Sundry Photography/iStock Editorial via Getty Images

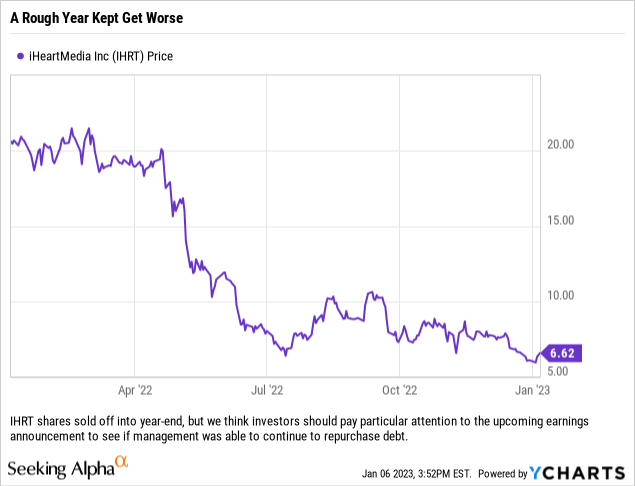

We last covered iHeartMedia (NASDAQ:IHRT) back on August 10, 2022 in an article where we discussed why we felt the company’s shares had already bottomed. At the time, shares were down 60% for the year and we thought that there was a nice entry point available for investors. As it would turn out, there was further downside and since our article the stock is down 30% from that point. By this information alone, one would think that investors should be bailing because iHeartMedia either has a busted business model or is a broken stock.

While the results on our latest entry have been pretty depressing, we think that the management team has the correct plan in place to deleverage the balance sheet and essentially do now what Cumulus Media (CMLS) did about two years ago.

Debt Load

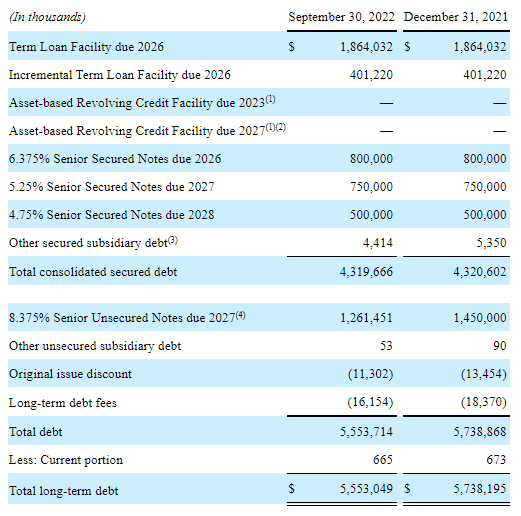

Looking at the company’s latest quarterly report, as of September 20, 2022 iHeartMedia had total long-term debt of just over $5.55 billion. Of that total, just under $4.32 billion is secured with the difference being unsecured debt. The company’s long-term debt is as follows:

iHeartMedia’s long-term debt load appears daunting. (Seeking Alpha, iHeartMedia Quarterly Filling)

All of this debt is high yield, but appears serviceable and at this time these issuances are not ones that investors should be losing sleep over. iHeartMedia has the wherewithal to manage this debt load and has no major maturities until 2026 – which provides additional room for management to maneuver.

Deleveraging

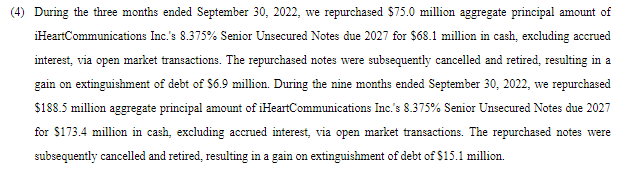

On the most recent quarterly results conference call, management discussed how they repurchased $75 million of the unsecured notes due in 2027 with a coupon of 8.375% in the third quarter. If you look at the company’s previously discussed quarterly filing, they disclose that this cost them $68.1 million (excluding accrued interest) which created a $6.9 million gain on the extinguishment of that debt.

A few positives about this specific transaction. First, using cash from the balance sheet, which is accumulating from FCF generation, can have (assuming the core business does not shrink) the added benefit of creating additional FCF. Also, based off of the numbers from the call and the filings, it appears that last quarter the company repurchased its bonds for just under 91 cents on the dollar. So, by deploying cash to retire debt, the company is able to spend less now (rather than waiting until maturity) and create savings on the interest expense line moving forward.

iHeartMedia has been focusing on the unsecured debt this year, buying back just under $190 million in principal. (Seeking Alpha, Company Quarterly Filing)

For the year, iHeartMedia has now repurchased almost $190 million of this specific issuance and could end up purchasing at least $250 million (principal) total for the year at below par prices.

