Sundry Photography

A lot of investors thought Intel Corporation (NASDAQ:INTC) was a 2023 turnaround story, but the chip giant still hasn’t hit bottom. The company faces economic and market headwinds along with pressure from stronger competitors, leading a massive lowering of expectations for this year. My investment thesis remains Bearish on INTC stock, even on the dip below $28 in after-hours trading.

Horrible Quarter

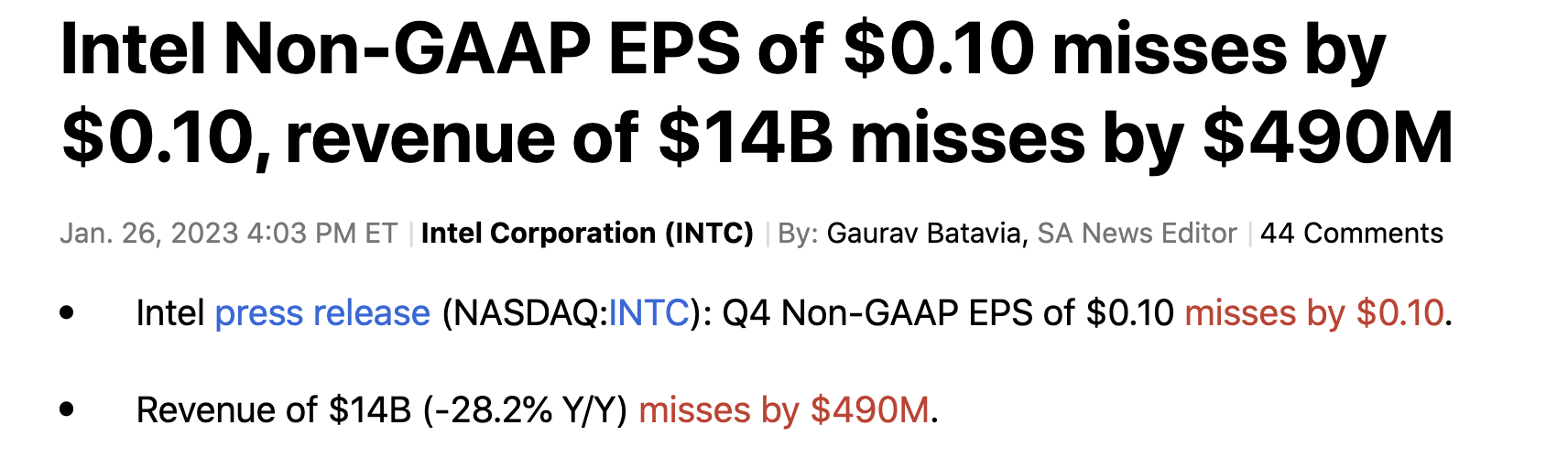

Intel forecast a weak quarter in Q4 2022, yet the company couldn’t even hit those targets. The chip giant missed analyst sales targets by nearly $500 million, with revenue falling 28% YoY.

