Sundry Photography/iStock Editorial via Getty Images

We had a recent tussle with the Intel Corporation (NASDAQ:INTC) bulls where we pointed out the problems awaiting the stock in 2023. Well, Q4-2022 rolled by and it was not as bad as we feared. It was far worse. We summarize the results for investors and reiterate that we will see $20 before $40.

Q4-2022

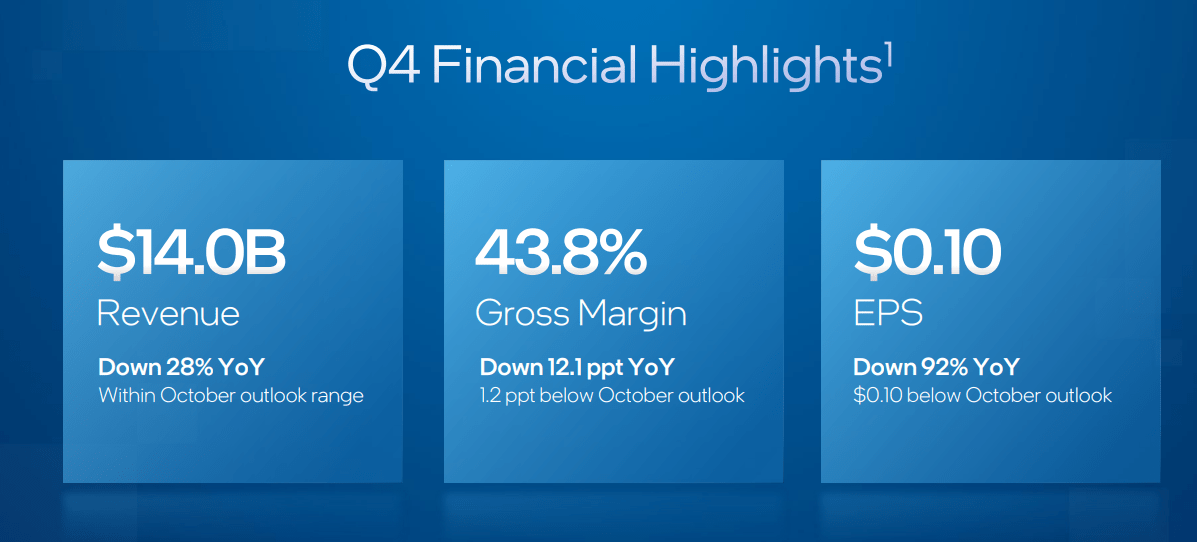

INTC came in at $14 billion of revenues, missing estimates by $490 million. Anyone who knows how the analyst community works should know that they did everything possible to enable a beat.

Seeking Alpha-INTC

Revenue estimates are down 14.43% over the last three months and $100 million lower than what they were when we wrote the last article. INTC still missed in a resounding manner.

What was perhaps more troubling for the long standing bull pen was that gross margins came in at 43.8%. This was the biggest disagreement between our own forecasts and those of the Wall Street analysts.

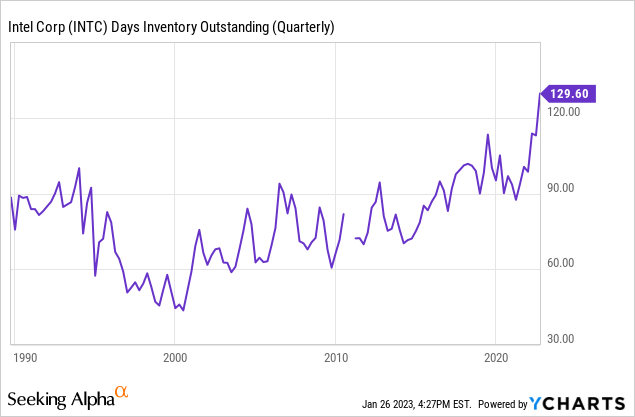

Days of inventory outstanding on the balance sheet looks extremely bad for pricing power. Note that INTC went into the 2001 and 2008 recessions with far less bloat on its balance sheet and it still got creamed.

Source: INTC, $20 Before $40.

This 43.8% in gross margins is right near historic lows despite the quarter that was supposed to create some semblance of a rebound. Earnings came in at 10 cents, half of where they were expected and down 92% year-over-year.

