choochart choochaikupt/iStock via Getty Images

This article was first posted in Outperforming the Market.

Investment thesis

When I think of the disrupter, I think of indie Semiconductor (NASDAQ:INDI). I like to identify companies that have the potential to take on the current industry incumbents and I think that indie has the potential to gain significant share in the AutoTech semiconductor space. The company brings innovative products into the market and also benefits from strong industry tailwinds like the electrification and autonomous vehicles revolution that will bring content spend and volumes up. In this article, I will also go deeper into the quality of the founder-led management team, which has continued to impress me. At the end of the day, indie also has strong growth visibility given the large strategic backlog that it has.

I have written articles on indie earlier which can be found here. I have also done deep dive articles into indie, looking deeper into its competitive landscape, competitive advantages and valuation, amongst other things, in my investment service, Outperforming the Market. indie is part of The Barbell Portfolio, which members get access to, and indie has helped members get a 25% return so far in 2023.

Understanding the company and its business model

indie’s goal is to provide customers with a comprehensive portfolio of automotive semiconductors and software solutions. It focuses on the fastest growth mega trends in auto which are electrification, ADAS and user experience.

The company uses a fabless business model, enabling the company to be asset-light and minimize capital expenditures while focusing on its core competitive strengths in designing and engineering. The company uses third party foundries to manufacture, assemble and test its products.

indie collaborates with key customers and partners with more than 10 Tier-1 automotive suppliers as its go-to-market strategy. As an approved vendor to several Tier-1 automotive suppliers, its offerings are found in many top automotive manufactures globally. The company has also met the tough quality standards of more than 20 global automotive manufacturers. As a result of innovative products, a differentiated portfolio of cutting-edge solutions, as well as strong engineering and design expertise, indie has been able to ship more than 140 million semiconductor products since inception.

Products and solutions

The current suite of products involves a wide range of automotive applications, ranging from ultrasound for assistance in parking, cabin wireless charging capabilities, infotainment and LED lighting used to enhance user experience, telematics and cloud access for improved connectivity.

Perhaps the products currently under development are the ones that are more exciting as they involve a wide range of products like Frequency-Modulated Continuous-Wave (“RMCW”), LiDAR, radar and vision solutions for Advanced Driver-Assistance System (“ADAS”), to charging controllers, diagnostic platforms and e-fuse chips for electric vehicles. indie intends to have a comprehensive ADAS portfolio, delivering a full suite of system-level solutions that supports all key sensor modalities for its customers.

As such, indie’s key products and solutions focus on three of the mega trends we see in autos today and they are electrification, ADAS and user experience.

The company has a strong design experience and capabilities in things like mixed signal and RF design, analog and power management, Digital Signal Processors (“DSP”), ARM-based Microcontrollers (“MCU”) and system engineering, optimization and partitioning. These capabilities in core technologies allows indie to deliver leading edge AutoTech architectures to customers.

On top of these products, almost all of indie’s products are embedded with automotive grade software solutions and ARM 32-bit processors. indie also enabled algorithm development and co-development with hardware through its own proprietary design flow.

As I will explain below, indie acquired TeraXion in 2021 and the company designs and manufactures innovative photonic components on various technology platforms, including fiber Bragg gratings (“FBG”) and low noise lasers. Thereafter, these components are then integrated into solutions for the laser systems, optical sensing and optical communication markets.

Manufacturing

As mentioned above, indie has a fabless business model and works with its network of third parties that helps to manufacture, assemble and test its products.

The key manufacturing partners that indie works with are X-FAB, ASE Group, Sigurd and GlobalFoundries. indie uses GlobalFoundries (GFS) as its foundry partner for some of its process technologies, including advanced nodes, while X-FAB is contracted for mixed signal and high voltage foundry. indie uses ASE Group for packaging and testing.

By using a fabless business model, indie is able to lower their spending on capital expenditures as well as reduce its fixed costs, while focusing on their engineering and design resources on the company’s own core competencies and let its third-party partners with other competencies do the manufacturing, assembling and testing.

To ensure resiliency in its supply chain, indie has a few partners and sources for each part of the supply chain. The entire manufacturing period takes about 26 weeks, with the process initiated by indie sending a wafer purchase order while forecasting the demand to assembly and test partners at the same time. The latter step is to ensure that indie’s assembly and test partners are able to order the necessary materials and secure sufficient capacity for indie. The assembly process will take another 10 to 15 days while the testing process takes another 7 to 10 days. Once the product is finished, it is than warehoused and shipped to the desired location.

Company strategy

indie’s eventual goal is to have a comprehensive portfolio of automotive technology solutions, with a focus on designing and delivering the technologies that enable the three trends of electrification, ADAS, and enhanced user experience. I highlight the core aspects of indie’s growth strategy below.

A focus on high-growth applications

At the end of the day, the focus of indie is in AutoTech opportunities that benefit from the tailwinds of the three trends highlighted above.

As such, within the AutoTech space, it is focused on the applications that have one of the highest growth rates in the space, while being diverse in the applications it serves, ranging from wireless charging, telematics to ADAS opportunities.

Organic growth through existing and new relationships as well as new product launches

It is pivotal for indie to execute well on its current sizeable existing wins, which I will elaborate below, to show existing and potential customers that they are able to deliver reliably to customers. Furthermore, indie’s products currently support multiple Tier-1 automotive supplier platforms and can have a rather extensive reach to bring in new wins in time to come.

In the medium-term, indie plans to expand on its LiDAR solutions and bring Artificial Intelligence (“AI”) and Machine Learning (“ML”) processor acceleration capabilities into new deployments in radar and vision applications.

Growth through selective acquisitions

Since being publicly listed, indie has selectively acquired companies that it views as bringing a unique opportunity to the company in the long-term. For the pursuit of inorganic growth, indie will only acquire companies that complement its existing portfolio and technology or companies that will speed up their growth plans.

The acquisition of TeraXion in 2021 was one significant acquisition since listing as it adds an innovative laser portfolio to indie’s ADAS solutions. TeraXion’s highly integrated architecture is expected to bring 10 times improvements in system performance and cost, and at the same time, the acquisition expanded indie’s geographical design and development footprint. This acquisition is expected to further solidify indie’s position in the fast-expanding market for LiDar.

Growth through a nimble supply chain and partner network

As elaborated earlier, indie focuses on the engineering and design aspects while it uses third party partners to manufacture, assemble and test. With its network of partner foundries, testing and assembly partners, this enables indie to move quickly to changing market demands and exceed specific customer requests.

The asset-light fabless model has enabled indie to have the distinctive ability to reduce the manufacturing period, thereby bringing industry leading cycle times.

Also, this asset-light model enables indie to be able to scale up rapidly when needed while reducing fixed costs to the minimum. When demand grows and backlog increases, indie can simply scale the business by following the process mentioned above in the “Manufacturing” section above by leveraging on its key third party partners which have their own competitive advantages in manufacturing, assembly and testing.

A margin expansion strategy

The company intends to expand its margins by designing and developing new and more highly integrated solutions. Through continued focus on innovative designs and development, this will enable future margin expansion opportunity as indie creates a suite of portfolio products that are superior to competitors.

This will involve a relentless focus on innovation and research that will hopefully drive improvements on multiple fronts, including performance, efficiency, lower costs and size, amongst others.

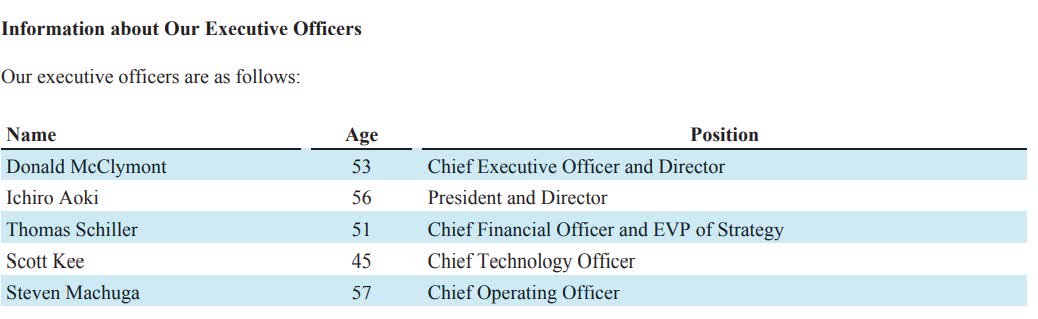

Management

I like that indie is a founder-led company with highly competent executives that have a track record of high performance. On average, each person in the executive team has 17 patents to their name, and 60% of the executive team are co-founders of indie.

The executive team

Executive team of indie (indie 2021 Annual Report)

Firstly, indie’s CEO is none other than Donald McClymont. He is one of the co-founders of indie and is the key person responsible for driving shareholder value, solid execution of business strategy and creating the direction and vision of the company. He was at Axiom Microdevices, which was later sold to Skyworks Solutions (SWKS) prior to the founding of indie in 2007, primarily in charge of building relationships with industry players and implementing the strategy of the company. Prior to Axiom Microdevices, he played roles in companies like Skyworks Solutions, Conexant and Fujitsu. He has five patents to his name and has a Master’s in engineering Electronics and Electrical from the University of Glasgow.

