FeelPic

Infosys Limited (NYSE:INFY) is set to report its earnings on January 12th. Given the weakening macros, I am not too optimistic about the revenue growth prospects. The company experienced exceptionally strong growth over the last couple of years due to an accelerated shift towards digitization. However, with the economy reopening this should start to slow down and I expect revenue growth to revert back to pre-covid levels over the next couple of years. Many companies allocate their IT budgets in the early part of the year and given the significantly weaker macro environment versus early last year, I am expecting a slowdown in new orders. I am optimistic about margin improvement prospects, though. INFY’s margins should benefit from increasing utilization, decreasing subcontractor spend, and weakening Indian Rupee. Additionally, the declining attrition rate should also help margins. The stock is trading at ~21.47x FY24 consensus EPS estimate which is a discount to its five-year average forward P/e of ~23.60x. While I like the margin improvement prospects and lower than historical valuations, I would prefer to be on the sidelines for now given slowing revenue growth.

Revenue Outlook

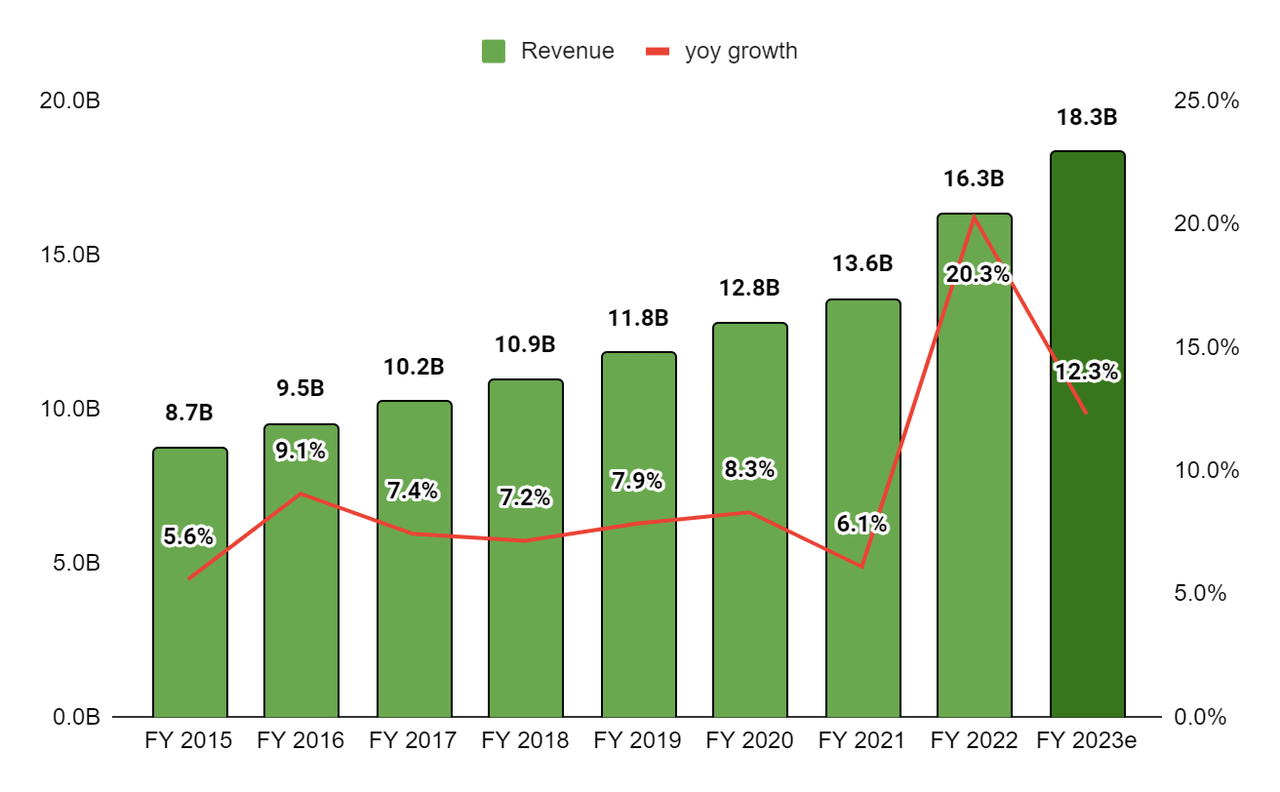

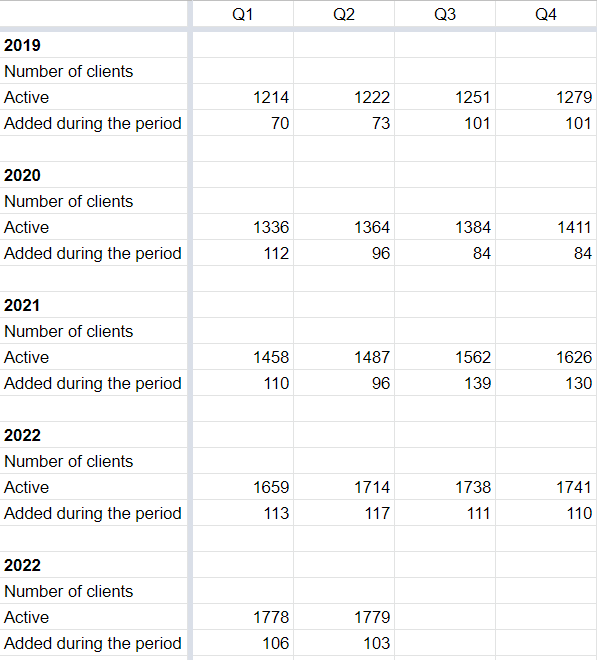

After growing between mid-to-high single digits from FY15 to FY21, Infosys’ revenues accelerated meaningfully in FY22 and the first half of FY23 as the demand for digitization grew due to the lockdowns during the pandemic and the company received a good amount of contracts for its services. The strong demand in its end markets also led to an increase in the pace of new client additions and the number of larger deals over the past few quarters. The company has added 100+ new clients each quarter in the last eight reported quarters. In the second quarter of FY23, the company signed 27 large deals with a Total Contract Value (TCV) of $2.74 bn, with 54% net new contracts.

INFY’s revenue and yoy revenue growth (Company data, GS Analytics Research, FY2023 number are consensus estimates) INFY’s number of clients (Company data, GS Analytics Research)

