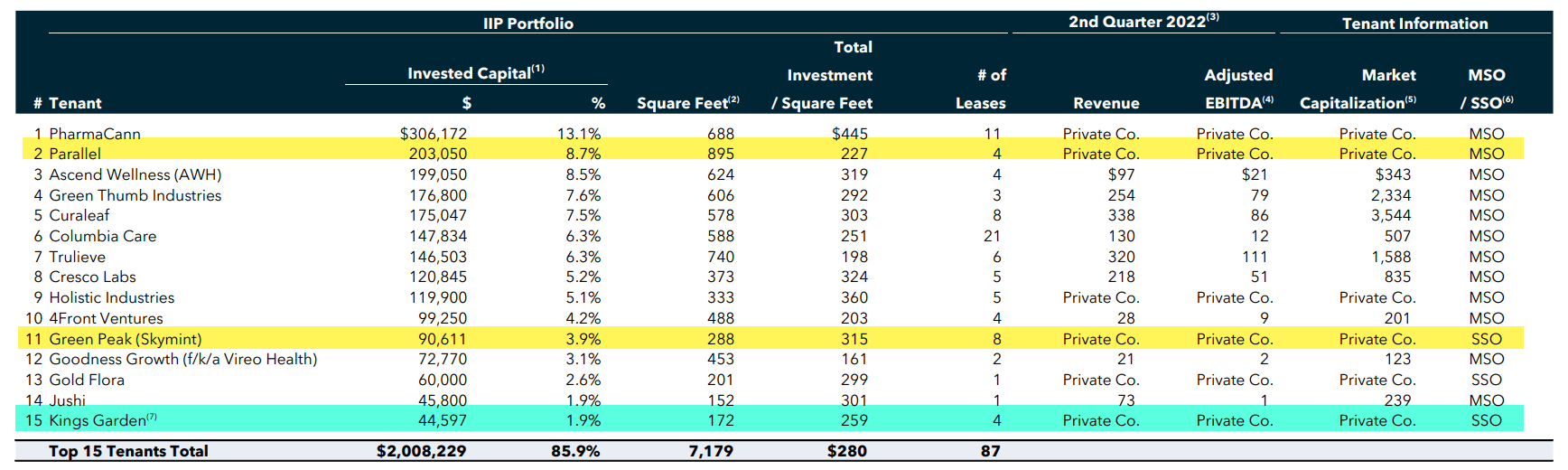

valentinrussanov/E+ via Getty Images

Last week Innovative Industrial Properties (NYSE:IIPR) announced several defaults related to the cannabis REIT’s 111-property portfolio:

- SH Parent, Inc. (Parallel) was in default on its obligations to pay rent at one of IIPR’s Pennsylvania properties (approximately 2.9% of invested / committed capital). Rent was paid in full through January 31, 2023 on all other IIPR properties leased by Parallel.

- Green Peak Industries, Inc. (Skymint) was in default on its obligations to pay rent at one of IIPR’s Michigan properties under construction (approximately 2.7% of invested / committed capital). Rent was paid in full through January 31, 2023 on all other IIPR properties leased by Skymint.

- Affiliates of Medical Investor Holdings, LLC (Vertical) were in default on their obligations to pay rent at IIPR’s California properties (approximately 0.7% of invested / committed capital).

While this news was unexpected, it was somewhat overshadowed by the news in the release related to Kings Garden.

- Kings Garden is paying rent for the four properties in California that it continues to occupy, including rent on the capital invested in the expansion project which is a part of the lease of one of the properties (this project is included as construction in progress below).

- For the three months ended December 31, 2022, Kings Garden paid approximately $1.8 million in base rent at these four properties, in addition to reimbursement to IIPR for pro rata taxes and insurance and direct payments for all other property operating costs.

