Prostock-Studio/iStock via Getty Images

InMode Ltd (NASDAQ:INMD) manufactures and sells minimally invasive aesthetic medical devices for plastic surgery, gynecology, dermatology, otolaryngology (ear nose and throat) and ophthalmology.

Non-invasive and minimally invasive aesthetic treatments like fat reduction, hair removal and muscle tightening rely on the use of medical devices powered by energy-based technologies like radio frequency and laser to achieve results without surgery. Demand for non-invasive treatments is on the rise because, compared to invasive procedures like traditional liposuction, patients don’t need to go under the surgeon’s scalpel. This eliminates the need for anesthesia, removes risk of scarring, and limits downtime associated with invasive surgery.

INMD, which is based in Israel, produces and sells radio-frequency powered medical devices directly to plastic and facial surgeons, aesthetic surgeons, dermatologists and OB/GYNs in the U.S. and other international markets. The U.S. accounted for 64% of its Q2 revenue while international sales accounted for 36% of revenue during the period.

Booming demand

INMD’s customers have a strong incentive to use its products as it helps them tap into the fast growing popularity of minimally invasive and non-invasive cosmetic procedures among patients. In the U.S., which is INMD’s anchor market, the number of skin tightening and fat reduction procedures conducted using energy based technologies increased 128% from 196,105 in 2020 to 391,855 in 2021, according to the data from the Aesthetic Society. The data further shows that total revenue for energy-based procedures, which include treatments like skin tightening, muscle toning, hair removal and vaginal rejuvenation among others, increased by 52% from $1.02 billion in 2020 to $1.55 billion in 2021.

This booming demand for energy-based cosmetic treatments in the U.S. is reflective of the broader global trend. The Global “”Energy-based Aesthetic Devices Market” is expected to grow at a CAGR of 10.2% between 2021-2028, according to business intelligence provider Market Research.

As a market leader, INMD has been a major beneficiary of the growing global demand for energy-based cosmetic treatments.

INMD’s CEO, Moshe Mizrhay, notes that the company had an installed base (basically the number of its devices in use by surgeons and medical experts) of around 14,000 units by the end of the second quarter of 2022. This represents a 20% jump in six month from an installed base of 11,600 platforms as at Dec 31, 2021, as per its SEC filings.

The growth in installed capacity, together with growth in consumables (INMD’s devices utilize consumables that are repurchased by the physicians from time to time), has driven strong financial performance for INMD for the first half of this year.

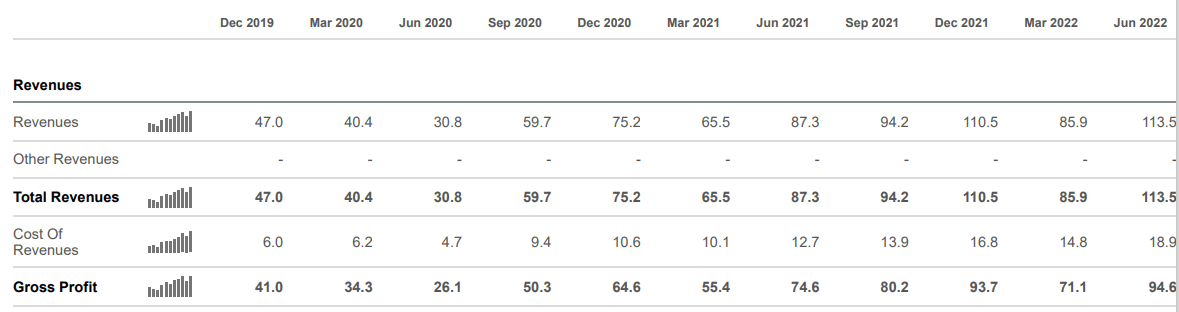

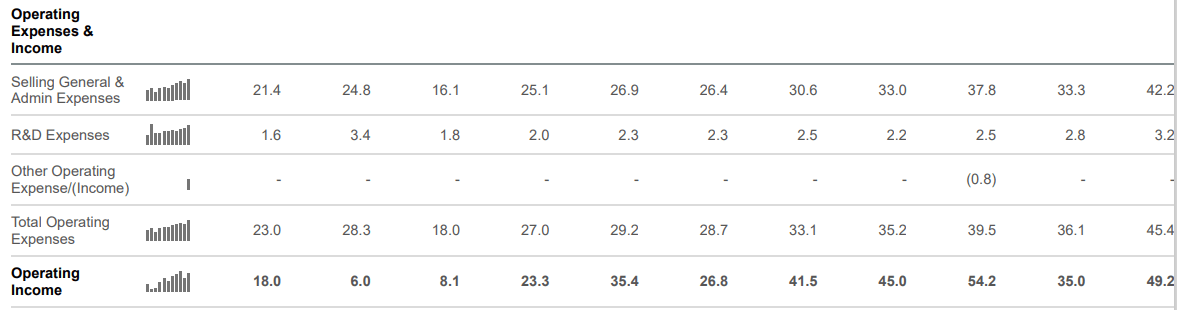

INMD performed exceptionally well in the second quarter, building on already strong Q1 performance. Comparing its latest results to historical results, it’s clear that the company is on a solid growth trajectory in terms of key financial performance metrics such as revenue and operating income. The below highlights, covering the latest quarter and past quarters all the way back to 2019, captures this winning streak.

Quarterly revenue performance since Dec 2019 (millions of USD) (Seeking Alpha)

Quarterly operating performance since Dec 2019 (millions of USD) (Seeking Alpha)

Despite the impressive growth of the underlying business (and the insanely high margins), INMD’s stock has been battered this year. It’s down more than 50% YTD. We, however, view this as a solid buying opportunity and actually recommended it as a good “buy the dip opportunity” in the earlier stages of the sell-off that beset growth stocks this year – in the interest of full disclosure, we’ve been accumulating the stock on most red days in the first half of the year.

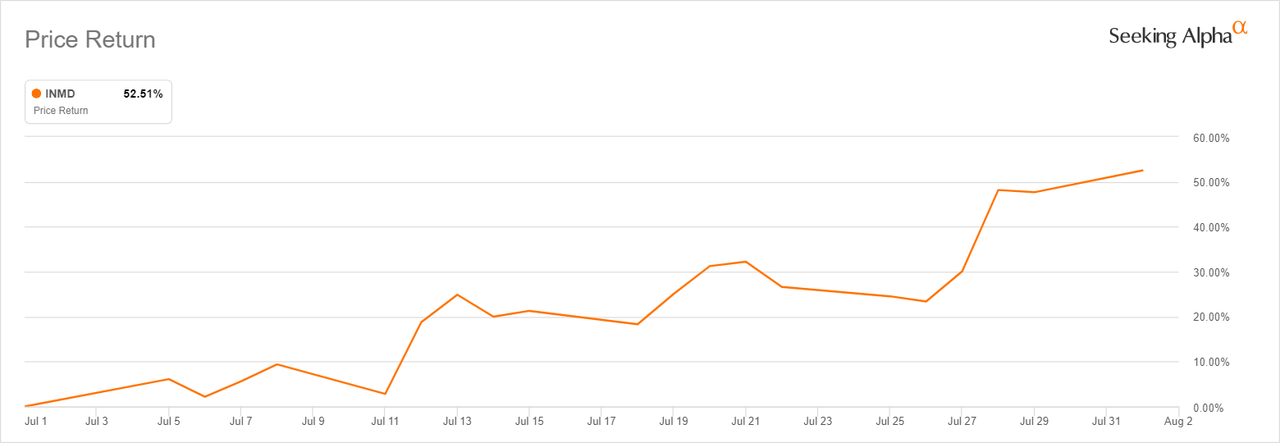

INMD stock is staging a strong comeback

We believe the market has started to see the potential in INMD. If you ignore the horrendous YTD performance and zoom in on its performance since the beginning of the second half of July, you’ll see that it is staging a strong comeback. The stock is up more than 50% since July 1.

