Maria Vonotna

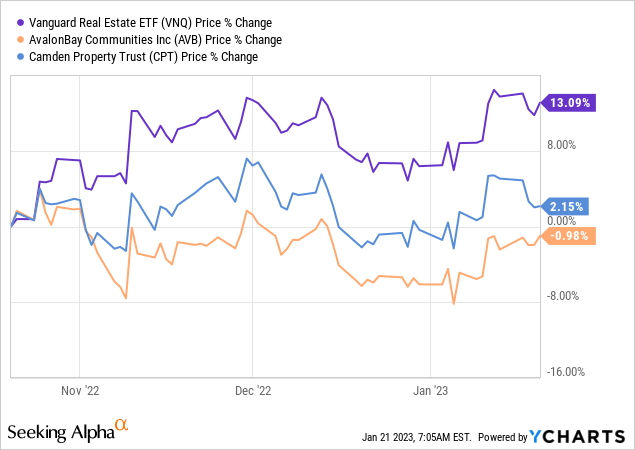

Most REITs recovered nicely over the past 3 months, but blue chip apartment REITs AvalonBay Communities (AVB) and Camden Property Trust (CPT) missed on this recovery:

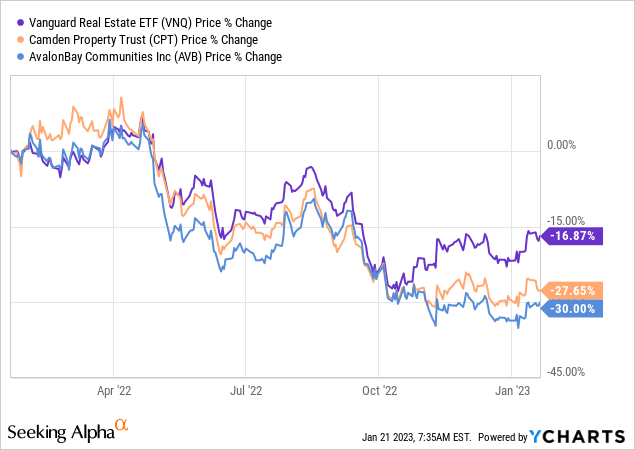

As a result, these blue-chip apartment REITs are now down a lot more than the average of the REIT sector over the past year:

We think that this is a historic buying opportunity.

AVB and CPT are both considered to be blue chips because they own class-A apartment communities, have strong investment grade-rated balance sheets, and have long track records of significant outperformance.

You could objectively say that these are resilient high-quality companies and yet, they are down even more than the average of the REIT sector.

AvalonBay

The market appears to be especially pessimistic about these apartment REITs because they are guiding fewer development projects in the near term. Moreover, rent growth will likely decelerate and there are concerns about cap rate expansion, which could negatively affect property values.

These are fair concerns, but do they really justify a ~30% discount to net asset value?

We don’t think so.

We think that the market is simply overreacting to near-term issues as it always does.

REITs like AVB will start fewer development projects in the near term because we are going through uncertain times. The high inflation and rising interest rates make it more complicated and riskier to develop new properties, and in an abundance of caution, AvalonBay prefers to delay some of its future projects. This will slow down its growth in the near term, but it does not change the long-term thesis, and it is the right thing to do in the world we live in.

Secondly, rent growth will likely decelerate as new supply hits the market and we go into a recession, but we all knew this already. The market appears to have only recently reacted to this reality as increasingly many media headlines began pointing it out. It is important however to remember that rent growth remains solid even despite a deceleration. Double-digit rent hikes are turning into high-single-digit rent hikes and those may soon turn into mid-single-digit rent hikes, but that’s solid growth nonetheless.

Finally, as we have noted in a recent article, we don’t expect any significant cap rate expansion. Cap rates have expanded a bit, but NOI has risen a lot as well, leaving valuations more or less intact. This was recently confirmed by BSR REIT (OTCPK:BSRTF), which reported that its NAV per share was flat over the last quarter. (For context: BSR is a Canadian apartment REIT that only owns properties in the US. Unlike US REITs, it must disclose the fair market value of its properties according to IFRS accounting rules).

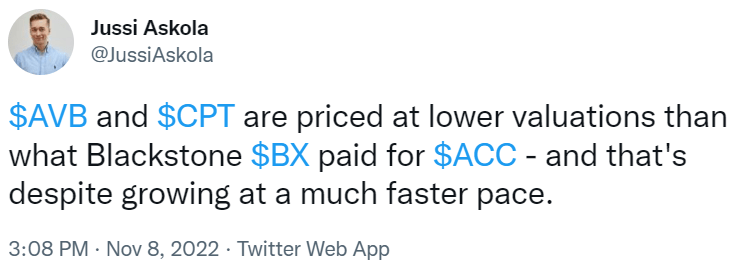

Major private equity firms like Blackstone (BX) have also been buying apartment communities left and right, despite the fears of rising cap rates. They recently bought out public REITs Bluerock Residential Growth REIT and American Campus Communities and these deals were made at materially higher valuations than those AVB and CPT today. This is one of the most sophisticated real estate investment groups in the world so don’t tell me that they don’t know what they are doing.

We think that the market has simply overreacted and mispriced these apartments REITs due to fears that won’t have a significant and lasting impact on their fundamentals. A 1-2 year period of slower growth has little impact on the fair value of apartment communities, which should be determined based on decades of excepted future cash flow.

Today, there is still lots of demand for these assets from institutional investors like pension funds and life insurers that need this type of long-dated inflation-protected cash flows.

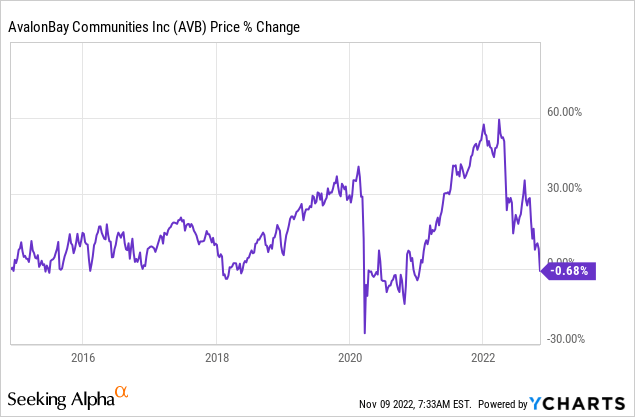

So repricing these assets at a 30% discount purely based on what we described earlier makes little sense. To really bring my point across, consider that AVB’s share price is now back at the same level it was in 2014 when its assets were far less valuable:

YCHARTS

We are today buying more shares of AvalonBay and Camden Property Trust. Both are similar, but CPT has a greater focus on rapidly growing sunbelt markets whereas AVB is more heavily invested in supply-constrained coastal markets. We believe that both offer 50% potential upside from multiple expansion, and we expect double-digit total returns from their 3-4% dividend yield and 5-7% annual growth while we wait.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment