Wolterk

One company that has exceeded my expectations as of late is a firm called El Pollo Loco (NASDAQ:LOCO). Even though profits and cash flows for the company have shown signs of weakening, the increase in sales achieved by the business, combined with reasonably priced shares, has led to some nice upside relative to what the broader market has experienced. Although I still maintain the view that the company’s fundamental condition likely warrants a lower valuation than its peers, my opinion on the company has improved as of late. Although I don’t feel as though the company will offer significant upside potential from here on out, I do now think that it probably warrants a soft ‘buy’ rating compared to the ‘hold’ rating I assigned it to previously.

Crazy performance

The last time I wrote an article about El Pollo Loco was back in May of 2022. In that article, I acknowledged that shares of the company looked quite cheap on both an absolute basis and relative to similar restaurant chains. At the time, revenue and earnings were continuing to grow, but the company’s cash flow picture had not shown any substantial improvement over time. This absence of growth led me to be somewhat neutral on the company, leading to my decision to rate it a ‘hold’ to reflect my opinion that shares would likely generate upside that would more or less match what the broader market would achieve moving forward. Since then, however, the company has outperformed my expectations. While the S&P 500 is down 3.7%, its shares have generated upside of 12.3%.

Author – SEC EDGAR Data

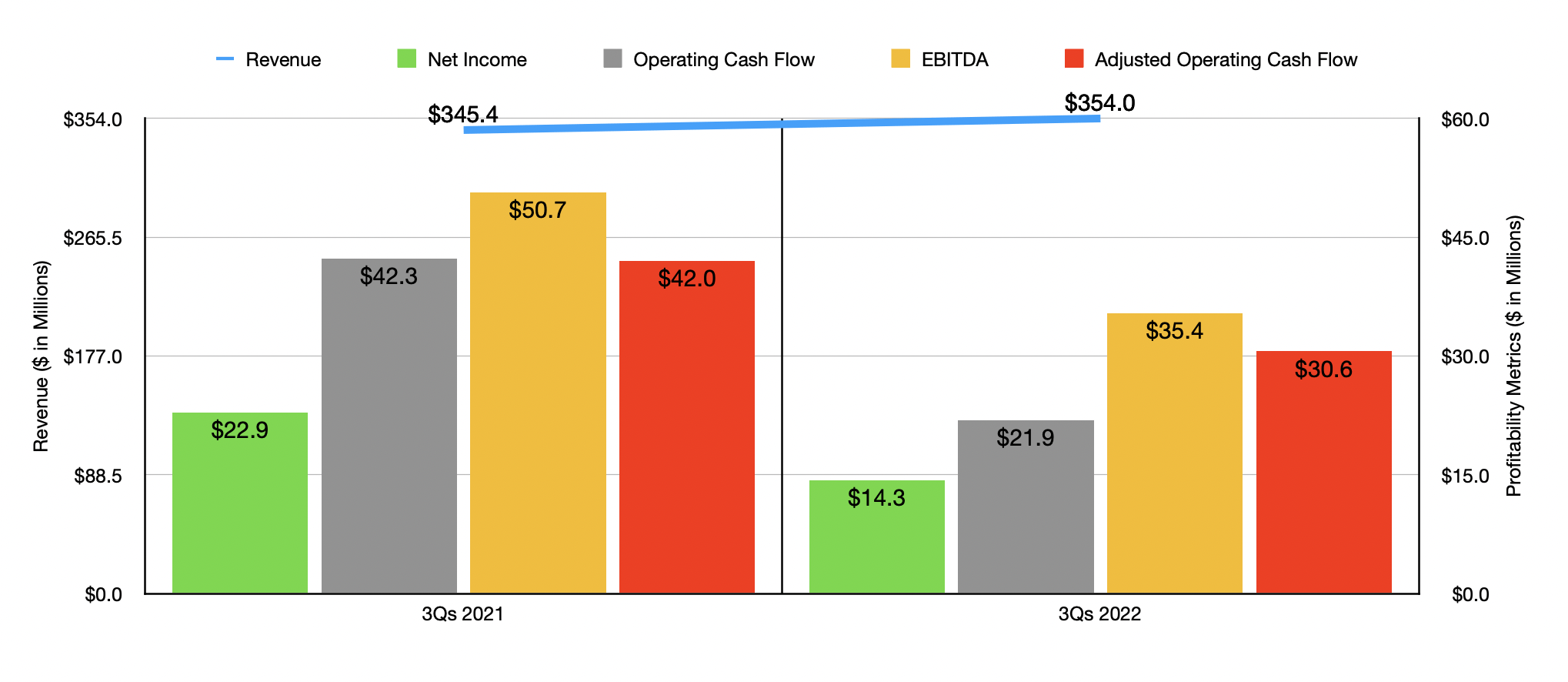