INMD stock return since July 1 (Seeking Alpha)

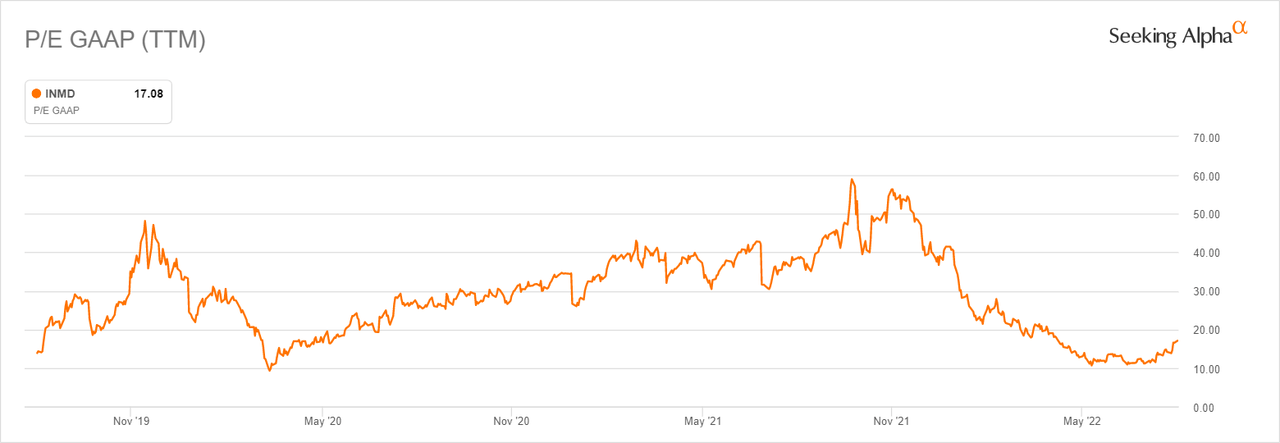

This trend is, in our opinion, likely to hold. INMD’s fundamentals have never been stronger, yet it is still valued relatively cheaply if you look at historical valuation. It is currently trading at around 17x P/E GAAP. The stock has historically managed to hold over 30x P/E for sustained periods of time, indicating potential upside at current levels.

INMD’s historical P/E (Seeking Alpha)

Besides an attractive valuation, INMD’s underlying business is also likely to continue growing robustly. The management raised guidance for FY22. The company raised its FY2022 revenue outlook from $415M – $425M to $425M – $435M vs. consensus of $416.84M.

Key strengths

For those in the bull camp, the key strengths that make INMD a good investment are the continued success of its internationalizations, its ability to successfully launch new products, its incredible economics and the fact that we are still in early days in terms of the growth of the overall energy-based aesthetic devices market.

INMD has in the past few years been able to grow its international revenues significantly. This is critical in reducing the risks of overly depending on the U.S. Its U.S. installed base as per its latest investor presentation was 6600 units against a worldwide installed base of 14,000. This means the U.S. is 47% of its business in terms of unit sales (even though on revenue it’s 64%). This is a clear indicator that INMD has been able to grow its international presence considerably. The company notes its now in a total of 78 countries (U.S. included)

INMD has also successfully launched new products in 2022. The company’s foray into women’s health through the launch of Empower RF, for example, is showing signs of early success; it’s on track to meeting its 2022 targets ahead of plan.

“Our expansion into the women’s health and wellness space is becoming a vital part of InMode’s business. Total sales were originally projected at $20 million for the year but with the current market along with Health Canada’s approval, we are now aiming to reach over $30 million in revenue by the end of the year,” said Shakil Lakhani, President North America, in the Q2 earnings call.

It’s also worth noting that INMD has insanely high margins, with Gross Margins consistently coming in above 80% in the last three years. This is despite unprecedented challenges such as inflation and supply chain disruption that has led to significant cost push across major industries.

INMD further has a net income margin of 42.6% and no long-term debt. INMD today boasts of a $443 million cash pile, up more than double the $193.4 million it had in December 2019.

INMD’s market cap in past three years (Seeking Alpha)

Looking INMD’s the market cap over the past three years, this year’s decline has erased all the gains of 2021. We believe this is an overreaction occasioned by the broader sell-off in growth stocks and that the stock will recover and surpass its historical highs, given the business is fundamentally in its best shape ever.

Conclusion

INMD is attractively valued with significant growth potential. The comeback in the stock starting July 1 is likely to hold and we believe it is a strong buy. The key risk to watch out for, especially as the overall industry grows, is the emergence of stronger competitors. We, however, believe InMode’s high margins give it considerable pricing power.

Be the first to comment