Althom

Introduction

There are thousands of ways to assess the quality of one’s portfolio. Most of them are quantitative measures based on numbers and math. However, I also apply a simple measure based on coming up with reasons to sell investments in my portfolio. If I cannot come up with compelling reasons, I’m not selling a single share. Huntington Bancshares (NASDAQ:HBAN) has been in my portfolio since 2020. I got in really cheap as part of a bigger project I was working on back then. The shares add quality high-yield to my portfolio. Yet, I am constantly looking to sell as I prefer stocks with higher growth and I have to say that regional banking stocks are so very boring. However, I haven’t sold a single share under the HBAN ticker as the company is simply too good to sell. There are not a lot of good alternatives in that high-yield range (without going overweight energy) and if HBAN dividend growth picks up again, we’re dealing with a company that is poised to deliver very satisfying long-term total returns.

In this article, I will guide you through my thoughts and explain why HBAN shares will remain a core part of my portfolio.

Also, I finally get to give my income-oriented investors a high-yield pick again after covering a lot of dividend growth stocks this year.

So, let’s get to it!

Quality High-Yield

Initially, Huntington Bancshares was my only financial holding. I bought the company in 2020 at $9.30. Back then, I was working with clients on trading opportunities given the severe stock market weakness back then. I decided to go a step further and make the company a core holding of my dividend portfolio back then. I really liked the high yield, which was needed given that I decided to mainly focus on dividend growth.

Author Portfolio

My current pre-tax portfolio dividend yield is 2.3%, which I am hoping to maintain.

This means I will have to stick to high-yield companies as I continue to buy low-yield dividend growth stocks.

Huntington Bancshares is a great way to add income to one’s portfolio. This Columbus, Ohio-based regional bank was founded in 1866. With a market cap of $19.0 billion, the company is the 9th-largest regional bank in the United States

The bank’s main focus is on the Midwest, where it has a huge footprint in Ohio, Michigan, Minnesota, Pennsylvania, and India with branches in Illinois, Colorado, West Virginia, Wisconsin, and Kentucky.

The single best thing about HBAN is its yield, which is backed by strong fundamentals.

