Chip Somodevilla/Getty Images News

Intel (NASDAQ:INTC) is about to report its Q4 earnings results later today after the market closes and it should shed a light on whether Pat Gelsinger’s plan of reinventing the company and restoring its leadership position in the semiconductor industry after years of disappointments is viable. The expectations from Intel for Q4 are already low so the company has a decent chance of beating its estimates and restoring investors’ confidence in its ability to turn things around. As we all await the results, this article will highlight the latest developments and outline whether now is a good time to add the company’s shares to your portfolio.

Can Pat Gelsinger Turn Things Around?

Last year I’ve already covered Intel’s business here on Seeking Alpha and noted how the company lost its leadership position in the CPU and foundry businesses due to a series of flawed decisions that eventually led to technological stagnation and helped enterprises like AMD (AMD) and TSMC (TSM) to rise to greater prominence. Intel’s disappointing performance in the first half of 2022 showed that the rapid depreciation of its shares in recent quarters was justified since it wasn’t able to deliver on its promises at that time. However, there are reasons to believe that in the following quarters, Intel’s CEO Pat Gelsinger might finally be able to turn things around and set the business on the path to recovery.

The IDM 2.0 vision that was presented by Pat Gelsinger more than a year ago focuses on fixing the company’s business processes to ensure that Intel is able to achieve the results that would help it to regain its former glory in the semiconductor industry. During the first phase of this new plan, Intel’s management was focused on investing in a proper roadmap that would be able to help the business to regain its transistor leadership, automate itself, and scale the manufacturing capacity of its foundry business. As it was doing so, it was nearly impossible to deliver the aggressive returns that the street had wanted. The good news though is that everything could change going forward.

During the latest conference call for Q3, the management stated that Intel is now moving into the second phase of IDM 2.0 which will decide whether the business would be successful in executing a proper turnaround and regaining investors’ confidence. One of the major turning points of this stage of IDM 2.0 is the deployment of EUVs for Intel 4 and 3 to improve the transistor performance per watt and density and help the business to achieve its goal of five nodes in four years. Intel is already progressing towards high-value manufacturing of Intel 4 and if successful, it would be able to try to regain its leadership in the industry by 2025.

While it makes sense for a lot of investors to be pessimistic about IDM 2.0 and Pat Gelsinger’s ability to turn things around, there’s one big reason why Intel could actually pull things off and finally deliver on its promises this time. Unlike a year ago, now there’s a great interest by Western governments to secure supply chains for the semiconductor industry and decrease their reliance on China. One of the most efficient ways to do so is by pouring public funds into federal programs that incentivize the return of manufacturing back to home. The passage of the CHIPS Act last year is a clear signal to all businesses that the U.S. government is open to financing major projects that create jobs at home in an industry that’s important to national security.

Thanks to the passage of the CHIPS Act, the U.S. government could become one of the main financiers of Intel’s transformation at a time when it needs the most support. During the latest conference call, Intel’s management already noted that the U.S CHIPS Act and its EU alternative give the company a lot of flexibility on how to grow the business and execute the transformation plan. We could safely assume that Intel would be able to at least offset costs to build new fabs, get additional tax benefits, and boost its R&D yield, all of which could help it to make an IDM 2.0 vision a reality.

While Intel hasn’t received any public funding yet, it’ll likely start collecting checks later this year as there’s an indication that it could get over $20 billion across CHIPS Act and FABS Act or even more if Europeans accelerate their plans to secure supply chains for their semiconductor industry.

Is Now A Good Time To Buy Intel?

The street expectations for Intel for Q4 are already relatively low, which could give the business the ability to beat the estimates and give investors additional hope. It’s likely that the market has already priced in a Q4 revenue decline of 23% – 28% Y/Y to $14 billion – $15 billion that the management has guided due to macroeconomic headwinds. As such, any improvement from this forecast can temporarily push the stock higher after results are revealed. The only thing that matters at this stage is how big of an upside Intel’s stock could have in case of a successful performance in Q4.

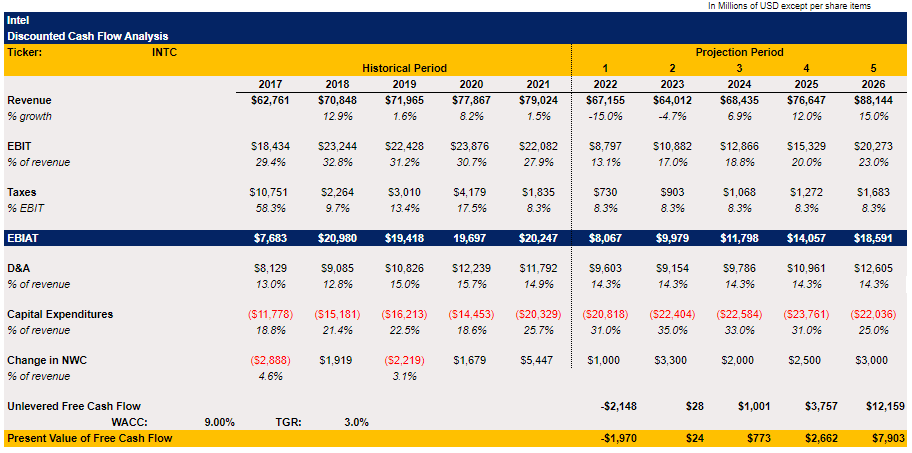

My DCF model below aims to answer that question. For the following years, my top-line and EBIT assumptions are mostly in-line with the street consensus expectations. Over time, earnings in the model improve as the management has guided several times that the savings plan coupled with efficiency efforts should improve profitability over time. The tax rate is the same as during the latest historical period since it’s still unclear how big of an effect the CHIPS Act could be on reducing overall taxes in the following years. The D&A in the model is the average of previous years, while the change in net working capital is positive as was the case in recent years.