Looking forward, I expect the order pace for INFY to start slowing down in the coming quarters due to the uncertainty of macroeconomic conditions. On its previous earnings call, management talked about seeing some slowdown in the retail industry, Hi-Tech market, the telecommunications business, and the mortgage business of the financial services segment, especially on discretionary programs. Further, on its earnings call last month, Accenture (ACN) also talked about seeing delays in decision-making across its customers as well as changes in the pace of spending and some pausing in smaller deals.

I believe INFY should also report a similar situation in its upcoming third-quarter earnings call. Most companies finalize their annual IT budgets in January, along with the annual planning cycle. I expect a significant tightening in IT budgets year-over-year given macros and customer optimism are much worse compared to where they were last year.

In addition to worsening macros, I believe the company’s growth should also get impacted by the normalization in demand with the economic reopening. During the last couple of years, many companies had to accelerate their digital transformation to remain competitive in lockdown. For e.g. prior to the pandemic, a brick & mortar retailer might have had plans to deploy its omnichannel capabilities across all geographies over the next several years. But due to lockdowns, it had no choice but to complete this transformation in a much shorter time frame and make sure its digital capabilities are completely rolled out across all geographies. This accelerated transition resulted in a faster order pace for INFY. With the economy reopening now, that urgency is no more there and I believe the big transformational projects might revert back to their historical multiyear timelines. This might result in a much more normalized and “in line with historical” growth rate for Infosys. If we look at the current consensus estimates they are modeling low double-digit growth for Infosys for the next several years. I believe these numbers are likely to prove optimistic and the company’s growth should revert to its historical mid to high single-digit range over the coming years.

