MmeEmil

Smoking pot is now more popular than cigarettes in the U.S. The trend comes as the Biden Administration moves ahead with cigarette nicotine reduction. Nevertheless, major cig stocks have produced strong relative returns in the last 18 months, along with other names in the Consumer Staples sector. One international brand recently reported its semiannual earnings report, and shares have been on the rise. Are there more gains to come, or is this trade about to go up in smoke? Let’s dig in.

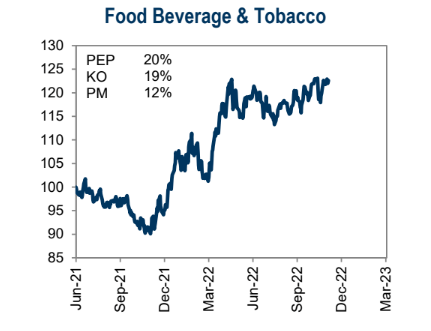

Safety in Staples: Relative Strength in Soda and Cigs

Goldman Sachs Investment Research

According to Fidelity Investments, Imperial Brands PLC (OTCQX:IMBBY), together with its subsidiaries, manufactures, imports, markets, and sells tobacco and tobacco-related products in Europe, Americas, Africa, Asia, and Australasia. It offers a range of cigarettes, fine cut and smokeless tobacco, papers, and cigars; and next generation product (NGP) portfolio, such as e-vapor products, oral nicotine, and heated tobacco products.

The U.K.-based $24.1 billion market cap tobacco industry company within the Consumer Staples sector trades at a low 11.9 trailing 12-month GAAP price-to-earnings ratio and pays a high dividend yield of 6.6%, according to The Wall Street Journal. Broad trends are away from tobacco use, as evidenced by an October report from the FDA that e-cigarettes are becoming more popular than traditional cigarettes. Firms that position themselves to benefit from that switch include Imperial Brands.

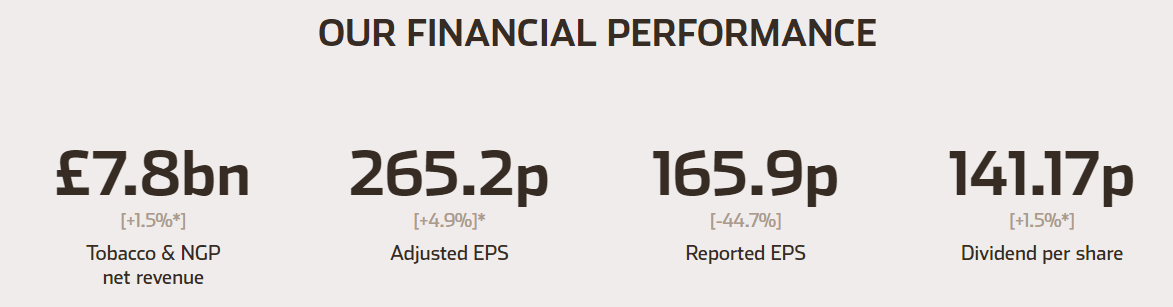

On valuation, Seeking Alpha rates the stock with an A, mainly driven by its relatively favorable EV/EBITDA figures and a low price-to-cash flow multiple. In its recent semiannual earnings report, the firm reported a 1.5% revenue increase and an 18% jump in net cash flow. Those are impressive numbers, though EBITDA was higher by less than 3% (adjusted EPS was +4.9%). Free cash flow was near flat. Overall, I think the P/E is priced about right considering tepid growth, but cash flow appears strong enough to support the yield. The stock, which trades at a discount to its sector, could also be a safety play in a recession. Finally, a reversal lower in the dollar should help the company.

