metamorworks/iStock via Getty Images

We really like buying regional bank stocks in this environment. We think they are best suited to benefit from the interest rate hikes the Federal Reserve is pushing as their balance sheets are bet easier to understand relative to a complicated multinational investment type bank. Simply put, they stand to benefit from widening net interest margins more than big global banks.

While we would expect regionals to see some slowing demand in loans for homes, autos, and new businesses, Huntington Bancshares Incorporated (NASDAQ:HBAN) continues to see growth. This was a name we last recommended as a buy at $8. Shares have appreciated about 75% from that buy call, but it has been a somewhat choppy grind and the stock has seen pressure like the market has in recent months. But the thing is that the low rates that weighed on financials was somewhat offset by a lot more demand. The pressure on bond yields from two years ago has completely reversed and yields are at highs not seen since the financial crisis.

Loan loss provisions are a recurring concern, given the economic woes stemming from high inflation and the battle against it. However, HBAN has just reported earnings, and in this column, we check back in with this sizable regional bank. We rate shares a buy. The price is still relatively attractive on valuation and the stock is a nice dividend-paying stock yielding over 4.5%. While the next few quarters will be tough on markets as rates keep rising and the economy weakens, we have been urging buys in the space. Let us discuss the key metrics you should be looking for in any bank investment.

Revenue strength in Q3 2022

Thanks to continued loan growth, deposit strength, and strong net interest income the bank saw revenues continue to reach new highs. In Q3, Huntington Bancshares reported a top line that beat consensus estimates slightly, and rose from Q3 2021.

With the present quarter’s revenues of $1.9 billion, the company saw an 11.8% increase in this metric year-over-year. The $60 million beat was not overwhelming, but given the difficulty of handicapping where results would land and the anxious state of the markets we see this as a big win for the bank. Many banks have been preparing for an economic downturn for months sometimes costing them on the top and bottom lines relative to peers, but this was a strong quarter and the outlook remains strong. However, pressure in non-interest income and a spike in provision for credit losses weighed on earnings, though they also beat expectations.

Earnings beat, but watch loss allowances

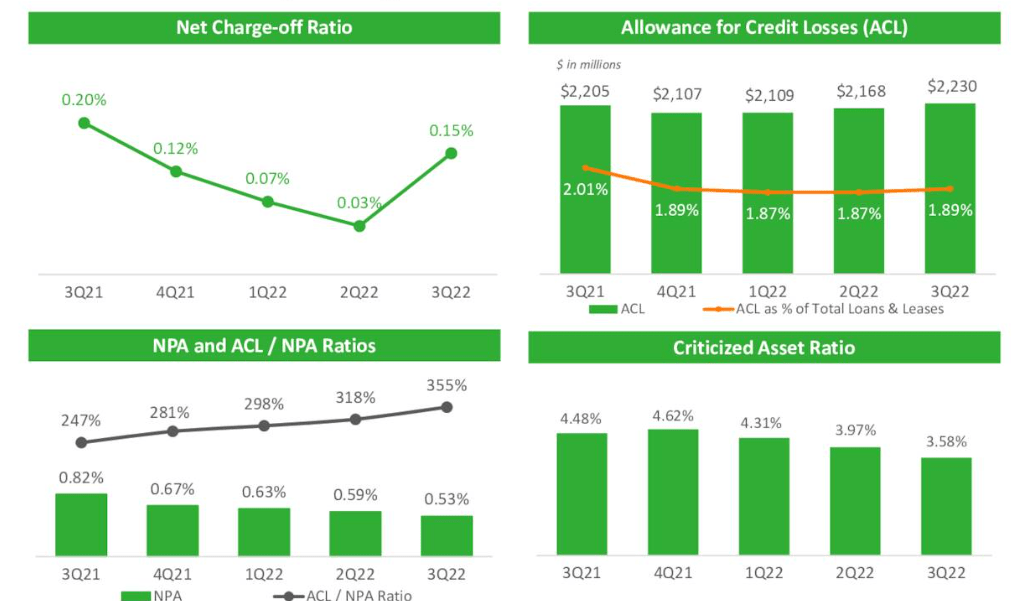

The jump in revenues year-over-year led to strong earnings, though we are closely watching expenditures as well as an increase in the allowance for credit losses which was up two basis points to 1.89% of total loans, reflecting a reserve given heightened economic uncertainty, a total of $2.2 billion. Overall, Huntington reported net income of $594 million, a nice increase from a year ago, which saw net income of $377 million.