INTC Q4-2022 Presentation

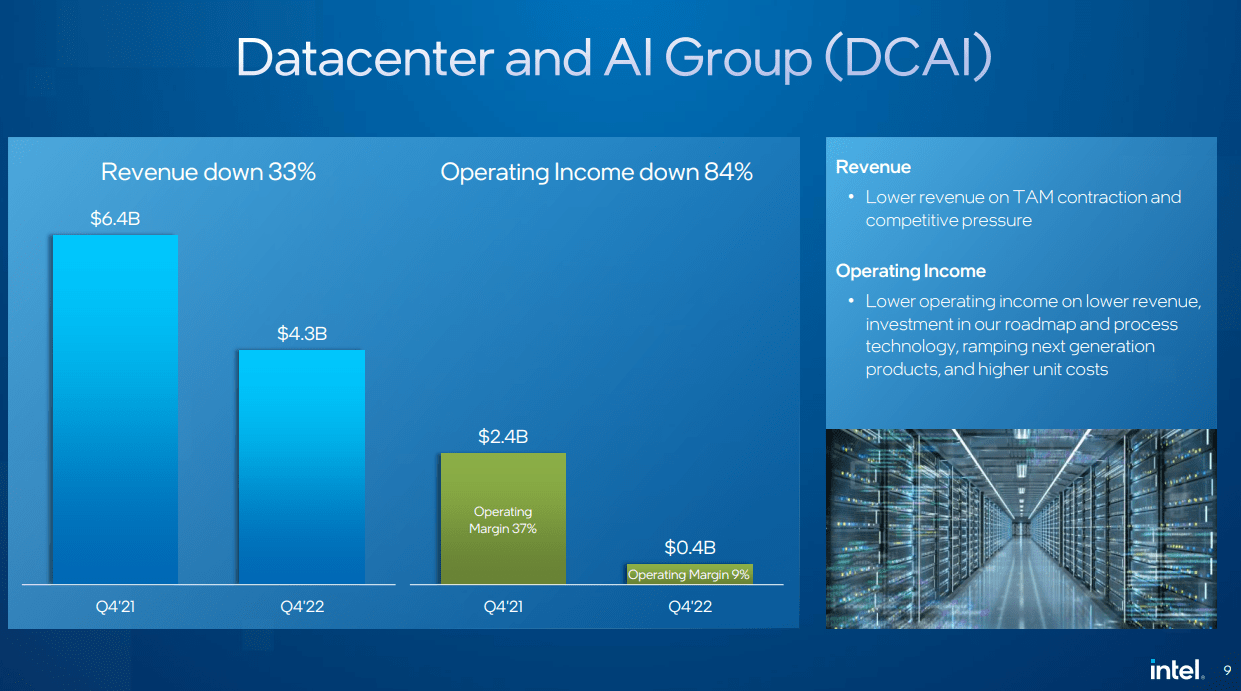

There was blood across all segments, but data center looked the most scary with operating income almost evaporating. That 84% drop shows what happens when INTC faces dual threats of competition and declining revenues.