Margin Outlook

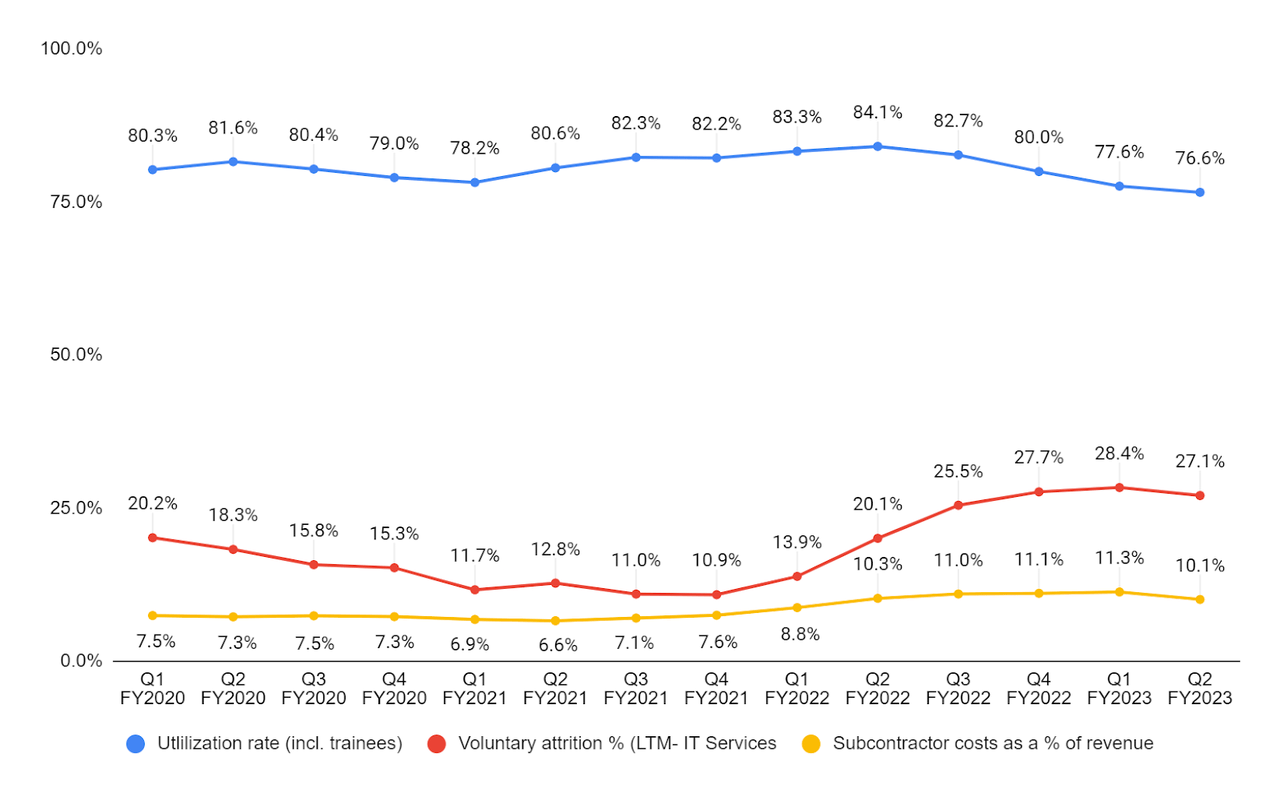

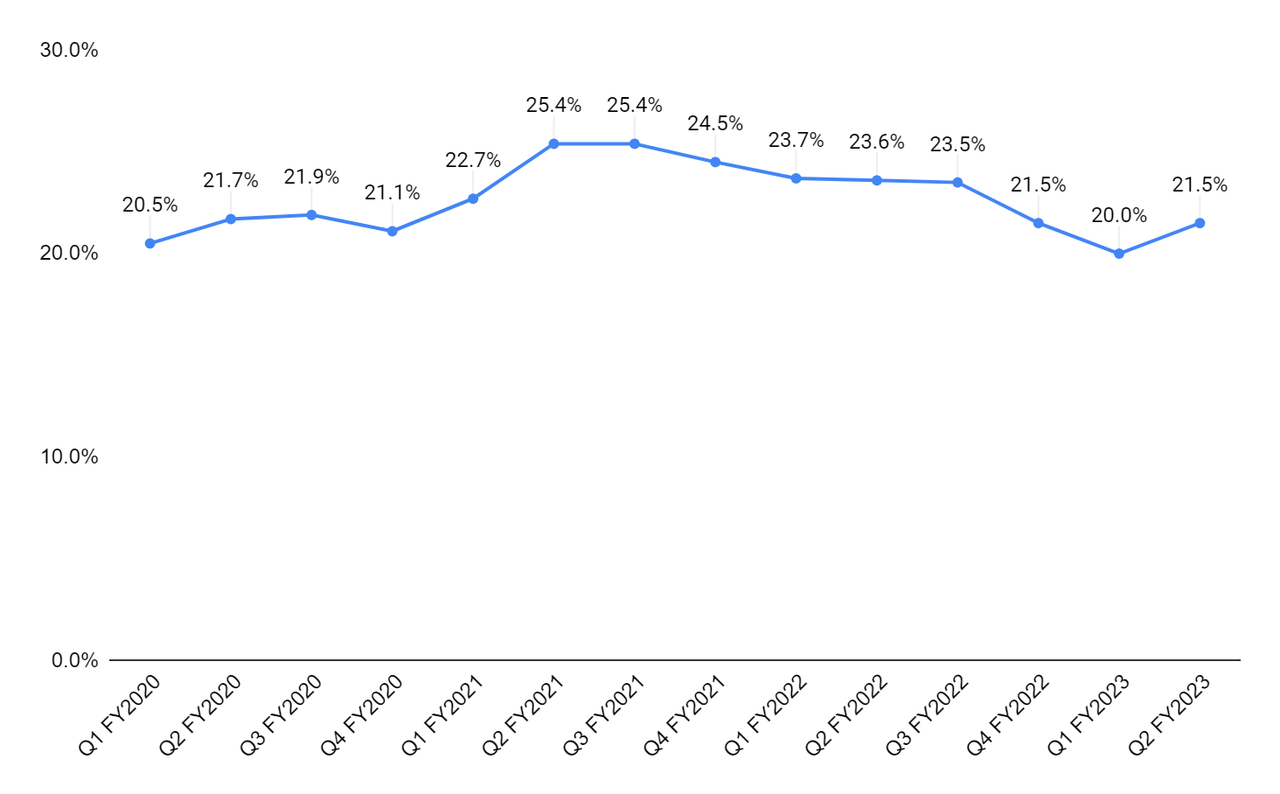

Over the last few quarters, the company’s margins are declining due to the decreasing utilization rate, wage hikes, increase in subcontractor costs, and increased travel following the reopening of the lockdown. Due to the sudden increase in demand, the company started hiring more entry-level employees (trainees) in recent years. There is a gap between hiring and deploying an entry-level employee on a project as these recruits have to undergo detailed training. So, the utilization suffered. Further, since the demand was high, the company had to rely on subcontractors for project fulfillment. This increased the company’s subcontractor costs over the past few quarters, further impacting the margins.

INFY’s utilization rate including trainees, attrition rate, and subcontractor costs as a % of revenue (Company data, GS Analytics Research) INFY’s operating margin (Company data, GS Analytics Research)

Looking forward, management is working on improving utilization and lowering subcontractor costs as a percentage of revenue. As the entry-level trainees hired in recent years are deployed on projects, utilization should improve. Further, their deployment should also reduce dependence on subcontractors, further helping the margins. Employee attrition rate and wage inflation are also expected to reduce given the normalization in IT services demand. Further, the appreciating dollar and declining rupee are usually beneficial for Indian IT services companies that have their vast workforce based in India and clients abroad. While the slowdown in revenue growth is likely to be a headwind, I am optimistic about the company’s margin growth prospects in FY24 and beyond.

Valuation & Conclusion

The stock is currently trading at 24.66x FY23 consensus EPS estimate of $0.72 and 21.47x FY24 consensus EPS estimate of $0.83. Over the last five years, the company’s forward P/E has averaged around 23.60x. While the stock’s FY24 multiple is at a discount to the historical average and I like the company’s margin improvement prospects, the uncertain macros and likelihood of a slowdown in revenue worry me. I would be closely watching management’s commentary over the next couple of quarters to get a better sense of the extent of the slowdown. Till then I prefer to be on the sidelines and have a neutral rating on the stock.

Be the first to comment