As you may recall, in September 2022 IIPR announced a confidential settlement with Kings Garden regarding its default on contractual rent payments. And in Q3-22, the company said IIPR had regained possession of two properties that were under development. From the release last week:

- San Bernardino property (approximately 192,000 rentable square feet): IIPR is actively evaluating alternative non-cannabis uses for the property due to market conditions in California and changes in the zoning of the property.

- Cathedral City property (approximately 23,000 rentable square feet): IIPR executed a letter of intent to lease the property and is negotiating lease terms with the potential tenant. There can be no assurance that IIP will lease the property on the terms anticipated, or at all.

In short, IIPR management has successfully resolved the defaults with regard to Kings Garden and is now getting tough with two other operators – Parallel and Skymint – both privately-owned operators.

Source: IIPR Q3-22 Presentation

Cannabis Is Not for Everyone

As I explained last week to iREIT on Alpha members, the cannabis sector is a high-risk property category. To illustrate the point, I used the example of OneMain Holdings (OMF), a consumer finance company that generates high portfolio yields, as I explained in a recent article,

“Net interest margin remained strong at 18.1% in the quarter and the overall portfolio yield was 22.6%, down 55 basis points sequentially. Net charge-offs in the quarter were 5.9%.”

In other words, whenever you charge high interest rates – whether it’s for credit-constrained consumers (i.e. OMF) or cannabis operators, there will be defaults. That’s just a fact!

Granted OMF charges 18% to 40% for the use of their money, and cannabis companies charge around 14% to 18%, the basic math suggests that there will be defaults and the most successful firms will be able to manage such risks. As Howard Marks said, “manage risk is what separates the best from the rest”.

Now, the key to IIPR’s success is rent collection, and as I see it, the announcement last week was simply a shot across the bow to both Parallel and Skymint to either pay rent for the Pennsylvania and Michigan properties or a lawsuit will be filed. Period!

Keep in mind, the leases have corporate guarantees, and they enjoy a common lender (in Canada). It appears that IIPR has no interest in restructuring the current credit facilities (with the lender), which would involve tearing up the leases and taking a substantial rent haircut.

Simply put, IIPR said “no way Jose”…

In other words..

IIPR is calling their bluff!

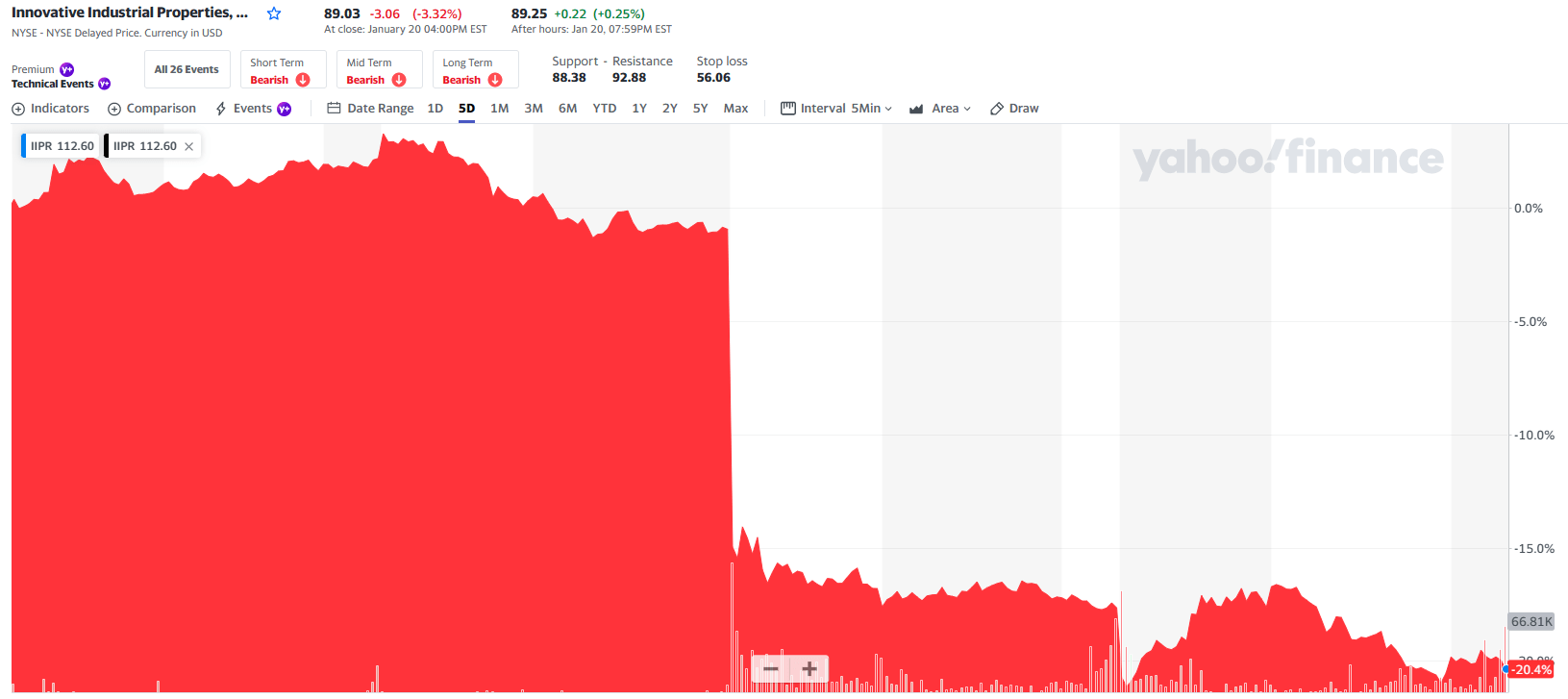

And the medicine was painful (as seen below):

Yahoo Finance

What does this mean?

Keep in mind, there are no federal cannabis laws, so these cannabis operators cannot file bankruptcy…that’s important to know…

So, the options include as follows…

- IIPR could evict their tenant which would include a lawsuit to gain possession of the premises,

- IIPR could also go after the corporate guarantee (which I’m sure they will if they evict the operator from the premises).

How critical are these two properties?

The Pennsylvania property leased by Parallel is located in Pittsburg and is a 240,000 square foot property in which Parallel occupies 100,000 square feet. There is a good chance that Parallel wants to remain in PA since there is a likely recreational (cannabis) vote in 2023 or 2024.

Recreational marijuana became available for legal purchase in New Jersey in 2022 and New York is legal. Maryland should be legal by the middle of 2023.

cbsnews.com

The Green Peak (Skymint) property is 200,000 square feet and located in Lansing, Michigan. The property is located in an industrial park and the building has high ceilings (easier to release).

In addition to Pittsburg, IIPR leases two properties from Parallel in Florida (paying rent) and one development deal in Texas.