HBAN Q3 slides

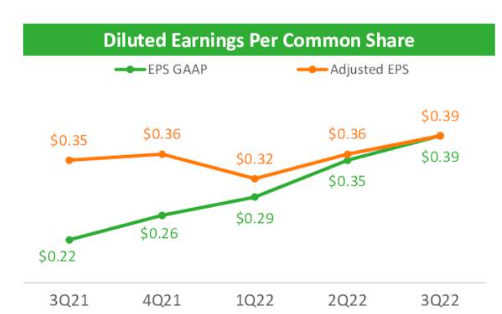

Earnings per share came in at $0.39, up from Q3 2021 $0.17. What investors need to decide is if there will be improvement or not, and we think there will be as net interest income looks like it will only get better in 2023. It is a great time to own regional banks, but do watch closely to see if there is a decline in loans or deposits, as well is changes in credit quality. For now, we see strength on the horizon.

Loans and deposits show growth

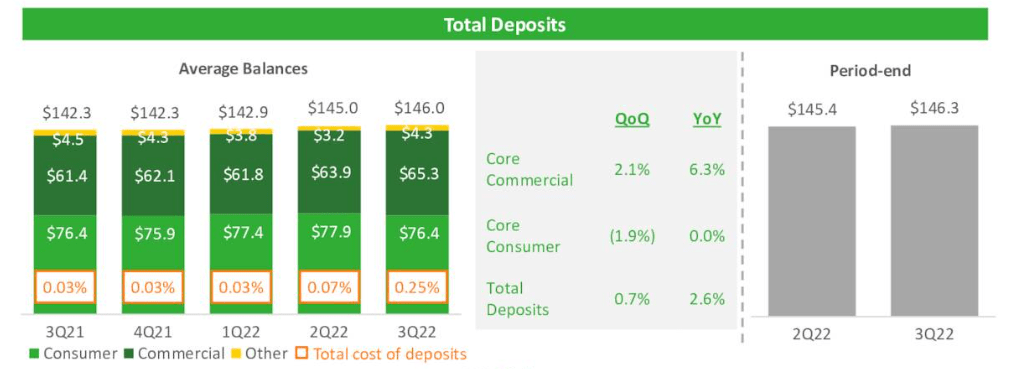

While the company has made strategic acquisitions in the past we want to see organic growth in loans and deposits. We are pleased with the progress. The bank delivered average deposit growth of $1 billion. Deposit growth was led by commercial deposits, up $1.4 billion. Total deposits were $146 billion, up $4.7 billion from last year.

HBAN Q3 slides

Remember, we always say that growth in loans and deposits is key for any bank, small or large. That is how you make money as a bank. It is the bread and butter of any bank. It just works, especially when demand remains solid and loans are made at better rates. The model is simple, you take in deposits at a low interest rate, and lend at a higher one. It has been working for hundreds of years, and will continue to do so well into the future.

HBAN Q3 slides

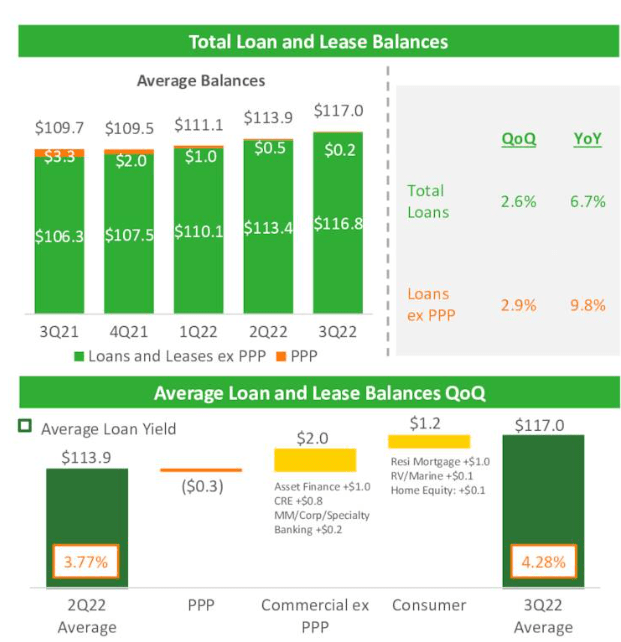

That said, the bank saw Q3 average loan balances jump 2.6% quarter-over-quarter, coming in at $117 billion. Excluding PPP, total loan balances increased $3.3 billion, or 2.9% driven by both strong demand for commercial and consumer loans. These results for Huntington should be considered a strength.

