JasonDoiy

We remain bullish on Intel (NASDAQ:INTC) post-earning results. We expect the worst of the macroeconomic headwinds and inventory correction cycles in both PC Client and data center markets to have been priced into the stock. Our bullish sentiment is targeted at the long-term investor; we believe INTC stock provides a favorable risk-reward for investors as the weakness has been priced in, and we see green shoots in the company’s foundry business toward 2025.

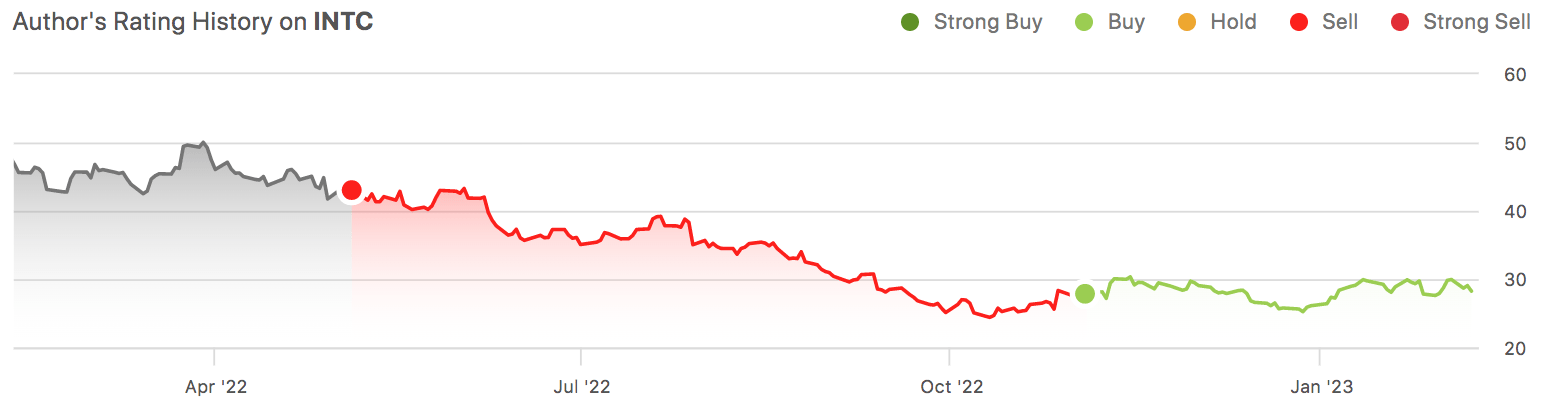

We upgraded INTC from sell to buy in early November based on our belief that the weakness was getting factored into the stock and INTC’s financial performance would stabilize in 2023. The following graph outlines our rating history on INTC over the past year.

SeekingAlpha

Our bullish sentiment hasn’t been shaken by the company’s miss on 4Q22 expectations on EPS and revenue or the grim outlook for 1Q23. We expect INTC is slowly hitting its turning point, with the stock down 43% over the past year and inventory correction cycles nearing their end in both PC Client and data center markets. We believe the industry rebound narrative in 2023, coupled with INTC’s new product, Sapphire Rapid server CPU, and its process node roadmap toward 20A will further improve INTC’s position in the industry. We expect the stock price to remain volatile in the near term, and hence channel our buy recommendation at long-term investors.

Weakness priced in, turning point in FY2023

Our bullish sentiment on INTC is not because we believe the stock will skyrocket in the near term; instead, it’s based on our belief that the worst of the macroeconomic headwinds are priced into the stock at current levels. INTC’s revenue declined 28% Y/Y in 4Q22, and the company expects to see further sequential declines in its core businesses: client computing, data centers, and network/edge sales. While the outlook for 1Q23 is grim, we believe this is the sign that INTC is passing through the eye of the storm and is now better positioned to grow meaningfully in the mid-to-long term. Our bullish thesis on the stock can be broken down into the following points:

