gremlin/iStock via Getty Images

Now that Federal Reserve Chair Jerome Powell has warned of a potentially higher terminal Fed funds rate and that the bond market has adequately adjusted for this risk, we believe that the conditions necessary for signaling peak yields have been fulfilled. Recent data indicating a resilient economy also supports our view of a mild recession without a significant rise in corporate defaults. As such, we see high-yield bonds providing the best reward-to-risk within the fixed-income space for a medium-to-long-term investment horizon.

We initiate our coverage of the iShares iBoxx $ High Yield Corporate Bond ETF (NYSEARCA:HYG) with a “Strong Buy” rating.

High-Yield Bonds Setting Up For Historic Gains

For investors targeting a balanced portfolio allocation, we see a compelling case to overweight high-yield bonds. Having suffered a disastrous year marked by heavy bond market losses due to aggressive monetary tightening by the Fed, high-yield bonds are setting up for historic gains that could potentially surpass equity returns in the next one to two years.

Not only do we see yield compression as default risk moderates on the back of a resilient U.S. economy, but we also expect the much-awaited Fed pivot to materialize in late 2023 that will drive a broad-based decline in yields.

As the accompanying chart shows, the Bloomberg U.S. Aggregate Bond Index, which tracks the performance of a broad basket of U.S. investment-grade government and corporate bonds has collapsed by -16% year-to-date. On previous occasions when the index has registered intra-year declines greater than -5%, returns in the subsequent two to three years have often been quite spectacular. We certainly see the potential for double-digit returns for investment-grade bonds and even higher returns in the high-yield space.

Bloomberg, FactSet, J.P. Morgan Guide to the Markets – 31 October

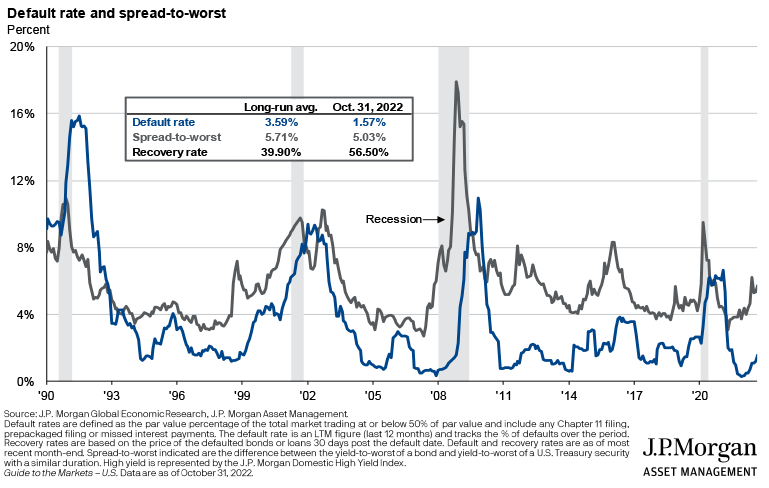

Resilient Economy Keeping Default Rates In Check

According to the latest commentary from Fitch Ratings, the agency is expecting U.S. high-yield default rates to reach around 2.5%-3.5% in 2023. This forecast remains below both the 3.8% 21-year historic average and well below the 5.2% rate set in 2020. The year-to-date high-yield default rate currently stands at just 1.2% and is expected to drift towards 1.5%-1.75% by the end of 2022.

These forecasts are generally in line with our view of a mild recession without a significant rise in corporate defaults. Despite this rather benign view of the economy, however, yield spreads have remained relatively wide (5%) due to heightened concerns of a deep recession.

J.P. Morgan

As the economic outlook improves in 2023 and fears over inflation subside, we expect spreads to narrow accordingly, giving an added boost to returns on high-yield bonds in addition to a broad-based decline in yields.

iShares iBoxx $ High Yield Corporate Bond ETF

According to fund information provided by iShares, HYG seeks to track the investment results of an index composed of U.S. dollar-denominated, high-yield corporate bonds. At the time of writing, HYG is the largest and most liquid high-yield corporate bond ETF with US$15.4 billion in assets under management, well ahead of the SPDR Bloomberg Barclays High Yield Bond ETF (JNK) in second place with US$8.5 billion.

As of October 3, HYG’s portfolio had an SEC yield of 8.22% with an effective duration of 4.14 years, and a moderate expense ratio of 0.48%. This is an ideal duration for our purposes, given that we see peak returns for high yields in the next one to two years.

Although we acknowledge that short-dated bonds look attractive at the moment, we see more return potential in longer-dated bonds when the Fed eventually pivots on monetary policy. Not only are longer-dated bonds likely to outperform due to higher sensitivity to interest rate changes, but they also provide long-term investors with the option to hold to maturity, avoiding the risk of having to reinvest at lower yields for the next couple of years.

iShares

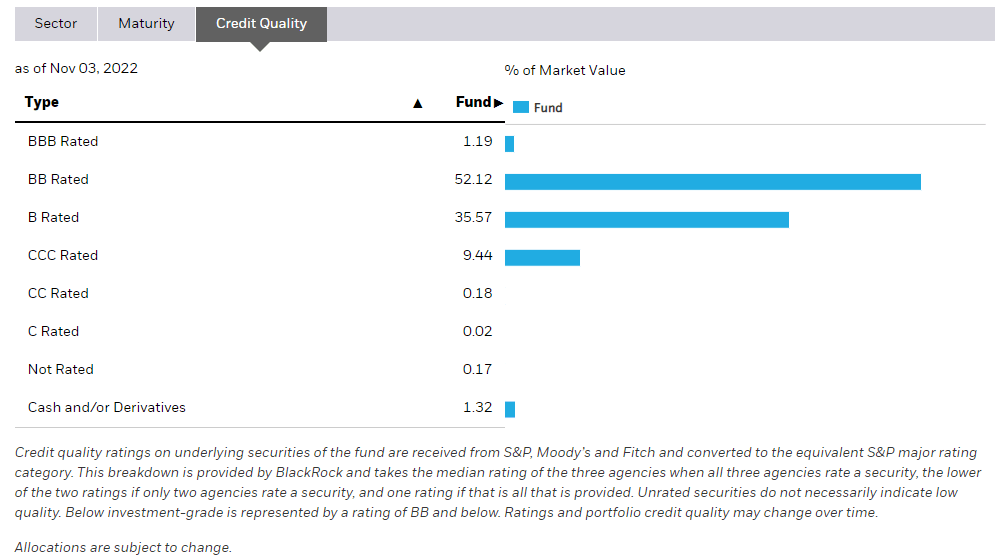

HYG is also well diversified, with 1,218 holdings and no single exposure exceeding 0.5% of the portfolio. The majority (52.1%) of the fund’s holdings are “BB” rated corporate issues in sectors including consumer cyclical (20%), consumer non-cyclical (13%), communications (18%), and energy (12%).

iShares

Trading metrics for HYG are also healthy with tiny spreads, high volumes, and the fund trading very close to NAV. We note that HYG usually trades at a premium above NAV, but at the time of writing is trading at a slight discount.

etf.com

In Conclusion

High-yield bonds are setting up for historic gains that could potentially surpass equity returns in the next one to two years. HYG is also a cost-effective ETF that will allow investors to quickly build exposure to high-yield bonds and lock in an attractive yield of 8.2% for the next couple of years.

We initiate coverage of HYG with a “Strong Buy” rating.

Be the first to comment