Source: Seeking Alpha

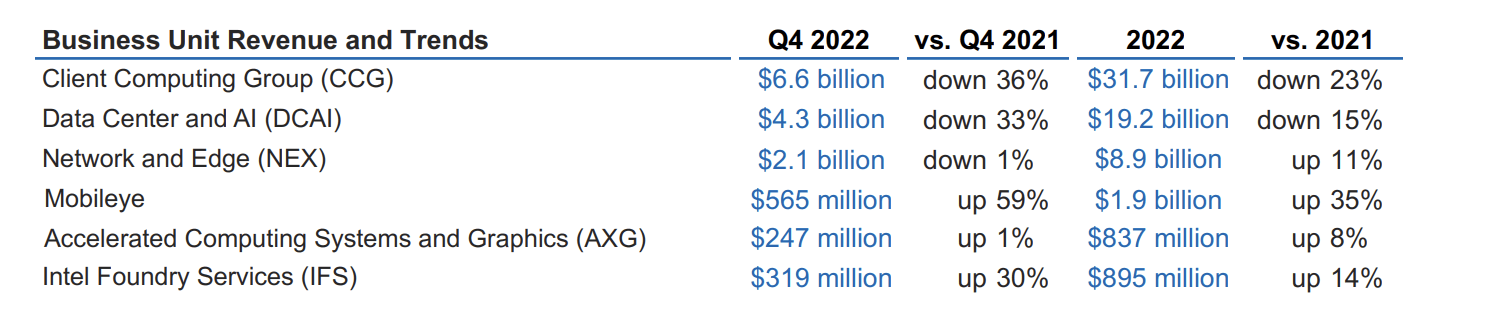

The troubling part for the business is that the PC markets were weak, leading to the Client Computing Group revenues falling 36%. The Data Center and AI sector remains hot, but Intel reported sales falling 33% YoY to only $4.3 billion. Advanced Micro Devices (AMD) continues to take market share in the Data Center area, leading to this revenue dip.

Source: Intel Q4’22 earnings report

Oddly, the most promising unit was Mobileye Global Inc. (MBLY), where Intel just IPO’d the business. The auto tech business grew at a 59% clip, but the company guided to sequentially down revenues in the 1H of the year.

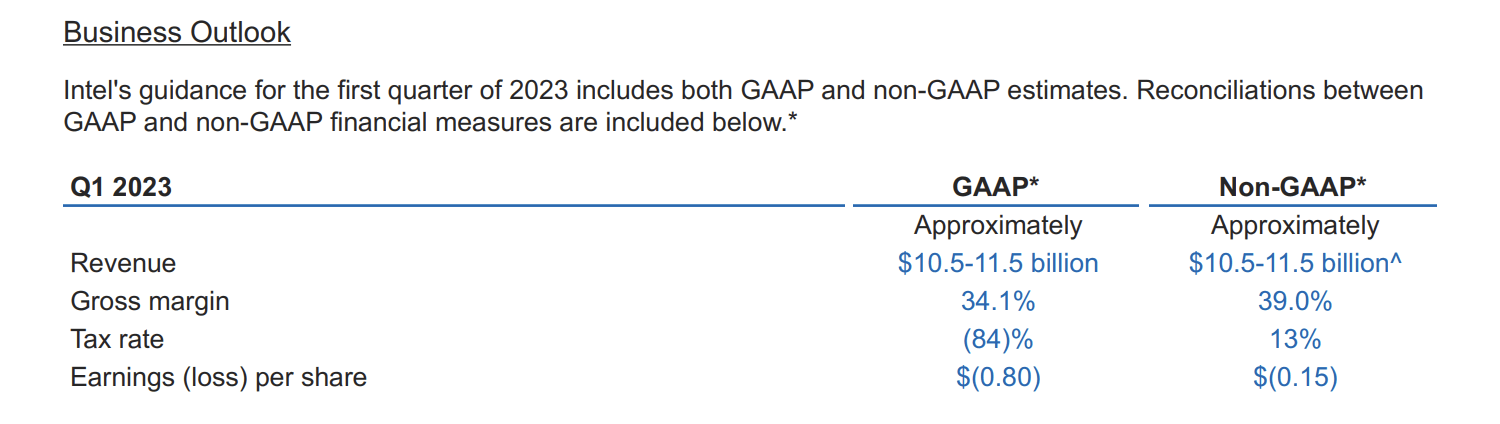

The most disturbing part of the earnings report was the Q1’23 guidance. The company forecast revenues of only $11.0 billion when analysts forecast revenues sequentially flat at $14.0 billion. The company was forecast to watch revenues slide 24% for the quarter, and the target is now a massive 40% dip from $18.35 billion last Q1.

Source: Intel Q4’22 earnings report

The troublesome part is the gross margins dipping to only 39% (3 points higher due to accounting changes on depreciation), when Intel use to generate margins toping 60%. The chip giant actually forecasts a $0.15 loss for the quarter, placing the quarterly dividend of $0.365 at risk, though the company reaffirmed the next payout on March 1.