For investors, the key driver here seems to be growth on the top line. And even though the company is exhibiting some weakness in some respects, that sales growth does continue. For the first nine months of its 2022 fiscal year, for instance, the company generated revenue of $354 million. That’s 2.5% higher than the $345.4 million generated the same time last year. This increase was driven mostly by higher revenue associated with its franchised locations. With the number of franchised stores climbing from 290 to 297, revenue generated from franchise revenue for the company grew from $24.9 million to $28.9 million, while franchise advertising fee revenue grew from $19.4 million to $21.6 million. By comparison, revenue associated with the company’s 190 locations that are owned by the business rose more modestly from $301.1 million to $303.6 million.

Even though sales increased nicely, profits for the business are down. Net income during the first nine months of 2022 totaled $14.3 million. That compares to the $22.9 million generated the same time one year earlier. On the cost side of things, the company saw its food and paper costs climb from 22.9% of sales to 25.3%, while labor and related expenses increased from 26.1% of sales to nearly 28%. This increase in costs also was instrumental in pushing cash flow figures for the company down. Operating cash flow nearly halved from $42.3 million to $21.9 million. Even if we adjust for changes in working capital, it would have dropped from $42 million to $30.6 million. Meanwhile, EBITDA for the business tanked from $50.7 million to $35.4 million.