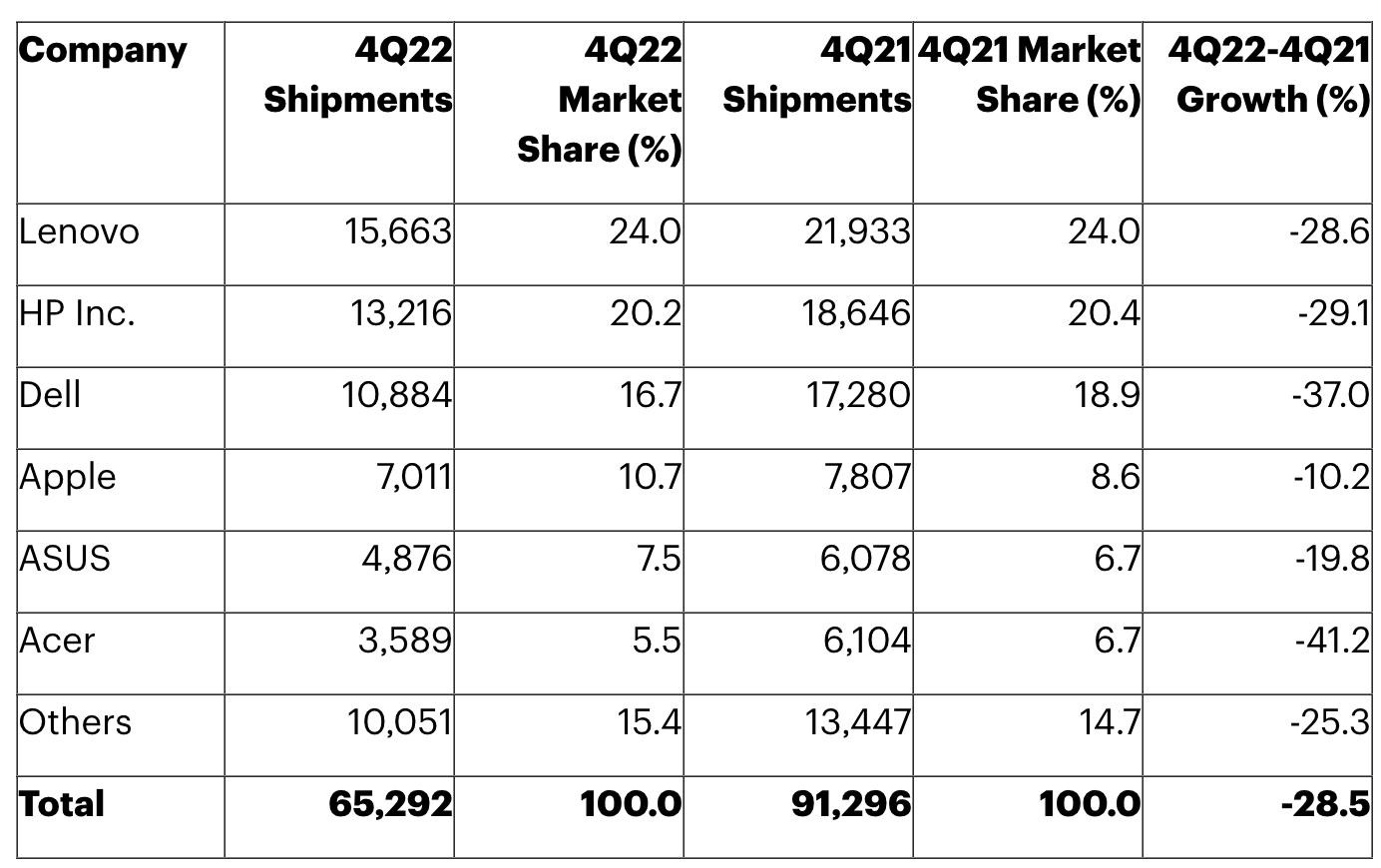

1. PC Client is still sluggish but recognized

Weaker PC demand from the post-pandemic environment in 2022 has spilled into this year, but we believe what’s different about this year is that we know the PC market is suffering, and so does INTC. According to Gartner, 4Q22 marked the largest sequential shipment decline since the company began tracking the PC market almost 30 years ago. Still, PC shipment levels of 2022 beat pre-pandemic demand levels. We believe it’s all really about perception, and we believe INTC is better positioned than it was this time last year because the weak demand has been priced into the stock and the outlook. We believe the company is being more realistic in the PC TAM expectations for 2023. INTC had originally forecasted the PC TAM to be between 270-295M and now expects it to be on the lower end of this range. We also expect the PC Client inventory correction cycle to end toward 2H23 as suppliers work through the high inventory levels built up from pandemic demand levels. The following table outlines the estimates for 4Q22’s lower PC unit shipments going out from PC vendors in thousands of units:

Gartner

We expect inventory correction in the PC Client to be completed toward 2H23 and believe this will improve demand levels for INTC toward 2024.

2. Data Centers & market share to AMD

On the data center front, we expect softer cloud spending in 2023 due to the harsh macro environment; with Canalys reporting the quarterly growth rate for cloud infrastructure services slowed from 34% in 1Q22 to 23% in 4Q22. We’re constructive on the weakness of the data center demand being priced into the stock, along with the broader macroeconomic headwinds. While share loss to Advanced Micro Devices (AMD) has been a pressing issue for INTC, we believe INTC’s new “Sapphire Rapid” server CPU is well-positioned to stamp further share loss to AMD in the server market. We believe the company’s 4th generation Xeon Scalable processors, code-named Sapphire Rapid, will fuel INTC’s turnaround and enable the company to moderate any share loss to AMD even during the softer spending environment.

