VeselovaElena/iStock via Getty Images

Ingredion Incorporated (NYSE:INGR) produces components used in the food and beverage, paper, and personal care sectors. Its sweeteners, which include syrups, maltodextrins, dextrose, and polyols, make up approximately 35% of its sales. Starches, used in both the food and industrial industries, account for around 45% of sales, with co-products accounting for the rest. About a third of its sales come from specialty ingredients with added value, while the remaining sales come from commodity-grade ingredients. With the majority of its sales taking place outside the United States, INGR operates globally and has significant exposure to growing markets in Latin America and the Asia-Pacific region.

Company presentation

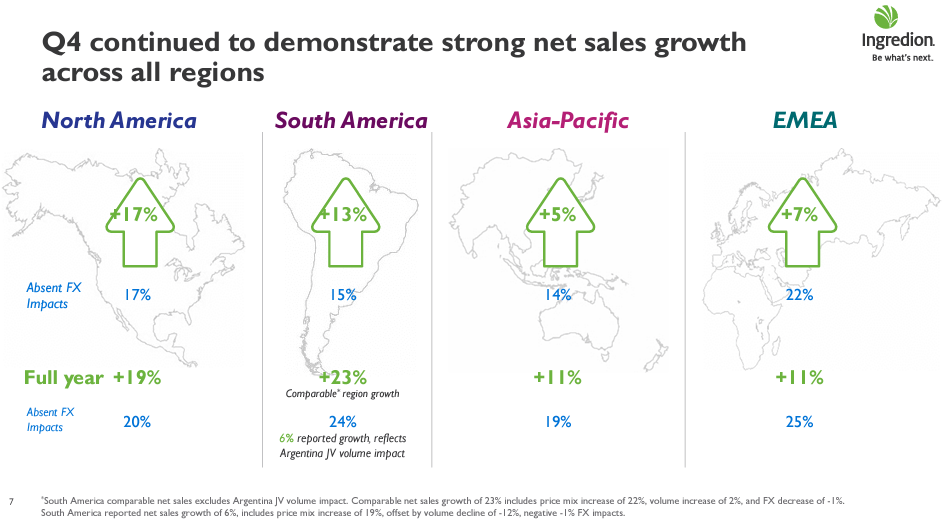

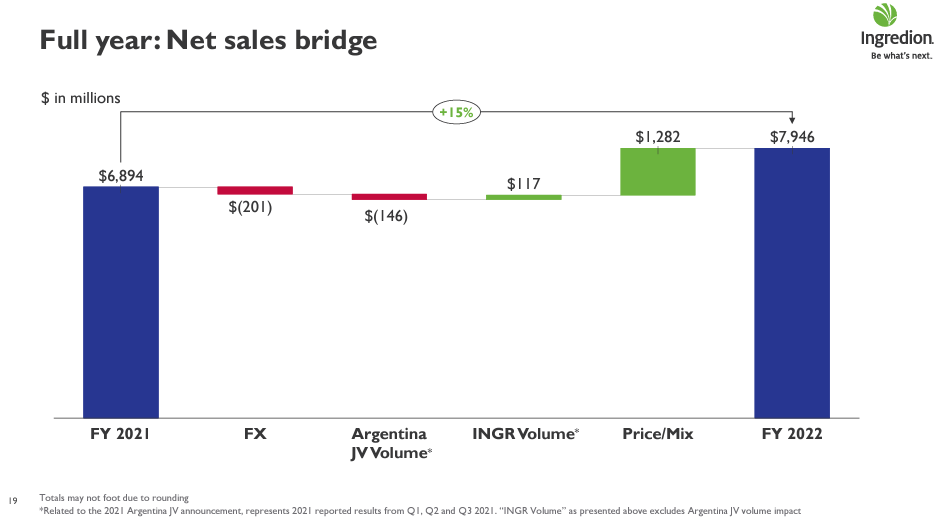

Last year, INGR showed strong pricing power, with prices rising 19% compared to the previous year. This allowed the company to absorb cost inflation and resulted in a 15% growth in net sales.