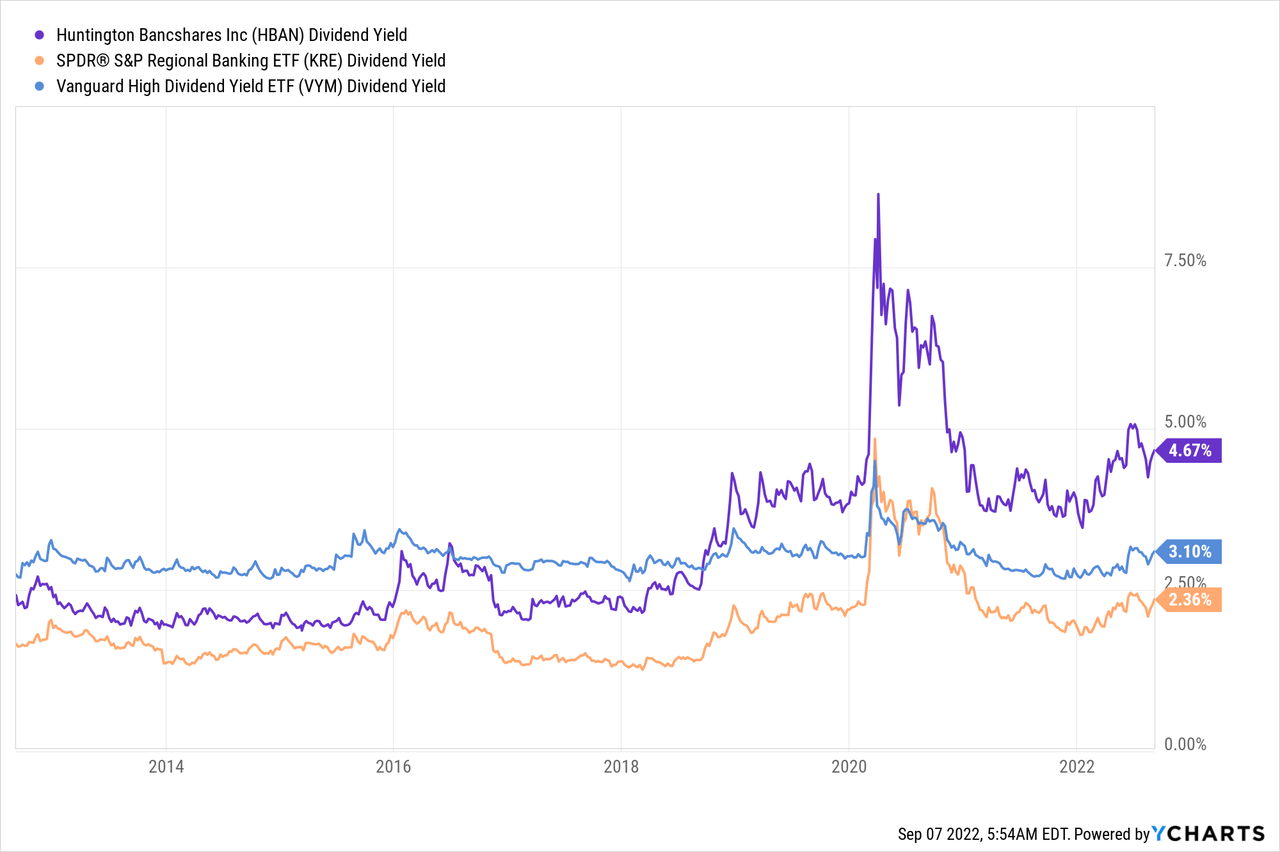

Currently, HBAN pays its investors $0.155 per share per quarter. That’s $0.62 per year, which translates to a 4.7% yield. This yield is one of the highest of the past 10 years, excluding the pandemic sell-off in early 2020. Moreover, this yield is almost 160 basis points above the Vanguard High Yield Dividend ETF (VYM), and more than double the yield of the SPDR Regional Banking ETF (KRE).

If investors want a yield this high, there are opportunities in other areas. For example, a lot of energy companies have similar yields or at least the potential to get to HBAN’s levels thanks to high energy prices.

HBAN, however, brings a bit more to the table than just a decent yield.