3. Foundry player in the making

INTC’s IDM 2.0 strategy has put it at the forefront of the transition to move chip-making to the U.S., and part of our bullish thesis is based on our belief that the company will become a meaningful foundry player in 3-4 years. The company’s foundry business generated $319M this quarter, a 30% increase Y/Y. We believe INTC is progressing well in its process node roadmap toward 20A in 2025. INTC’s chips are getting smaller to keep up with Moore’s Law; in 2024, INTC will transition from classifying process nodes on a nanometer-scale to with angstroms. The 20A node will be the industry’s first 2nm-class node to be launched, and we expect the rebranding that comes with 20A will drive INTC into the “angstrom era.” We believe the change in transistor structure opens up a larger possibility for INTC to become a meaningful foundry player in the industry.

Valuation

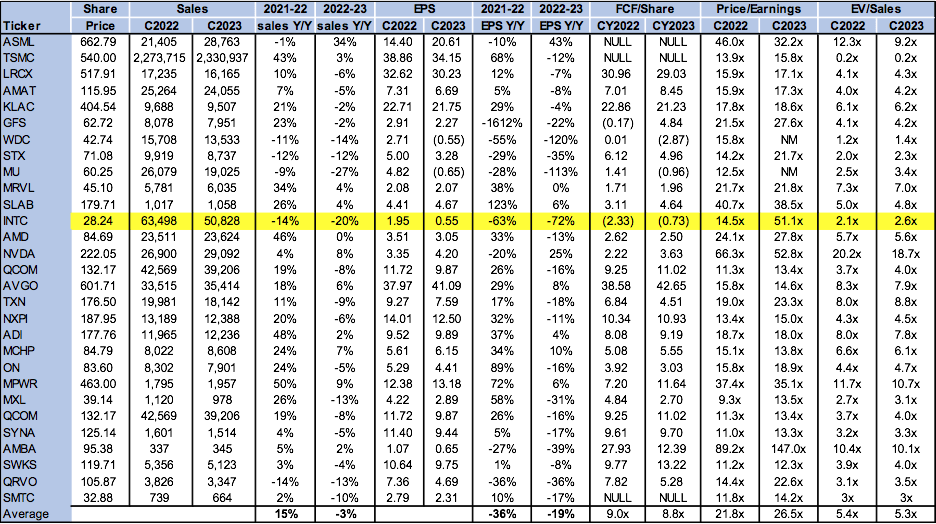

INTC trades at relatively expensive metrics; 51.1x C2023 EPS $0.55 on a P/E basis compared to the peer group average of 26.5x. The stock is trading below the peer group on an EV/Sales metric, trading at 2.6x C2023 versus the peer group average of 5.3x.

The following table outlines INTC’s valuation compared to the peer group.

TechStockPros

Word on Wall Street

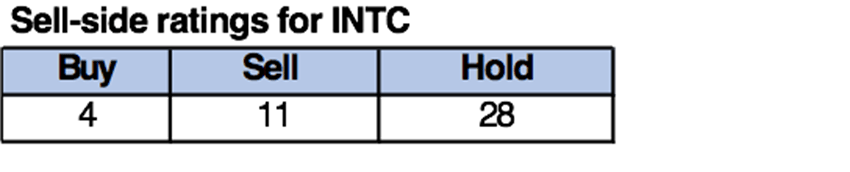

Wall Street doesn’t share our bullish sentiment on the stock. Of the 43 analysts covering the stock, four are buy-rated, 28 are hold-rated, and 11 are sell-rated. We believe Wall Street’s bearish sentiment is based on a near-term outlook for the stock’s performance and is overly pessimistic given INTC’s outlook for 1Q23. Our analysis, on the other hand, focuses on the stock being an attractive investment for long-term investors based on the weakness being priced into the stock at current levels and INTC’s foundry plans in the U.S.

The following tables show the sell-side ratings for INTC.

TechStockPros

What to do with the stock

We recommend that long-term investors look for an entry point for INTC stock at current levels, as we believe the stock is hitting a turning point. We believe the worst of the macroeconomic headwinds have been priced in and expect the inventory correction cycles on both PC Client and data center fronts to be over by 2H23. We’re constructive on INTC’s outlook, factoring in the weak demand environment, and believe the company is better positioned to improve its financial performance in 2023. We believe INTC is also well-positioned to become a meaningful foundry player by 2025 with its process node roadmap toward 20A. While the stock price remains volatile amid market uncertainty, we believe investors buying the stock at current levels will be well-rewarded in the long term.

Be the first to comment