Company presentation

In 2022, specialty ingredients accounted for 34% of sales and 51% of profits. As demand for specialty starches and alternative natural sweeteners continues to grow, selling a greater share of specialty ingredients should contribute to more steady profit growth for INGR.

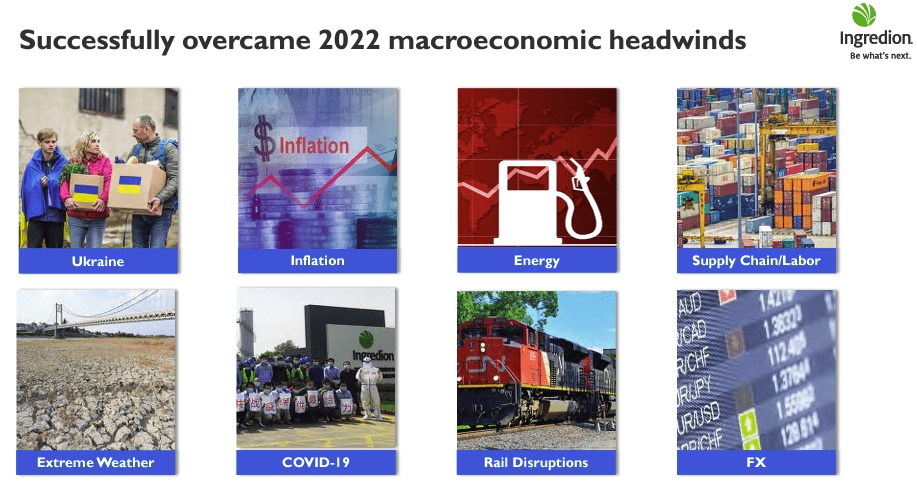

Also, INGR overcame macroeconomic headwinds and secured raw materials despite the impact of the Ukraine conflict and a drought in Europe. The company also successfully offset more than $200 million of foreign exchange headwinds and ramped up production and sales from its new Shandong facility.

Company presentation

INGR Boosts Profits with Focus on Specialty Ingredients for Food and Beverage Industries

INGR is a company that produces starches and sweeteners for the food and beverage industries through the wet milling and processing of corn and other starch-based raw materials. First, the raw materials are steeped in water to extract the desired ingredients. The starches are further processed into various ingredients used by the food and beverage industries.

INGR classifies its products as either core or specialty ingredients. In 2022, specialty ingredients generated 34% of sales and 51% of profits. Core ingredients are commodity-grade and do not offer any pricing power, while specialty ingredients are value-added and command higher prices and margins.

INGR has a global presence, reporting sales from four geographic segments: North America (62%), South America (14%), Asia-Pacific (14%), and Europe, the Middle East, and Africa (10%). Raw materials, including corn, make up half of the company’s unit costs and are purchased at market prices worldwide. INGR hedges against corn price fluctuations in North America to stabilize its margins.

To meet rising demand for specialty ingredients, INGR has been investing in areas such as starch-based texturizers, plant-based proteins, and specialty sweeteners like stevia and allulose.

Competitive Advantage

INGR has a competitive advantage due to its switching costs and intangible assets. Customers are often hesitant to change their product brands, as this would jeopardize their brand equity. Additionally, the R&D spending that goes into creating specialty ingredients results in intangible assets that are difficult to duplicate. With over 850 product-related patents and trademarks, INGR’s offerings are protected from imitation. Furthermore, the company is gradually shifting its focus to its specialty ingredients business through both internal growth and acquisitions.

Based on my analysis, I have estimated the cost of capital to be 7.3% (using an unlevered beta corrected for cash of 0.77). After reviewing the financial statements since 2013, I can see that the return on investment has consistently been above the cost of capital, with an average of 12.6%. This supports my conclusion that INGR has a competitive advantage.

