Alex Wong/Getty Images News

Immersion Corporation (NASDAQ:IMMR) has had a mixed reputation in the investing world in regard to its business model, which primarily entails defense of its 1,200-plus patent portfolio, which it has successfully defended against big players like Sony (SONY) and Apple (AAPL), and is currently in litigation against Meta Platforms (META).

Taking into consideration its almost non-existent R&D, the company looks like it’s relying on its early mover advantage in the haptic industry, and its associated patents, as the means of generated revenue and earnings.

The problem with a business model like that is it doesn’t have much upside, as evidenced by revenue remaining in a range of $30 million to $36 million over the last five to six years.

And while its mobility segment has been growing nicely, its automotive and gaming segments have been dropping as a percentage of revenue, with revenue remaining in the range mentioned above.

In this article we’ll look at some of the latest numbers from its last quarter, look closer at its business model, and why there aren’t any visible catalysts that would drive its performance sustainably higher, outside a possible win in its lawsuit with Meta Platforms, which could give it a temporary boost, or possibly, depending on the outcome, another revenue stream that may modestly increase its top and bottom lines.

Recent earnings report

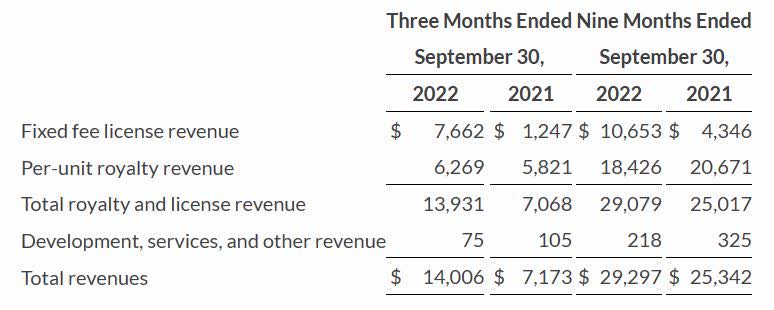

Revenue in the third quarter of 2022 was $14.0 million, compared to $7.2 million in the third quarter of 2021. Revenue in the first nine months of 2022 was $29 million, compared to revenue of $25.3 million in the first nine months of 2021.

The company continues to run lean, cutting GAAP operating expenses to $3.1 million in the reporting period, down from $3.5 million in operating expenses in the third quarter of 2021. Taking into consideration expenses from sales and marketing and R&D continue to fall, it reinforces my thesis that the company is almost totally relying upon its patent portfolio as its business model.

I say “almost” because it is attempting to leverage some of its cash from its licensing and royalty revenue streams into stock investments.

As for its fixed fee licensing revenue stream, that was $7.7 million in the third quarter of 2022, compared to $1.2 million in the third quarter of 2021. Its fixed fee licensing revenue for the first nine months of 2022 was $10.7 million, compared to $4.3 million in the first nine months of 2021.

Per-unit royalty revenue for the third quarter of 2022 was $6.3 million, compared to per-unit royalty revenue of $5.8 million in the third quarter of 2021. Per-unit royalty revenue for the first nine months of 2022 was $18.4 million, compared to per-unit royalty revenue of $20.7 million in the first nine months of 2021.

Net income in the third quarter was $7.7 million, or $0.28 per diluted share, compared to net income of $3.8 million, or $0.12 per diluted share in the third quarter of 2021. Net income in the first nine months of 2022 was $10.96 million, or $0.43 per share, compared to net income of $11.1 million, or $0.48 per share in the first nine months of 2021.

In the third quarter of 2022 the company had cash and cash equivalents and short-term investments of $133.5 million.

As of the end of the third quarter of 2022 the company had repurchased 2,542,065 shares at an average price of $5.20 per share and instituted a cash dividend of $0.03 per share.

Revenue percentage by segment

There has been a significant shift in revenue per segment since the third quarter of 2021. At that time its Mobility segment accounted for 61 percent of revenue, followed by Gaming with 23 percent, Automotive with 14 percent, and Other with 2 percent.

In the third quarter of 2022 that shifted to Mobility accounting for 75 percent of total revenue, Gaming 14 percent, Automotive 5 percent, and Other 6 percent.

For the first nine months of 2022 Mobility accounted for 67 percent of total revenue, Gaming 19 percent, Automotive 8 percent, and Other 6 percent.