Why Focus On The Unsecured Issuance?

We think that management is being strategic about how they retire debt. While the easy answer would be that they are focusing on taking out the highest coupon debt in order to create additional cash flow, which through three quarters has resulted in annualized interest expense savings of nearly $15.8 million, we think that management is optimizing the balance sheet just in case interest rates remain elevated.

What do we mean by that? Well, the unsecured debt is the riskiest tranche and thus carries the higher coupon. The secured debt has extra protections and thus lower coupons. This also gives rise to interesting changes in the underlying price of these issuances as interest rates change and people have worries about the overall debt market. For instance, even though the 8.375% coupon debt has a higher coupon which should insulate those bonds better against rising rates (versus the lower coupon bonds), the other issuances from the company all have credit enhancers which also insulate their prices. In short, the secured debt basically has an average rating of B+ while the unsecured debt has an average rating of CCC+.

Long story short, outside of the 2026 debt (which trades between 93 and 94 cents) and the 2028 debt which sports a low 4.75% coupon (and trades for about 84.25 cents), the company’s debt that matures in 2027 trades at about the same price even though one has a coupon 3.125% higher. So when you are not an investment grade issuer, the easiest way to lower your interest expense and make your debt more attractive is to issue secured rather than unsecured debt. Now that the company is deleveraging, ironically they are presented with a no-brainer of a decision, which is to repurchase the unsecured debt at basically the same price as the secured debt even though the coupon has a yield that is roughly 60% higher.

We think that iHeartMedia may be able to repurchase on average $200 million per year from 2023-2026 and possibly $100 million in 2027 prior to the maturity of the unsecured debt. If you go with our base case that the company repurchases another roughly $60 million in principal in Q4 to get to about $250 million for 2022, then iHeartMedia ends the year at about $1.2 billion in outstanding debt for the 8.375% Unsecured Notes maturing on 5/1/2027.

With our assumption that the company could hit $900 million in repurchases (principal) for the unsecured debt prior to maturity, the company would only have to address rolling about $300 million of the unsecured. Even if rates are higher at that time, the company will have created an additional $75 million+ in annual interest expense savings and should be able to handle a higher rate on an overall smaller debt load.

Now one could argue that the entire 5/1/2026 secured issuance with a coupon of 6.375% could be repurchased by maturity, however we think there are two reasons that the company is not focusing on this earlier maturity. First, the interest rate is 200 basis points lower so there is less free cash flow created by repurchasing that debt. Second, if rates are still higher by then, rolling secured debt will be cheaper than trying to roll unsecured or a mix of secured and unsecured.

To highlight this point, we would point out that the 6.375% coupon 2026 secured debt is trading at a yield of roughly 8.66% while the 8.375% coupon 2027 unsecured debt is trading at a yield of roughly 12.20%. There is an obvious answer to this debt problem and management is in fact addressing this in the most economic and prudent manner possible in our view.

Looking Forward

There are a number of scenarios one can run off of these numbers, to figure out the impact to EPS, cash flow per share, etc. but they all hinge on the base case we laid out on iHeartMedia’s management being able to continue to aggressively repurchase debt. We feel pretty comfortable with our conservative estimates for at least $250 million in total repurchases this year and an average of $200 million per year moving forward. Already the company has repurchased $188.5 million through three quarters, and Q4 should see significant free cash flow (it is traditionally the company’s biggest quarter), so there is the possibility that we get more than $250 million this year.

In the years ahead, $200 million should be achievable if the company’s business remains relatively steady plus we would point out that the company’s debt over the last quarter has gotten cheaper; the repurchases in Q3 were done at about 91 cents on the dollar and that issuance is now trading just north of 87 cents on the dollar. While that does not sound like a big difference, when you are discussing millions of dollars, especially hundreds of millions of dollars, it really does matter because on $200 million in purchases on a forward basis (principal), that would result in $8 million less in actual spend (and cost $174 million total rather than $200 million).

Our Final Thoughts

We really like these highly leveraged media businesses that have management teams focused on optimizing the business while also addressing debt loads right now. Not all of them are of the same quality, but we are finding some names with management teams that are making smart moves and creating scenarios where they may very well surprise the market in the next 12-24 months by having leverage ratios much healthier than anyone expected and additional cash flow to deploy via savings on interest expense.

Of course, this will hinge upon the economy not turning south and advertising dollars disappearing, but we would point out that there should be a wave of political advertising starting gradually in late 2023 and flooding the market in 2024. That bodes well for this trade, as it is a kicker that can either help solidify our thesis or drastically enhance our base case.

Be the first to comment