurozone. It affects foreign currency translation, which reduces its revenues. Fortunately, the stronger currencies of these countries have advantages. The offsetting effect of ForEx may be substantial, but the overall operations remain solid. It enjoys higher premiums and foreign investment yields.

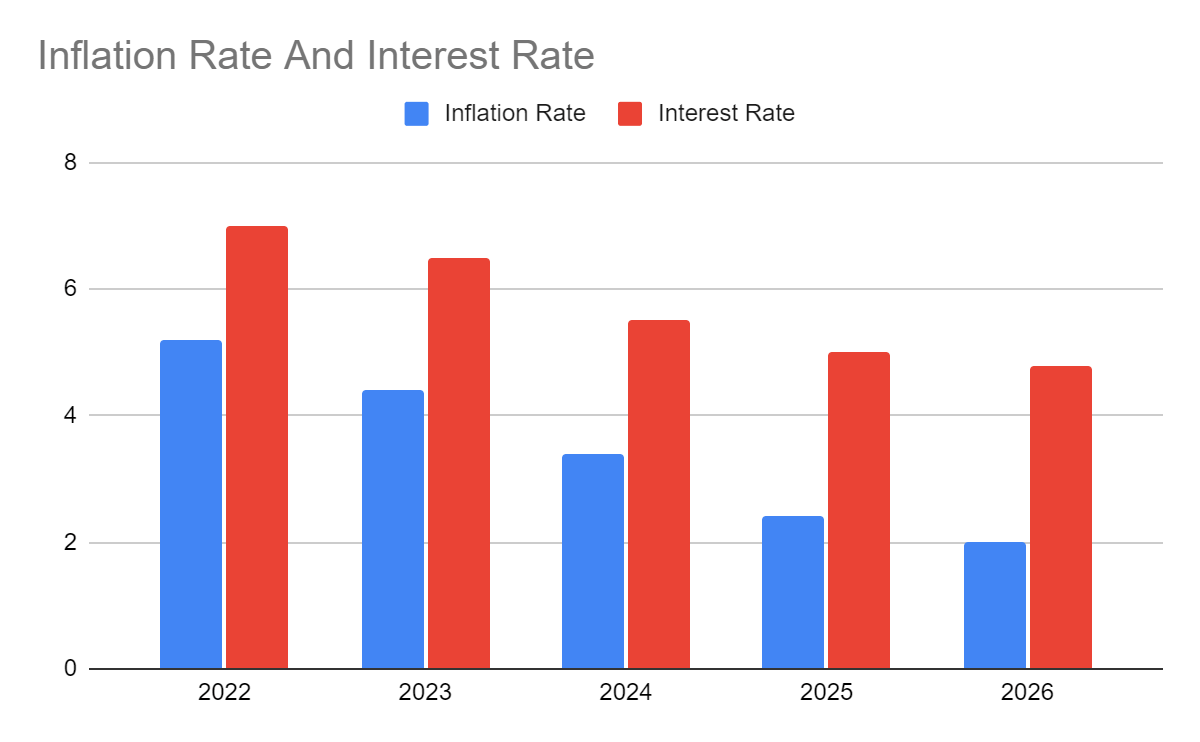

Also, Jordan’s economy is on its way to stability. Inflation continues to lull at 5%. With that, we can say the inflation peak is done. I expect it to keep decreasing to 3% in the following years. We can attribute it to more stable market demand and the costs of imported materials. It may help the core operations with more stable labor-related expenses. Regarding borrowings, interest rate hikes are not much of a concern since the company has already paid its borrowings. The impact of interest rates may be more evident in ForEx implications for business transactions. But of course, it must still be careful since it operates in other countries. It has some locations in Bermuda, which was also affected by Hurricane Ian, leading to higher claims from insurance companies.

Inflation Rate And Interest Rate (Author Estimation)