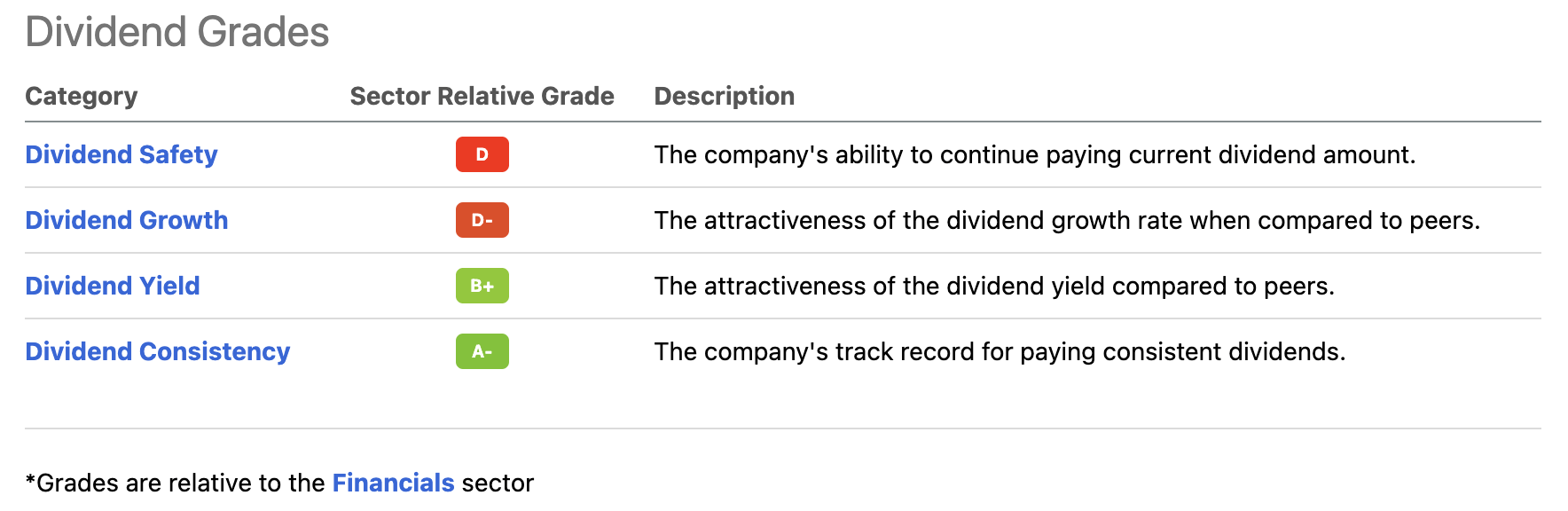

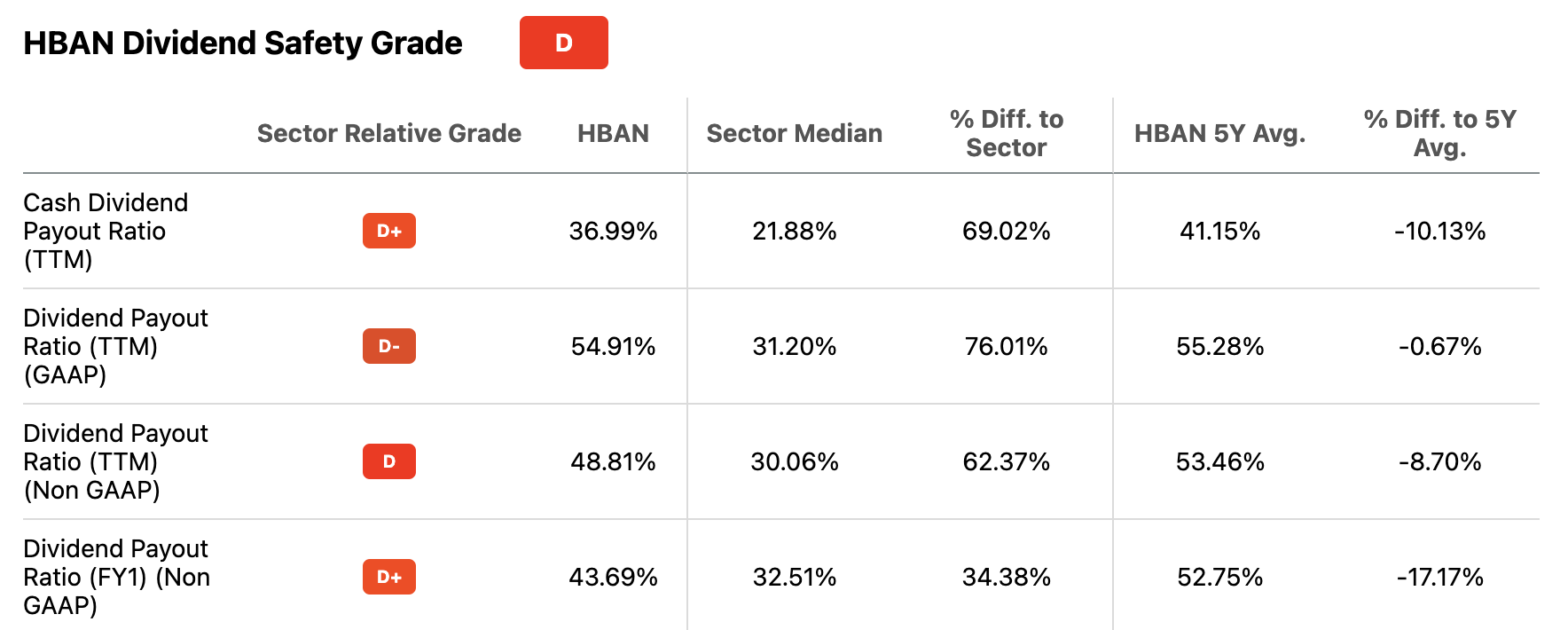

The table below displays the Seeking Alpha dividend scorecard for HBAN. Please note that all numbers are quantitative, meaning no subjective opinions are involved here. Also, the grades are relative to the financial sector.

Seeking Alpha

What we see is that the yield is indeed scoring high versus financial peers, and that’s a good sign as financials, in general, tend to have high yields – think of major banks, regional banks, and related companies.

Moreover, the company scores low on dividend growth. That’s not entirely true as it depends a bit on what numbers are important.