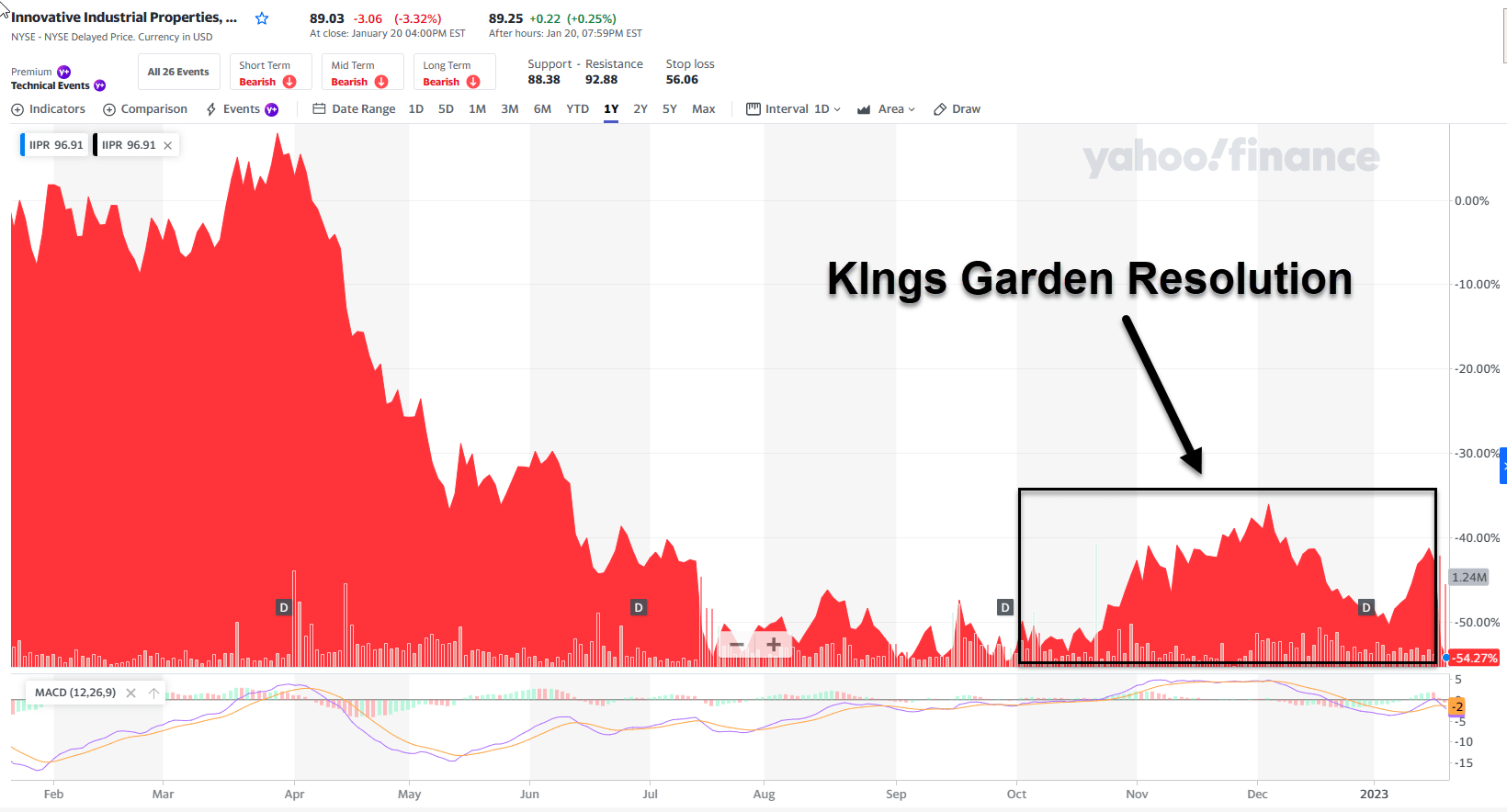

Keep in mind that IIPR’s share price was seeing signs of recovering with the Kings Garden resolution:

Yahoo Finance

Kudos to Management

IIPR’s track record has been exceptional since 2017, generating:

- 137% CAGR net operating income (NOI) growth

- 194% CAGR AFFO growth.

Over the last five years, it’s grown its dividend by a whopping 64% CAGR.

Its capital structure includes just 12% debt to total assets… no material debt maturities until 2026… and a debt service coverage ratio above 15x. And it’s proven it can manage tenant defaults.

The REIT announced on its Q3-22 earnings call that it had collected approximately 97% of contractually due base rent and property management fees associated with its distressed tenant, Kings Garden.