Earnings Report Company Website

There are a couple of things of interest in these numbers, the first of which is I was surprised by the rapid decline in Gaming revenue as a percentage of total sales; I would have thought that would be a segment that would be a growth engine for the company.

I feel the same about Automotive. It’s not that the segments are declining, it’s the pace of decline in quite significant.

What it appears is happening is it could be a result of the running off of its patents, or a reduction in use of its patented technology in the two segments in order to save money, as top management reprioritizes spending in the uncertain macroeconomic environment.

Risk with its patent portfolio

There are strengths and weaknesses to relying upon a patent portfolio as a business model. The strength is an enforceable revenue stream that provides a moat for the duration of the patent.

On the other hand, a patent portfolio has the weakness of being temporary in duration. For example, from the end of 2021, the company held approximately 1,600 patents. By the end of June 2022, that had dropped to between 1,200 to 1,300.

The point there is, while there is a very predictable stream from fixed fees, licensing and royalties, those streams of revenue dry up once the patents run off. So in order to grow, the company must spend on R&D in order to develop new patented technology, or expand its existing patent portfolio to other markets.

Outside of that, it would be reliant on the emergence and growth of new industries like AR/VR for growth, based upon the need to use its technology.

It could be argued that its litigation strategy provides significant revenue at times, and that is true. The problem is, the bulk of that is usually in upfront settlements, and as past lawsuits have shown, when they are one, they don’t contribute huge amounts of recurring revenue to the top line of the company.

In other words, even with a win with Meta, it would primarily be a temporary boost on the front end, but as for a revenue stream it would probably be more modest than people many think, again, based upon past legal wins.

That said, the patents associated with the Meta Quest headsets have a patent life of 14 years remaining on them and based upon sales possibly reaching as high as $100 million over the next couple of years, and assuming the trial lasts that long, it would result in a big royalty payment from Meta to IMMR.

The other thing to consider is the company is running out of big companies to litigate against, and investors need to look at the inherent potential in its patent portfolio over the long term, and in that regard, it has limited upside based upon its lack of R&D, and the continued running off of its patent portfolio, which is going to continue to shrink.

Share price

Over the last couple of years, IMMR has stood up fairly well when considering the depth of the decline in high-growth tech stocks over that period of time. On February 8, 2021, it was trading at roughly at $16.50 per share, and dropped to a 52-week low of $4.22 on May 9, 2023, before jumping to a 52-week high of $8.195 on December 5, 2022.

If we look at its performance in 2022, it has actually made a nice run, especially from mid-October 2022 when it was trading at a little under $5.00 per share.

With nothing but the Meta litigation as a tailwind that could drive its share price up like that, it appears that is what the positive catalyst has been. That would suggest it’s being priced into the stock at this time, although I think it would get a much bigger upward move if IMMR wins the lawsuit, which based upon past wins, is very likely.

TradingView

Conclusion

IMMR is a company that has a business model of building up a patent portfolio in the haptic sector that is vigorously defends against anyone adapting the technology in its products. So far that has generally worked for the company, but it has limited upside because of the temporary nature of patents.

On the litigation side, it can get temporary boosts to its share price because of the millions of dollars it’s awarded, but as mentioned earlier, there aren’t a lot of big companies with deep enough pockets to move the needle if it decides to litigate to defend its patents.

That leaves licensing and royalty revenue streams as the growth engine of the company, and it would have to have a lot more deals in place to give it the momentum to break out of the revenue range its been in over the last five years. That’s because it’ll need to replace revenue streams as its patent portfolio continues to shrink over time. To do that, it would have to expand its reach in international markets.

Since the company has basically abandoned developing new products it could patent, based upon its miniscule R&D spend, it’s puzzling as to how it’s going to grow the company over the long term.

In the short term, it should be able to maintain its revenue streams in the $30 million to $36 million range it has been in for several years, and may even get a slight bump up if its wins its lawsuit against Meta, which it has a high probability of doing.

Taken together, I see IMMR as more of a trading stock than a long-term holding. It does have the capacity to move in big swings when it wins its lawsuits, and that will no doubt happen if it wins against Meta.

But with it jumping in price in 2022 with no growth catalysts, I think it’s going to drop back down until the lawsuit with Meta is decided.

Be the first to comment