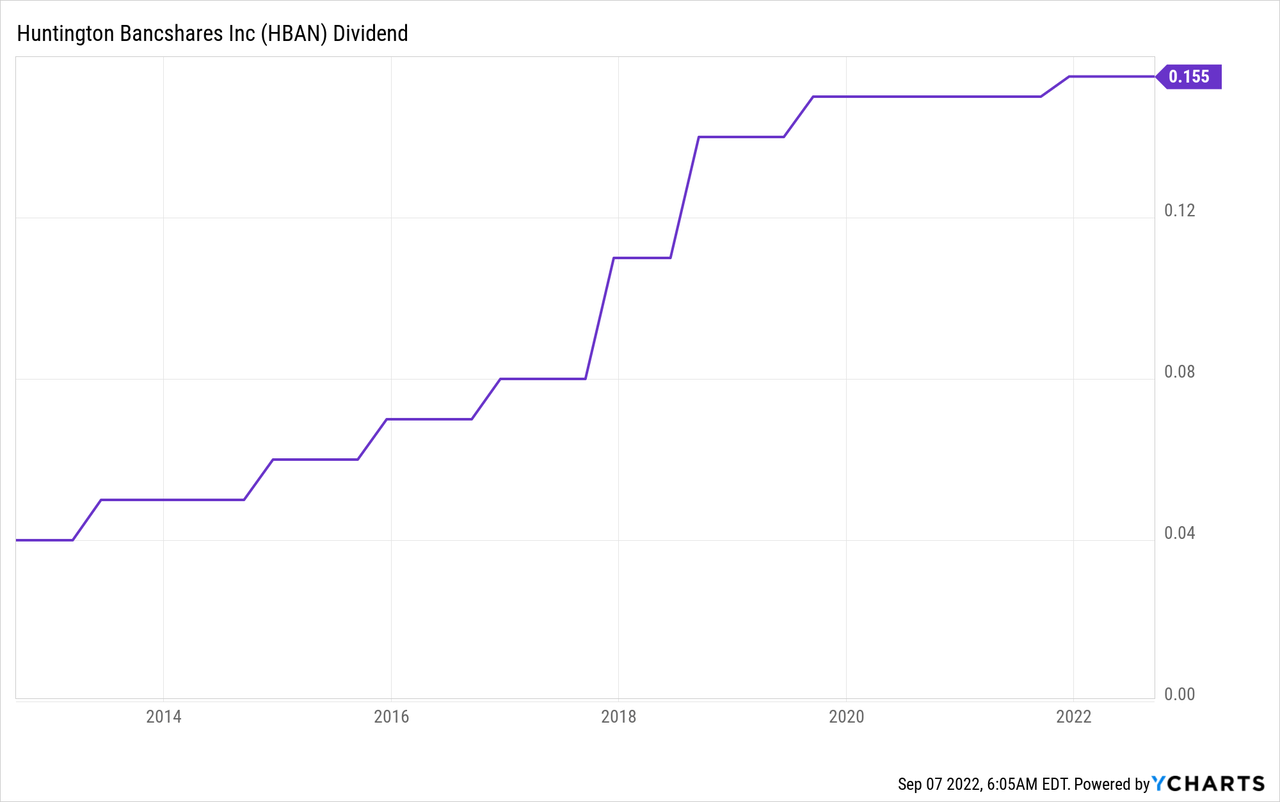

Short-term dividend growth is indeed quite bad as the company has just hiked once since the start of the pandemic. That hike was announced In October of 2021 when management hiked by 3.3%.

The good news is that since the Great Financial Crisis, dividend growth has been anything but underwhelming.

Over the past 10 years, the average annual dividend growth rate was 14.4%. The five-year average is a bit higher at 14.7%.

In these categories, the company scores A-.

With that said, I will also have to address the low score on dividend safety. After all, buying a high yield won’t do any good if it doesn’t come with decent safety. It’s like buying a luxury car that is likely to crash at any given moment.

The good news here is that while the company scores “low” on safety, it still has satisfying payout ratios, even if these ratios are above the peer median.

Seeking Alpha

It also helps that the yield comes with decent capital gains.

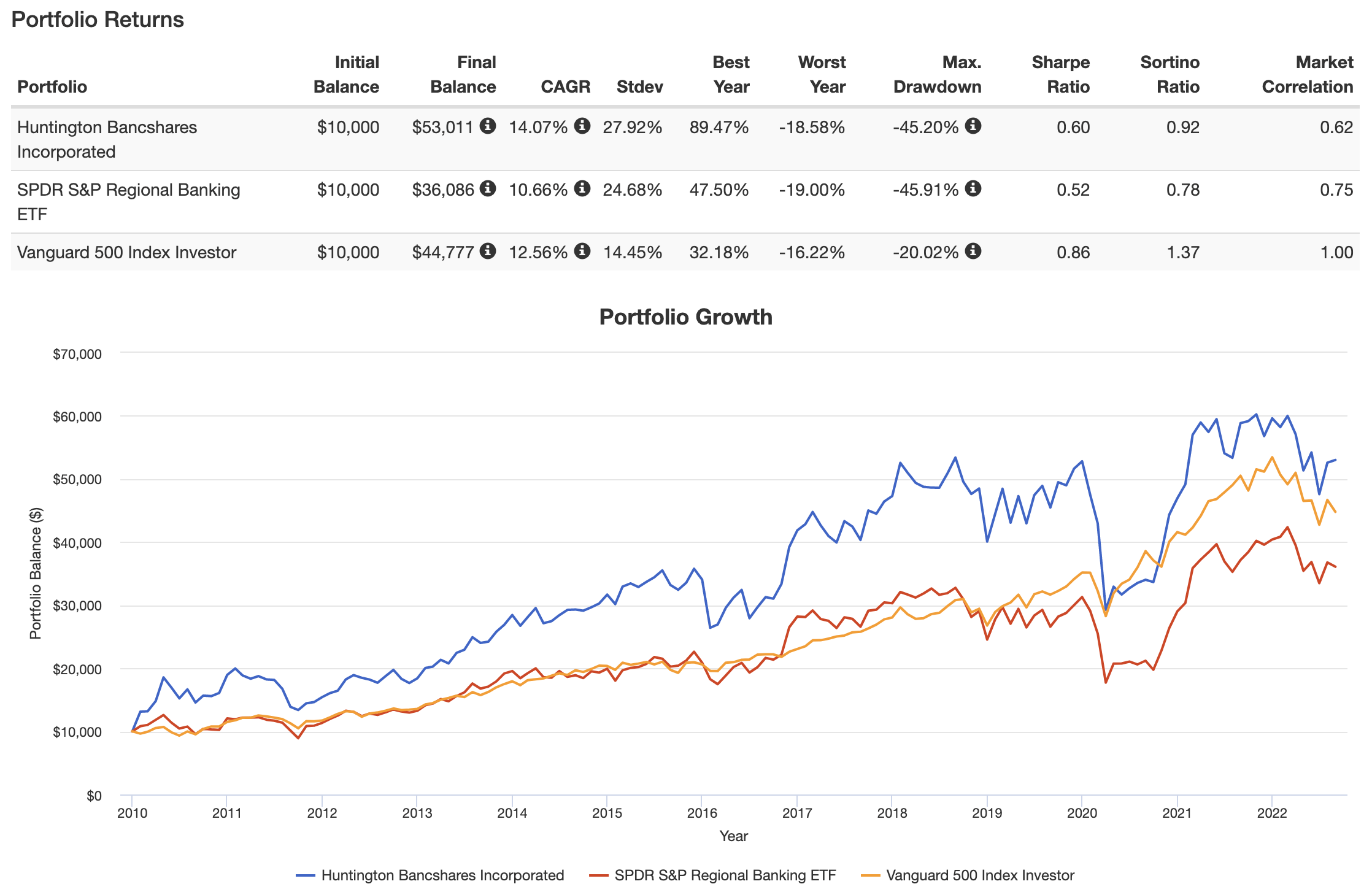

HBAN’s Long-Term Outperformance

Going back to 2010, HBAN has returned 14.1% per year with a standard deviation of 27.9%. This is a better performance than the SPDR Regional Banking ETF, which returned 10.7% – it also comes with a lower yield. It also beats the S&P 500, but not on a volatility-adjusted basis (Sharpe/Sortino ratios).

Portfolio Visualizer

HBAN investors have been prone to a few steep drawdowns. 25% drawdowns are tough, but it’s somewhat common. It has happened at least four times over the past 6 years. Including one sell-off of almost 60% when people thought the world was ending in early 2020.