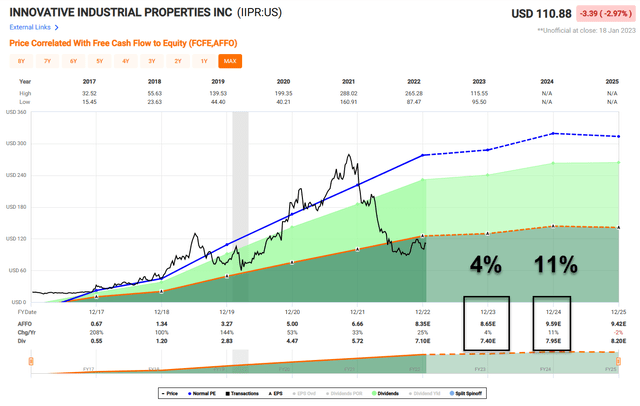

Now, IIPR’s growth has slowed, and analysts expect just a 4% AFFO per-share increase in 2023 and 11% in 2024.

FAST Graphs

Closing Thoughts

It’s also important to note that federal legalization may have chilled, but more states continuing to legalize weed (as I explained above). Both Maryland and Missouri voters approved to-be-taxed measures to allow it for individuals 21 and older.

Ohio and Oklahoma are then set to vote on it this year, and Florida and Nebraska in 2024. Moreover, as more states legalize cannabis, it becomes more difficult for others to resist the potential tax revenue.

Even in my home state of South Carolina, that’s considered one of the most conservative states in the nation, my friend, Representative Nancy Mace is using her clout to help legalize cannabis with a 3% so-called “sin tax” similar to those once in place for tobacco and alcohol.

In effect, the States Reform Act, as the legislation is known, would treat cannabis like alcohol instead of heroin.

Then again, the SAFE banking delays gives it an extended window to grow its business without big-bank competition. Here’s what NewLake Capital (OTCQX:NLCP) CEO, Anthony Coniglio, told me recently,

“…we thought that it would take years and years after passage of that bill for banks to truly be a competitor.”

IIPR’s diversified portfolio also remains a useful advantage, and so does the 85% payout ratio (based on AFFO). Assuming all of the above-mentioned defaults materialize into sustained vacancies, the NOI would drop around 6.3%, putting the payout ratio at ~91%.

Keep in mind, IIPR has security deposits too and if they’re used to pay rent during the cure period, the tenants must re-up the deposits.

Speaking of re-uping, that’s precisely what I did on Friday. While I maintain a speculative allocation in IIPR (and the cannabis sector), I took another bite at the IIPR apple.

Its dividend yield is attractive at 8.1%, and its p/AFFO multiple is 10.7x. While IIPR’s equity multiple is elevated at 9.4x, remember it transacts at low double-digit cap rates. So the deals remain extremely accretive.

Also overlooked in the press release last week:

As of January 18, 2023, IIP has entered into two definitive purchase agreements to acquire two properties for a total aggregate investment of approximately $63.0 million, which includes amounts expected to be made available as reimbursement to the applicable tenants for qualifying improvements to the properties.

As of January 18, 2023, IIP has also executed four non-binding letters of intent to acquire two properties and to make available additional funding for improvements at two of IIP’s properties, representing a total expected investment by IIP of approximately $93.8 million.”

Although the industrial sector is the closest sector peer group, I would discount the valuation since IIPR has significant capital expenditures (‘CAPEX’) invested in its properties. This arguably creates value from a licensing perspective – but does entail high risk if tenants’ default.

Prologis (PLD) trades at 28x, Americold (COLD) at 27x, and Medical Properties (MPW) at 9.6x. Keep in mind, IIPR’s balance sheet has lower leverage than any of these REITs.

In short, cannabis REITs are not for everyone, but if you’re allocating hard earned capital to the sector, I strongly encourage you to visit properties (like we have done at iREIT on Alpha), speak regularly to management (here, here, here, and here), and maintain sound diversification.

I guess we’ll see how the latest news plays out, and although we’re all navigating uncharted waters in the cannabis sector, I like the fact that IIPR’s management team is taking a tough stand, to either pay the rent or get out!

Be the first to comment