Author – SEC EDGAR Data

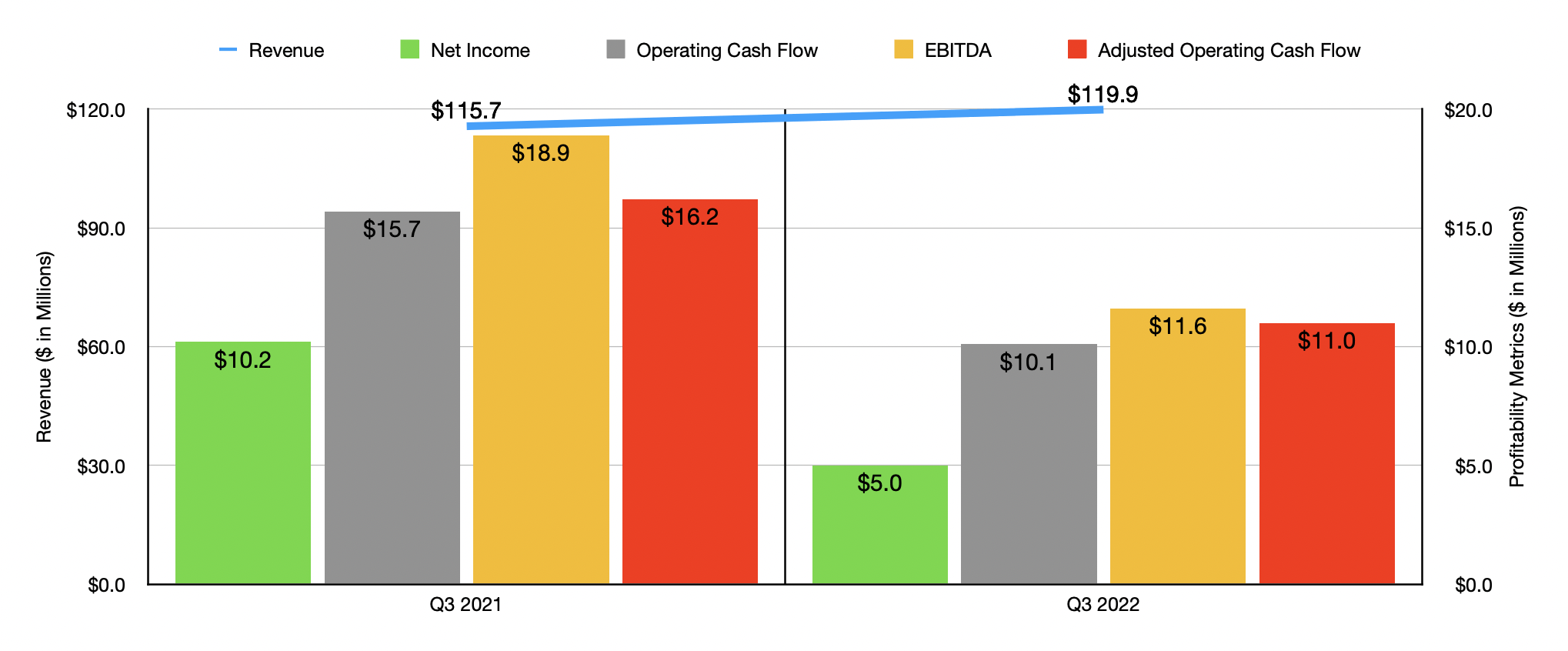

This trend continued into the third quarter of the year on its own. Revenue of $119.9 million came in 3.6% higher than the $115.7 million reported the same time one year earlier. At the same time, profits plunged from $10.2 million to $5 million. Operating cash flow declined from $15.7 million to $10.1 million, while the adjusted figure for this dropped from $16.2 million to $11 million. Even EBITDA pulled back, dropping from $18.9 million to $11.6 million. One thing that does not help confidence, in my opinion, is that management, during this time, has expressed interest in buying back stock. On October 11th of 2022, the company announced a $20 million share buyback program. Though to date, it’s unclear how much, if any, they have repurchased. Instead, the company should be focused on continued growth. For 2022 as a whole, they were forecasting the opening of only two new company-owned restaurants and between seven and nine franchised restaurants. Cost-cutting initiatives aimed at generating more cash flows, in the long run, would also not be a bad idea.