Annual Report Figures

Imperial Brands

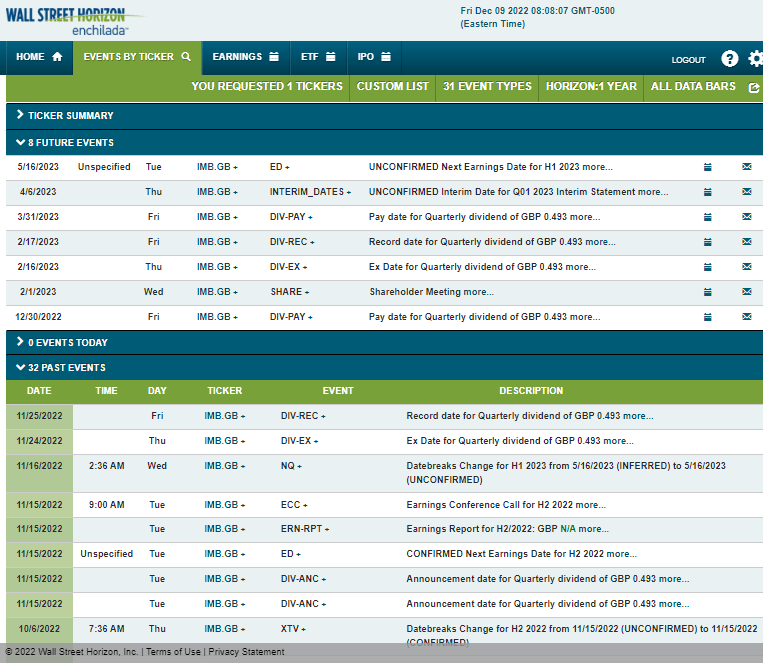

Looking ahead, corporate event data from Wall Street Horizon show an unconfirmed H1 2023 earnings date of Tuesday, May 16. Before that, Imperial has dividend pay dates at the end of December and March. More impactful to possible stock price volatility is a shareholder meeting on Wednesday, Feb. 1.

Corporate Event Calendar

Wall Street Horizon

The Technical Take

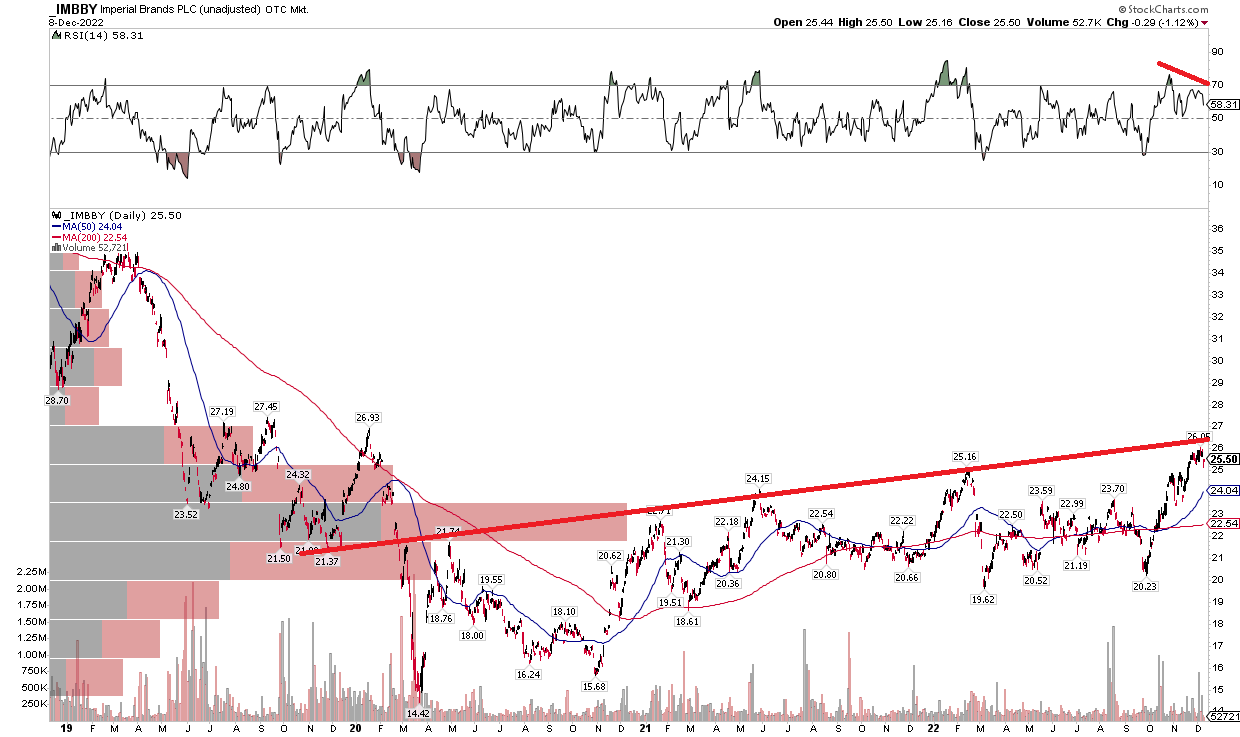

IMBBY sports a nice uptrend, but I see shares encountering resistance. Moreover, there’s bearish RSI divergence on the latest run-up. Profits should be taken considering the more than 20% jump off the October low. What’s positive from a longer-term perspective is a rising 200-day moving average, and I see support in the $19.60 to $21 zone – that should be a good spot to buy the stock on a pullback.

IMBBY: An Uptrend, But Share Hit Resistance

StockCharts.com

The Bottom Line

I like the valuation and dividend on Imperial, but the chart suggests taking a cautious stance in the short run. Buying in the low $20s looks like the right entry point, but long-term investors can hold the stock for its big yield.

Be the first to comment