Asset quality

We alluded to this above when we noted the increase in allowance for loan losses. Most banks are reading the tea leaves and upping their provision for losses. You see, loan growth is a strength, but only if the loans are quality. Risky loans may offer a higher return but not if the debt cannot be repaid and turns to toxic debts. Right now, the risk is purely economic as recession (which technically is here if you look to GDP) is widely expected to hit home in 2023.

HBAN Q3 slides

Now, over the years, the one reason we like Huntington is that it has been a relatively conservative lender, and its asset quality has continued to improve over time. As we mentioned the allowance for credit losses increased to $2.2 billion, or 1.89% of total loans and leases. Many of the major banks we have covered have seen banks going on defense more often than not. This is the risk of being a big regional bank. They are clearly preparing for possible defaults. Net charge-offs have ticked up. Net charge-offs were 0.15% of average total loans and leases for the quarter, but just 0.08% year-to-date. That said, nonperforming assets saw their 5th quarter of declines.

HBAN Q3 slides

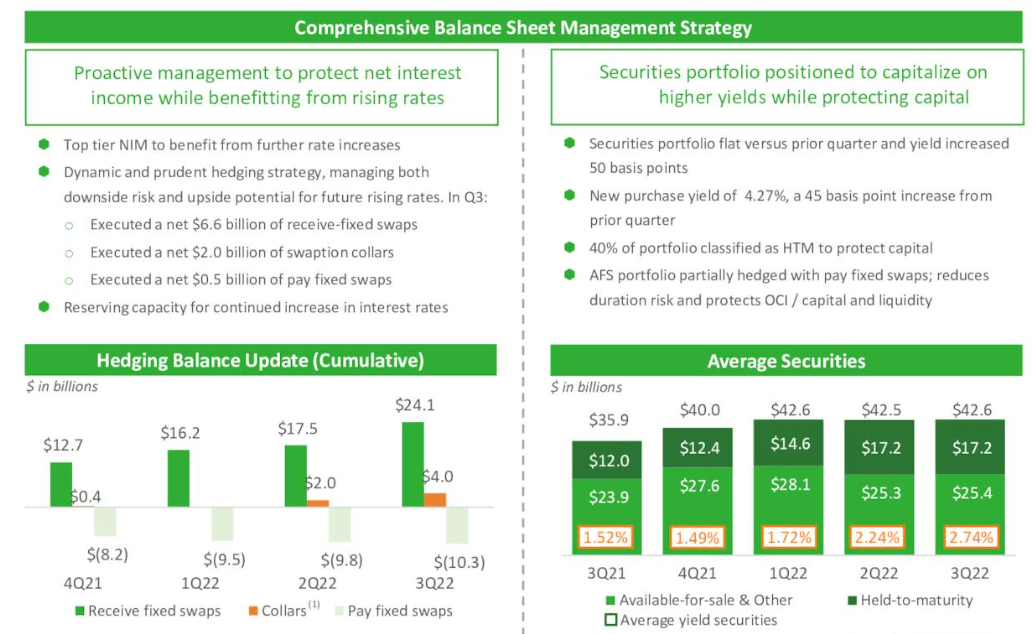

When you combine all of this information with the fact that management has been managing the balance sheet against the volatile rate backdrop through hedges and swaps, we think they have mitigated risk. The investment here is steady, and while all investment carries risk, as far as a regional bank is concerned, this one is strong.

Despite some protective actions, the improvement in the efficiency ratio continues to impress us as well.

Superb efficiency ratio

We always look for improvement in the efficiency ratio. The strongest banks have an efficiency ratio under 60%, with the ideal being around 50%, which is rather textbook. Well, this is also a strength of the bank. The efficiency ratio hit 53.9% a 210 basis point improvement from just Q2. We are pleased with what we see and anticipate this metric will remain under 60% in 2023. This is because the ratio is tied to revenue drivers and expense management activities which have been stellar here.

Take home

This is a winning investment. Huntington Bancshares Incorporated still pays a solid dividend, with a yield north of 4.5% now. The economy will likely soften, and the bank is preparing for some impacts there, but at the same time sees its net interest margins and income improving. The Huntington Bancshares is very healthy and enjoys robust demand at a reasonable valuation. Stock is buy.

Be the first to comment