The capital expenditures in FY22 stand at $21 billion, in line with the management’s forecast, while in FY23 it increases to 35% of revenues, in line with the management’s expectations that were noted during the latest conference call as well. After FY23, the CapEx starts to decelerate to 25% of revenues in the terminal year, also in line with estimates. The WACC in the model is 9%, while the terminal growth rate is 3%.

Intel’s DCF Model (Historical Data: Seeking Alpha, Assumptions: Author)

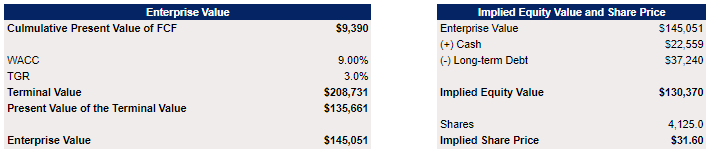

My DCF model shows that Intel’s enterprise value is $145 billion, while its fair value is $31.60 per share which indicates an upside of 6.4% from the current levels.

Intel’s DCF Model (Historical Data: Seeking Alpha, Assumptions: Author)

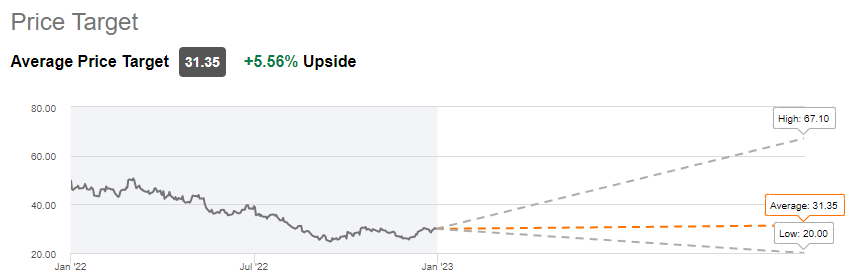

My price target is also close to the street consensus price target of $31.35 per share.

Intel’s Consensus Price Target (Seeking Alpha)

As we could see, the model shows that at the current levels, Intel still has an upside left. At the same time, a potential increase in sales, improvement in profitability, and a decrease in capital expenditures due to a more efficient allocation of capital all could make the upside even more significant than it seems today. Let’s not forget that it took AMD about 5 years to turn things around and become a force to be reckoned with in the semiconductor industry. Intel could be at a similar inflection point today and could yield significant returns for patient investors in the years ahead. However, the road won’t be easy whatsoever, and don’t expect any major returns in the next year or two at the very least.

Risks To Consider

Despite all the things stated above, there’s still no guarantee that Intel is at an inflection point and only the Q4 report would be able to give us a better understanding of whether Pal Gelsinger’s plan is deliverable. At the same time, while I’m more optimistic about Intel at the current levels, there’s still a possibility that the business could fail to deliver on its promises as was the case countless times in the last decade.

Let’s not forget that the company stumbled to went from 14 to 10 nanometers on time, which led to a significant loss of market share and forced Intel to play a catch-up game with its competitors. The latest data indicates that AMD would be able to capture more than 30% of the server CPU market this year thanks to the recent release of the 4th generation of its EPYC Genoa CPU. The same is also true for TSMC, which is ahead of Intel in technology and is on track to build and new fab in the United States faster than Intel, which shows that it would be harder for the latter to regain its dominance in the semiconductor industry anytime soon.

At the same time, due to the weak PC market, the street expects Intel to have another year of Y/Y revenue decline in 2023. Add to this the fact that Intel’s FCF is expected to be negative $2 billion to $4 billion in 2022 and neutral in 2023 and it becomes obvious that there’s a risk that the dividend could either be cut or fully eliminated to get better financial flexibility during this transformation phase. This is something to keep in mind before investing in the company, as that could actually be the only option left if Intel once again stumbles to achieve its goals.

The Bottom Line

Considering all of this, I’m more optimistic about Intel’s future in comparison to a year ago when the business continued to decline and lose market share while its stock was trading at exuberant levels. While it’s still too soon to talk about whether Pat Gelsinger will succeed in restoring Intel’s leadership position in the semiconductor industry, the fact that the management has a clear understanding of what needs to be fixed makes me more optimistic about its future.

We could be at an inflection point at this time as Intel could finally start regaining its former glory. The problem though is that there’s still a chance that we’ll see another set of excuses and delays that could destroy the turnaround thesis before the improvement has even started. Therefore, the smart decision right now could be to start accumulating shares and building a position in the company without exposing your portfolio significantly to it and decide whether to add more shares later on depending on how much progress the business will make in the following quarters.

Be the first to comment