Management notably left out cash flow and capex guidance for Q1’23 and full-year guidance. Intel has cash of $28.3 billion, while debt levels are already up at $42.1 billion. Intel has a huge capex plan in the process to build up the foundry business that only had $319 million in Q4 revenues.

No Guaranteed Rebound

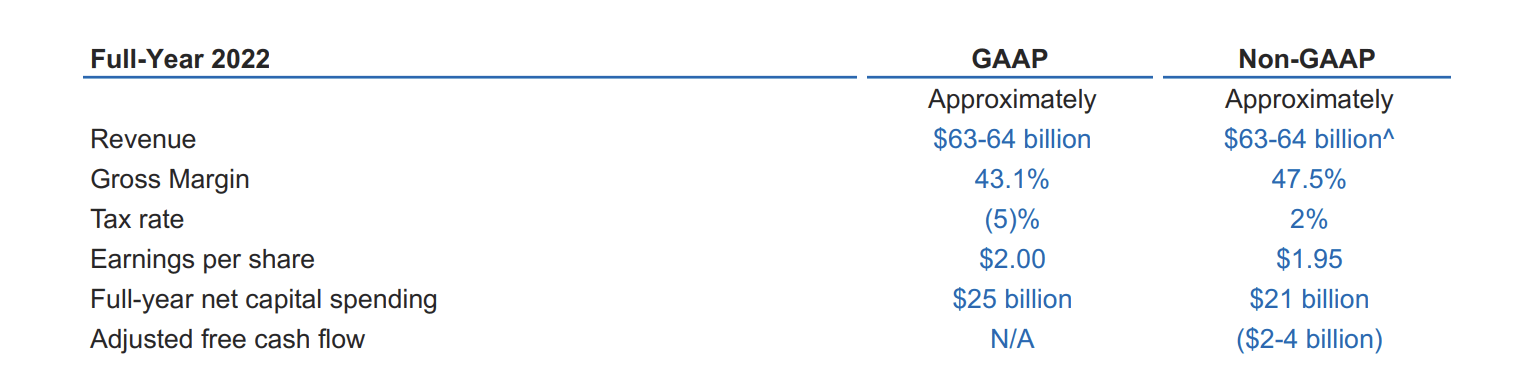

Intel is cutting $8 to $10 billion in annual costs by 2025, and catching up to AMD while eliminating such costs appears very difficult. The chip giant had previously guided 2022 to a free cash burn of up to $4 billion, and the big miss for the year suggests a bigger cash flow loss.

Source: Intel Q3’22 earnings report

Cash flow from operations in 2022 was $15.4 billion, while capex was estimated at $21.0 billion after government subsidies and funds from an investment partner, down from a nearly $25.0 billion spending level. Since operating cash flows will be substantially lower, Intel must either cut capex dramatically or the company will see a huge cash burn in the year.

After all, Intel started last year generating $18+ billion in quarter revenues, and the company is starting 2023 off at a level of only $11 billion. The chip giant still has to cover $6 billion in annual dividends this year while burning cash at an alarming rate.

Even at the after-hours price, Intel still has a market cap of over $110 billion. The company doesn’t even generate profits anymore, and strong competitors like AMD are taking market share during a difficult chip environment.

Source: Seeking Alpha

The big unknown is the more normalized earnings when the economy rebounds and chip demand stabilizes. The general analyst consensus was for Intel Corporation to earn somewhere around $2 per share over the next couple of years. The stock trades below $28 in after-hours trading, still leaving the P/E multiple at nearly 14x EPS targets that must be dramatically cut.

Takeaway

The key investor takeaway is that PC demand will likely increase from these levels after inventory reductions end. The question for investors is how much of the rebound is captured by Intel Corporation with strong competitors in the CPU and GPU space.

Investors must avoid the chip stock until Intel Corporation management stabilizes the business while facing an issue of constant revenue cuts when cutting so many costs.

Be the first to comment