JasonDoiy

Back in December, I detailed how there was potentially more pain ahead for shareholders of chip giant Intel Corporation (NASDAQ:INTC). The company’s CFO had issued comments then that suggested street estimates may be too high moving forward, which I thought could lead to a guidance miss at this week’s report. Well, Intel reported its Q4 results after the bell on Thursday, and as bad as they were, things are looking much worse in the current period.

For Q4, Intel came in with revenues of $14 billion. This figure matched the low end of management’s guidance, and was down 28% over the prior year period when excluding the divested NAND business. The street was looking for about $14.5 billion in total sales, the midpoint of guidance, so this end result was an obvious disappointment. The weakness was led by the Client Computing group, which saw revenues down 36% year-over-year, and the Data Center segment that was down 33%.

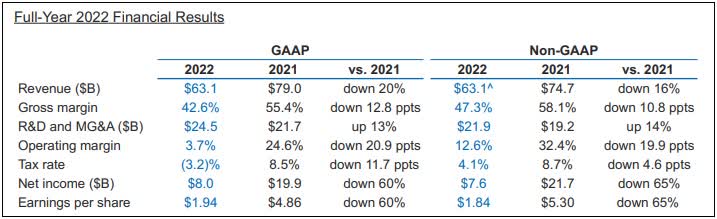

The revenue shortfall led to further pain down the income statement. Gross margins came in at just 43.8% on a non-GAAP basis, more than a full percentage point below guidance. The situation will get even worse moving forward, which I’ll get to, but inventories have certainly surged now. Intel finished 2022 with inventory up $2.5 billion over the end of 2021, despite full year adjusted revenues being down more than $11.5 billion. These numbers finished off a terrible year for Intel as the graphic below details.

Intel 2022 Overview (Company Q4 Report)

The pinch on revenues and margins hurt the rest of the income statement, where management couldn’t deliver enough cost savings. Intel finished last year with an increase of more than 10,000 employees, despite the huge decline in revenues. As a result, the two main operating expenses were actually up $140 million on a non-GAAP basis over Q4 2021. The company’s tax rate also surged unexpectedly, leading to just a dime of non-GAAP earnings per share. That was half of what the street was looking for, with the company actually losing more than $660 million on a GAAP basis.

With all of these results falling short, Intel’s adjusted free cash flow was a negative $4.075 billion for the full year in 2022. This was a negative swing of $7 billion from 2021, and was slightly worse than the bottom end of guidance. While the company isn’t in any financial difficulty currently, cash burn is not a welcome sight when you are paying $6 billion in annual dividends a year. For now, that will mean more debt added to the balance sheet, especially as Intel goes through a major capital expenditure cycle.

Unfortunately, as bad as Q4 results were, guidance was many times worse. I had mentioned in my previous article that Intel’s CFO had talked about normal seasonality in Q1, which usually meant a 5% to 7% decline in revenues from Q4 levels. Going into the report, the street was looking for a little more than a 3% sequential decline to $14.02 billion. However, management is calling for a midpoint of just $11 billion, plus or minus half a billion, which is roughly a $3 billion shortfall against the street. Last year’s Q1 saw $18.4 billion, so this is a dramatic plunge for a company of this size.

With revenues coming in low, gross margins aren’t expected to fare any better. Non-GAAP margins are forecast to be 39% in Q1 2023, down from 53.1% in the prior year period and 58.8% two years earlier. With the company’s chip performance falling behind peers, not only have revenues disappeared, but the company has lost a bit of pricing power. For the bottom line, management is calling for a non-GAAP loss per share of $0.15 in the period, whereas analysts were looking for a 25 cent profit. On a GAAP basis, Intel expects a loss of $0.80 per share. This outlook, especially on the bottom line, looks much worse when you consider the following benefit the company is receiving from a major accounting change it is making.

Effective January 2023, Intel increased the estimated useful life of certain production machinery and equipment from five years to eight years. When compared to the estimated useful life in place as of the end of 2022, Intel expects total depreciation expense in 2023 to reduce by roughly $4.2 billion, including an approximate $2.6 billion increase to gross profit, a $400 million decrease in R&D expenses and a $1.2 billion decrease in 2023 ending inventory values. Intel’s Q1 2023 outlook includes an estimated $350 million to $500 million benefit to operating margin or $0.07 to $0.10 benefit to EPS from this change, split approximately 75% to cost of sales and 25% to operating expenses. The change in depreciable life will not be counted toward the $3 billion in cost savings in 2023 or the $8 billion to $10 billion exiting 2025 communicated at Q3 2022 earnings.

In my previous article, I mentioned how Intel shares could drop to the mid $20s range, which was based on current estimates at that time. Shares did drop to that level before rebounding, but they are now down more than 8% in Thursday’s after-hours session, trading below $28 again. Going into this earnings report, analysts thought the name was worth more than $31 a share, but I believe we’ll see a lot of price target cuts on these results.

Given how bad this guidance was, I now think the mid to low $20s is a range that investors should target if they want to buy Intel Corporation, but I’m not going to put a concrete target on the stock until we see more results in the space so I can value Intel compared to its competitors for this year and 2024. However, it would not surprise me if shares re-test their 52-week lows, unless we get a dramatic market rally next week on a potential Federal Reserve pivot.

In the end, Thursday’s Q4 earnings report for Intel was a true disaster. The company reported a revenue result at the bottom end of its guidance range, which itself was a major disappointment when originally issued. Margins continued to be weak and thus the adjusted bottom line fell well short of estimates. Worse yet, Intel Corporation Q1 revenues are forecast to be much worse than even the most bearish analysts were looking for, and the company is expected to swing to a Q1 loss, even on a non-GAAP basis. With the turnaround here not looking good at the moment, it’s hard to recommend buying Intel Corporation shares unless the price comes down quite a bit more in the coming days.

Be the first to comment