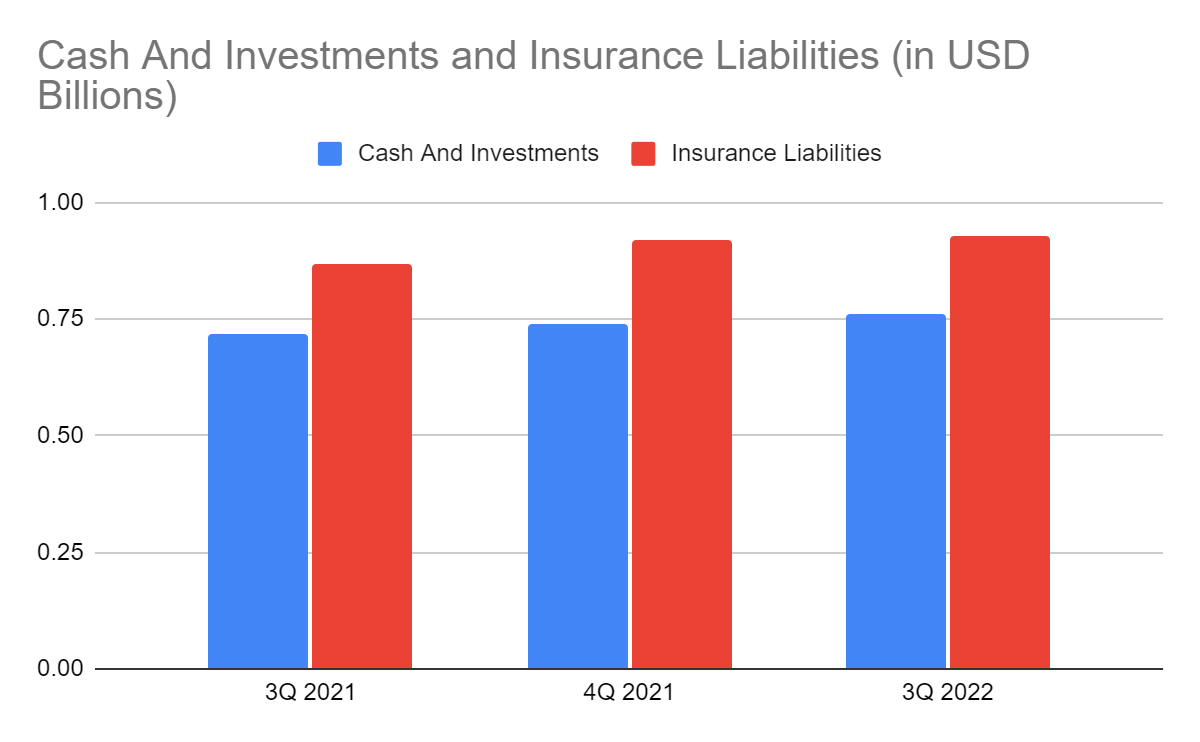

Amidst all these market changes, IGIC remains well-positioned. It maintains an impressive Balance Sheet, which is one of its cornerstones. It reflects the company’s adequate financial capacity and portfolio diversification. Cash reserves are adequate and stable at over $200 million, comprising 17% of the total assets. Investment securities of $500 million have stable value and yield. The combined amount is 51% of the total assets. They comprise 82% of insurance liabilities. It is a slight improvement from 80% in 2021 despite the increased claims in some of its locations. Indeed, IGIC maintains viability, liquidity, and sustainability.

Cash And Investments And Insurance Liabilities (Yahoo Finance)

Stock Price Assessment

The stock price of International General Insurance Holdings, Ltd. remains in an uptrend. It is consistent with the solid fundamentals and can be attributed to recent share repurchases. At $8.24, it is 5% higher than the starting price, showing a stable increase. Despite the higher price, the stock stays reasonable. The price-earnings multiple of 5.9x adheres to the reasonability of the stock price. With my estimated EPS of $1.48-1.5, the stock price may increase to $8.78-8.90. The tangible book value of the company adheres to it. TBVPS amounts to $8.07 versus $7.99. It is also better than the $7.36 average since its IPO. It may show a slight overvaluation with its PTBV multiple of 1.02x. But it is way better than the average of 1.2x. If we focus on the book value, the PB multiple will be 1.00x. Using the average PTBV, the target price will be $9.89, a 20% upside in the next 12-18 months.

Meanwhile, dividend payments are continuous, showing its commitment to shareholders. Annualized dividends are impressive, with yields of 2.67%. It is way higher than the S&P 600 and NASDAQ average of 1.42% and 1.34%. However, if the current quarterly payment of $0.01 continues, yields may drop. It is possible because the company plans to expand in Bermuda and Scandinavia. It may focus on spending on M&A before raising dividends. Thankfully, the company has adequate cash reserves to keep paying dividends. Also, the dividend payout ratio remains low at 3%. My EV model estimation agrees with the price metrics, given the target price of $8.42. There may be a 2% upside.

Bottomline

International General Insurance Holdings, Ltd. maintains stable growth and margins. It also holds adequate cash reserves and can expand without raising financial leverage. Its zero financial leverage means the company can focus on dividend payments. Also, the stock price stays reasonable with an attractive upside. The recommendation is that International General Insurance Holdings, Ltd. is a buy.

Be the first to comment