Author – SEC EDGAR Data

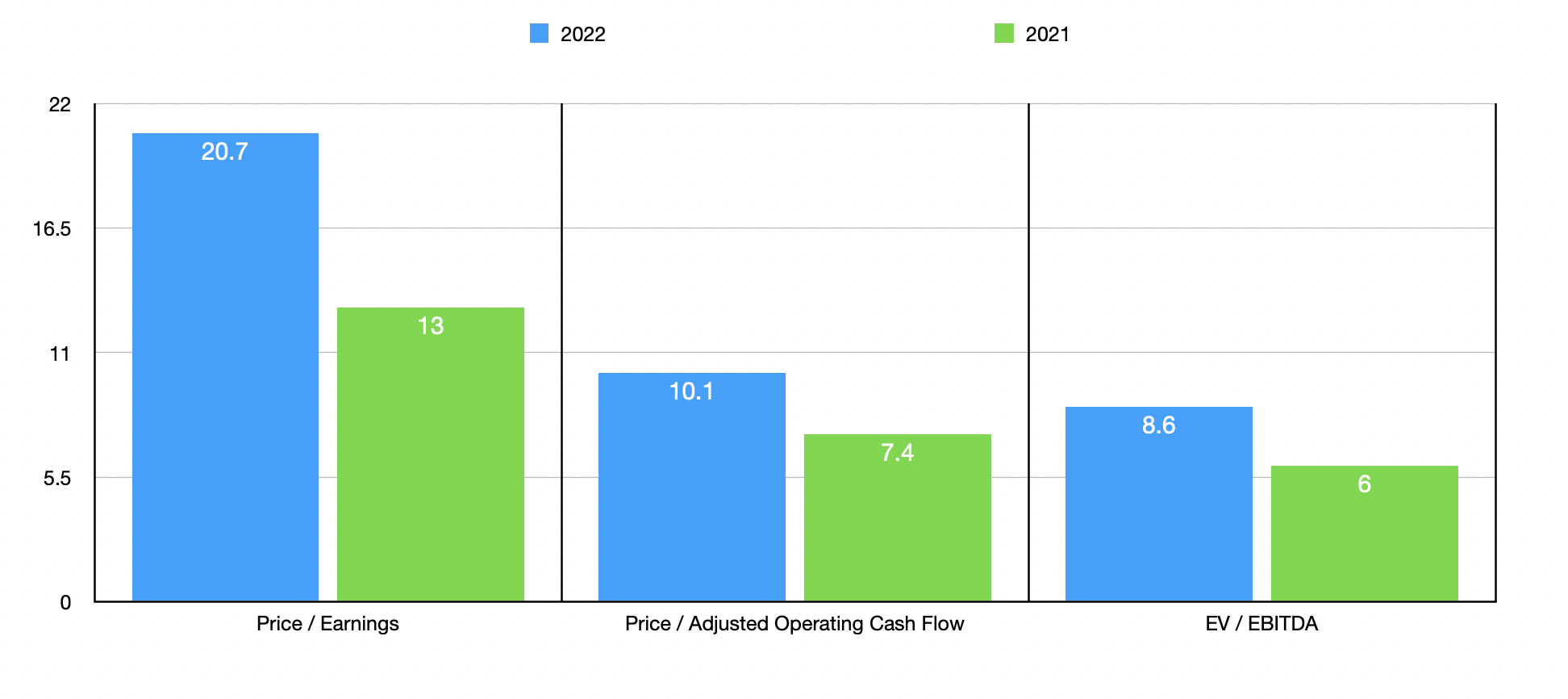

Because management has not provided any detailed guidance, we don’t really know what to expect for the rest of 2022. If we simply annualize results experienced so far, we would anticipate net income of $18.2 million, adjusted operating cash flow of $37.4 million, and EBITDA of roughly $44.3 million. If these numbers come to fruition, the company would be trading at a price-to-earnings multiple, on a forward basis, of 20.7. The forward price to adjusted operating cash flow multiple would be considerably lower at 10.1, while the EV to EBITDA multiple would come in at 8.6. By comparison, in the chart above, you can see pricing if we use data from 2021. At some point, margins should improve for the company. If they go back to what they were in 2021, the company would look quite cheap. As part of my analysis, I also compared the business to five other restaurant chains of a similar size. On a price-to-earnings basis, the four companies with positive results had multiples of between 15 and 745.7. And when it comes to the price to operating cash flow approach, the multiples for the five companies were between 8.7 and 19.8. In both cases, only one of the five companies was cheaper than El Pollo Loco. Meanwhile, using the EV to EBITDA approach, the range was between 6.4 and 85.2. In this case, only two of the five companies were cheaper than our prospect.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| El Pollo Loco Holdings | 20.7 | 10.1 | 8.6 |

| Chuy’s Holdings (CHUY) | 22.3 | 11.9 | 8.3 |

| Kura Sushi USA (KRUS) | N/A | 19.8 | 85.2 |

| The ONE Group Hospitality (STKS) | 15.0 | 8.7 | 6.4 |

| Noodles & Co (NDLS) | 76.1 | 18.0 | 18.1 |

| BJ’s Restaurants (BJRI) | 745.7 | 13.7 | 11.8 |

Takeaway

Although you might expect me to get more bearish about the company after seeing shares increase and bottom line results worsen, I understand now that investors are looking favorably upon the increased sales of the company. I also believe that inflationary pressures are likely to ease in the next year, increasing the probability that margins will go back to something similar to what they were in prior years. Add on top of this how cheap shares are on both an absolute basis and relative to similar companies, and I think that a soft ‘buy’ freighting would not be inappropriate at this time.

Be the first to comment