Author calculations & company 10-k filings

Valuation

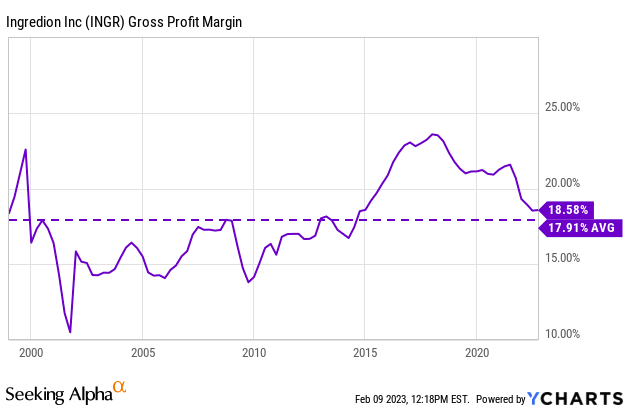

My fair value for INGR is $113 per share. The company has had an average gross margin of 18% since 2000. I believe this will experience an improvement of 500 basis points in the future due to the shift towards specialty ingredients, which command higher margins.

Ycharts

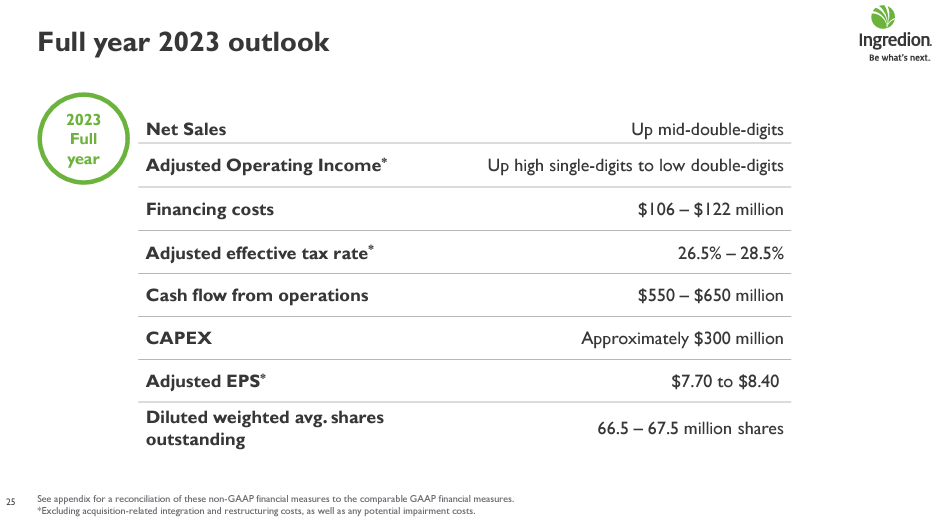

I expect INGR’s net sales to grow by around 13% in 2023, which aligns with management’s guidance. This growth will be partially offset by the decreasing prices of high-fructose corn syrup (HFCS), which accounts for approximately 10% of the sales. The decline in demand for HFCS and the reduction in production volume is expected to persist. In the long-term, I expect growth to converge to 1.7%.

Despite encountering challenges in some key markets, none of INGR’s business segments have reported operating losses since 2010. The company’s North American business has consistently maintained double-digit margins, even during the 2012 North American corn drought, showcasing the company’s strong earnings stability and the effectiveness of its corn input cost hedging strategy.

In 2023, INGR is focused on overcoming similar challenges as in 2022, such as foreign exchange rate fluctuations, inflation, and the war in Ukraine, by expanding its capacity, adjusting its pricing, increasing operational efficiency, and enhancing its risk management practices. The company is also investing in its supply chain and digital transformation to enhance its cost competitiveness, while advancing its sustainability goals, including sustainable sourcing of its five priority crops and reducing emissions.

Below are my main assumptions compared to management’s guidance.

Author estimates & company 10-k filings Company presentation

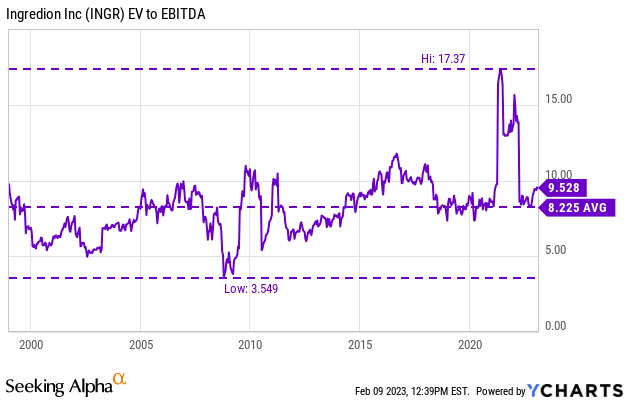

The expected price of $113 per share is based on an EV/EBITDA multiple of 9.9x, which is higher than the current 9.6x and the average of 8.3x. This increase in the multiple is reasonable, given the increasing proportion of revenue from high-margin specialty ingredients.