INTC Q4-2022 Presentation

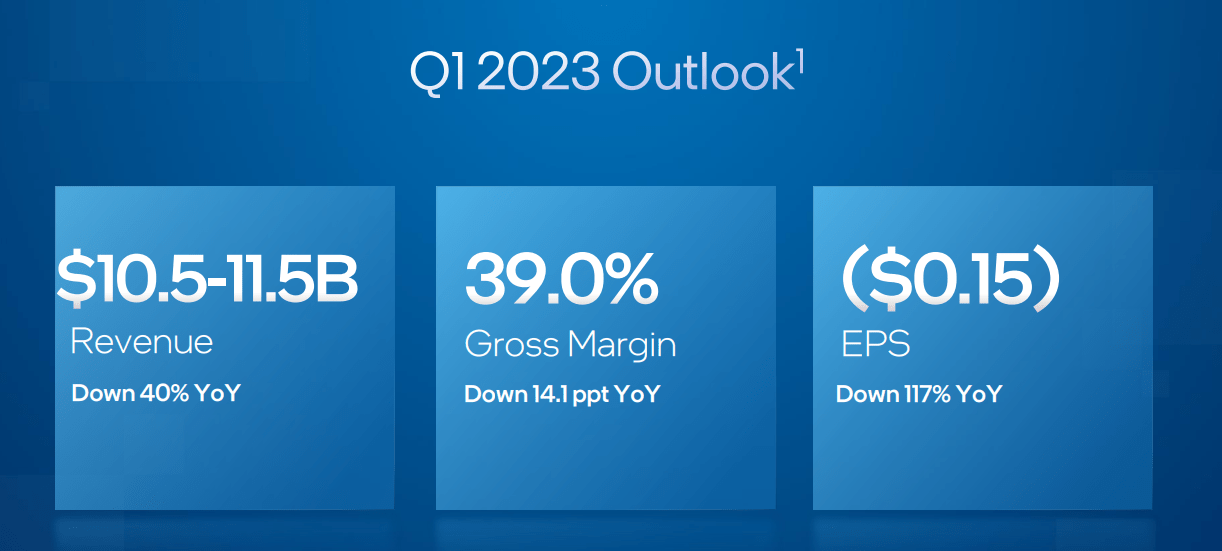

INTC’s woes compounded as it gave guidance for the next quarter. Revenue estimates are down 40% year-over-year. Wall Street is looking for $14 billion in revenues, something we said was not going to happen in this Universe.

INTC Q4-2022 Presentation

Gross margins will drop to 39% and earnings will be a loss of 15 cents a share. A reminder that Wall Street had pegged INTC to deliver 26 cents a share just a week back.

Seeking Alpha – INTC

Even the lowest estimate did not see the possibility of a loss. How could they? Who exactly would have thought that revenues would drop that low? We were arguably the most bearish and had felt a $12.5 billion quarterly run rate would be the trough. This is far, far worse. Even that 39% gross margin estimate looks incredibly optimistic. INTC is doing the low 40s in gross margins with a $14 billion run rate. So with revenue another 20% lower gross margins are likely to drop more.

Verdict

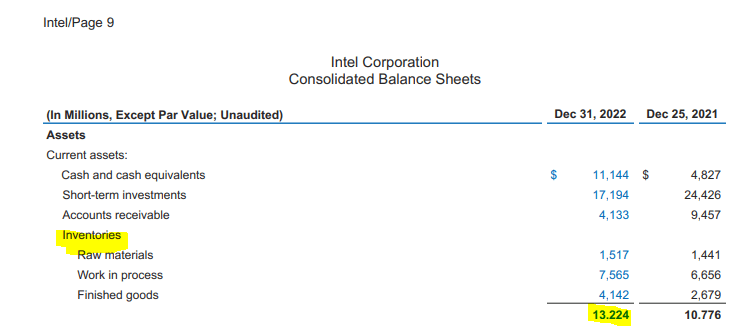

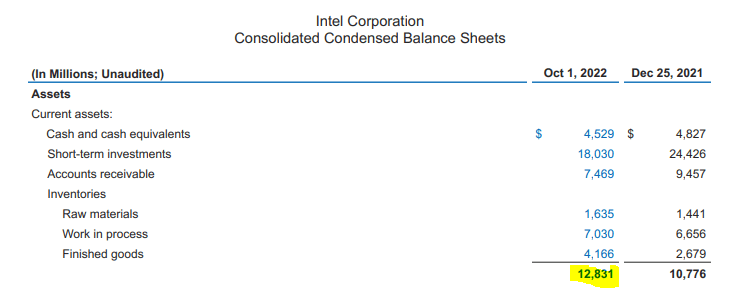

We still have not started the recession and INTC’s model is under extreme stress. As bad as this quarter was, it was made worse by inventories moving up. Total inventories were at $13.22 billion on December 31, 2022.

INTC Q4-2022 Press Release

Last quarter we saw $12.8 billion.

INTC Q3-2022 Press Release

When you combine this information with the forecasted drop in sales, guess what happens to the days of inventories?

You are going to need a bigger chart.

Based on this new information, we see almost a 0% probability that INTC’s dividend will survive mid-2024. With losses as far as the eye can see and a massive capex cycle still in its early days, INTC’s cash burn will reach a fever pitch in 2023. Rating agencies will be having the tough talk within two to three quarters. We think the Intel Corporation downside is still substantial and investors should not fall for the “priced in” concept. $15 before $40 is the new verdict.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Be the first to comment