Secondly, Dr. Ichiro Aoki takes on the role of President at indie and plays a key role in the execution of the company’s strategies and its technical roadmaps. Similar to Donald McClymont, he is a co-founder of indie and was also in Axiom Microdevices before the founding of indie, where he played the role of Chief Architect. Dr. Aoki also founded PST Eletronica in Brazil, which was subsequently sold to Stoneridge. He has an amazing achievement of developing 35 patents and authoring several IEEE papers, with more than 400 citations for two of them. He holds a Ph.D. and Masters in Electrical Engineering from the California Institute of Technology and a Bachelor of Science in Electrical Engineering from the University of Campinas.

The last of the three co-founders is none other than Dr. Scott Kee, who acts as indie’s Chief Technology Officer. His key role pertains to strategic product development and alignment of the roadmap. Similar to the other two co-founders, Dr. Kee was from Axiom Microdevices, playing the role of Chief Technology Officer there as well. He was also actually one of the co-founders of Axiom Microdevices. He has 35 patents developed worldwide and has a Ph.D. in Electrical and Electronics Engineering from the California Institute of Technology and a Bachelor of Science in Electrical and Electronics Engineering from the University of Delaware.

Next, we have indie’s CFO and Executive Vice President of Strategy, Thomas Schiller. He is in charge of corporate finance, financial reporting, investor relations and merger and acquisition activities in indie. Before joining indie in 2019, he has experience in Marvell Semiconductor (MRVL) and Skyworks Solutions. He did his Masters of Business Administration at the University of Southern California with a specialization in Entrepreneurship and Finance and he also did his Bachelor of Arts in Social Sciences with emphasis in Economics and Political Science at the University of California, Irvine.

Last but not least, indie’s COO is Steven Machuga who has been with the company since March of 2021. Before coming to indie, he was Vice President of Worldwide Operations at Skyworks Solutions since 2016, demonstrating competency in operations in a large organization, and has more than 30 years of experience in semiconductor development and high-volume operations management of the entire supply chain. Steven has a Masters in Chemical Engineering and Materials Science from the University of Minnesota, as well as a Bachelor of Science in Chemical Engineering, from the University of Connecticut. He also has achieved six US patents and three European patents.

Key takeaways from the management team

After looking at the key personnel that are running the show at indie, I think that there is a strong, quality team with a track record of success at the helm of indie.

This is not just a founder-led management team, which is more likely to take a long-term view and tends to outperform competitors, but also individuals that have experience spearheading large organizations in their past roles or creating value in companies which they join. On top of that, they all have competent industry knowledge, having an average of 17 patents per person amongst the five of them, and have solid academic foundation in relevant fields of study.

While I usually research on the quality and competency of management more to do further due diligence on the company, the pedigree of the executive team at indie leaves me with a higher-than-average level of confidence in the ability of the management team to execute at a high level. I would add that the founder-led, highly competent management team is one of the competitive advantages that will take indie to the next level.

Risks

Competitive pressures

indie is a small player in the AutoTech semiconductor industry. There are currently other players in the competitive landscape with significantly more financial resources that could put more of these resources into research and development efforts. This could reduce the competitive advantage that indie could bring to the market and thereby reduce the demand for and market share gain potential for the company. indie needs to continue to develop better and more innovative products than its larger peers in order to stay relevant and grow.

Funding needs

I am of the view that the company currently has sufficient liquidity to meet its near-term capital requirements. However, it may need to raise more capital to acquire new businesses or to increase expansion into a particular line of product. This may result in potential dilutive risks for current shareholders.

Cyclicality of the semiconductor industry

As the semiconductor industry tends to be cyclical, during periods of downturn or macroeconomic weakness, the semiconductor industry will likewise feel the pain as demand falls and the industry corrects. Given that indie is a relatively small company, it needs to show investors its ability to execute growth even in these down cycle periods.

Conclusion

I think that by understanding a company and its business model, it helps to give investors greater confidence in the company. indie’s goal is to develop a full suite of innovative solutions for customers. The focus here is on delivering a product that is better than what is available in the market, with an innovative mindset. Its fabless business model enables it to use an asset light approach to growing and scaling up, allowing the company to focus on its key expertise in engineering and design. Its strategy for growth, both organically and inorganically, is clear and the company continues to execute its growth strategy to add value for shareholders in the long-term. Furthermore, the deeper dive into management gives me confidence that indie is in good hands as a founder-led management team of high quality. As a result, I am reiterating my buy rating on indie and remain convinced of its long-term growth potential.

Be the first to comment