Ycharts

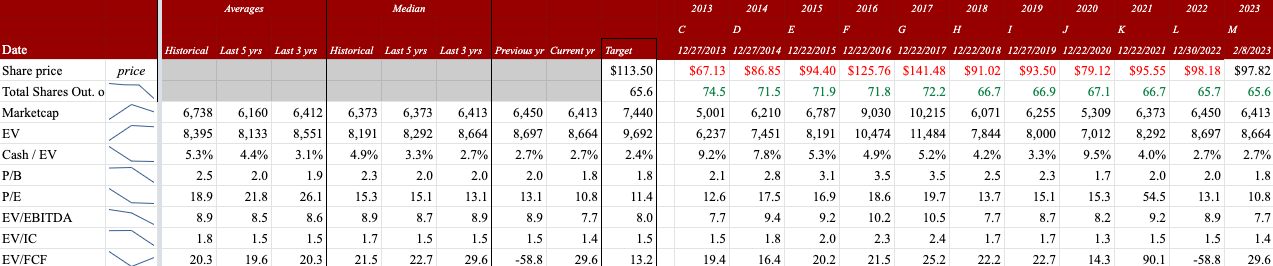

Below are the historical multiples compared to the multiples at the target valuation of $113.

Author estimates, company 10-k filings & Seeking Alpha

Manageable debt and a safe dividend

INGR’s balance sheet is sound. Its healthy balance sheet and manageable debt maturities make it capable of meeting its financial obligations. Net Debt / EBITDA has steadily increased from 1.6x in 2015 to 2.3x in 2022. While 2.3x is still a healthy level for such a company, my projections indicate that the metric would hover around 1.5x in the medium term.

Author estimates & Company 10-k filings

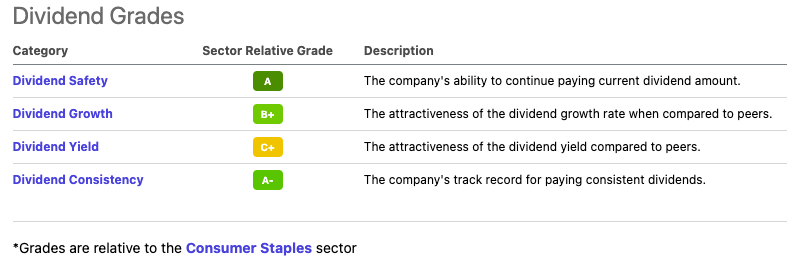

The dividend is pretty safe, it grew slower than the sector median (2.7% vs. 4.7%) and its yield is a bit higher than the sector median (2.7% vs 2.6%).

Seeking Alpha

Risk & Uncertainties

The decrease in demand for HFCS as a beverage sweetener is due to its association with health problems such as obesity and diabetes. About 10% of INGR’s sales come from HFCS.

INGR’s international operations may be impacted by the unpredictable prices of corn and other starch-based raw materials. Despite the growing demand for plant-based protein products, the lower profit margins associated with these ingredients may affect the company’s overall profitability.

INGR is vulnerable to volatile corn prices, and its hedging efforts are primarily focused on North American corn purchases. The spread between cornmeal and soymeal prices also affects INGR’s profits, as the two can be used interchangeably in many products, such as animal nutrition. Consumer preferences can both pose a risk and offer an opportunity for INGR. If the company fails to adapt to changing health concerns and avoid products like HFCS, sales may decline. On the other hand, aligning its portfolio with consumer demand could lead to faster sales growth compared to its peers.

Conclusion

INGR showed strong revenue growth in 2022 by focusing on pricing, and plans to continue this strategy in 2023. With a shift towards higher-margin specialty products, I expect the company’s multiples to expand. At a current fair valuation of $113, the shares offer a potential 15% upside.

Be the first to comment