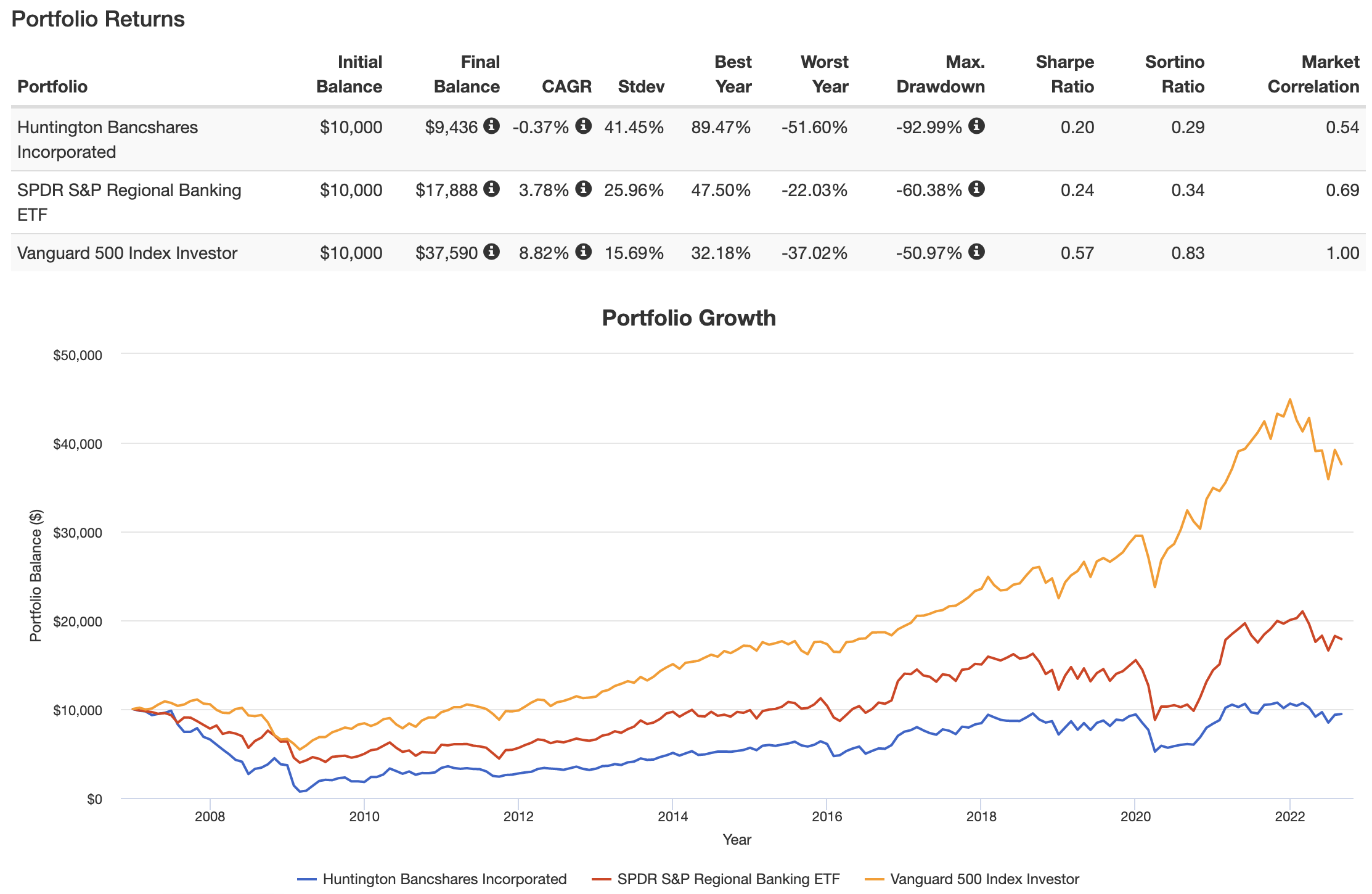

It also needs to be said that I was “cherry picking” (a little bit) when I showed you the outperformance chart above. Going back to the pre-Great Financial Crisis times, HBAN was unable to beat the market. Even worse, the stock has lost money as the 93% drawdown back then was just too much.

Portfolio Visualizer

The issue here is not that I expect a similar recession to happen anytime soon, but that regional banks, in general, come with high volatility, which hurts the long-term performance.

That’s why I will keep my exposure in HBAN limited, even though I’m not selling. I believe that the high yield makes the risk/reward fair for investors wanting to add more income to their portfolios.

It also helps that HBAN is evolving and becoming more than just a “boring” regional bank.

A Good Business, A Better Valuation

For example, the TCF merger is going smoothly. The company closed the transaction in less than six months. Total cost savings of $1.0 billion were achieved in 2Q22, one quarter earlier than expected.

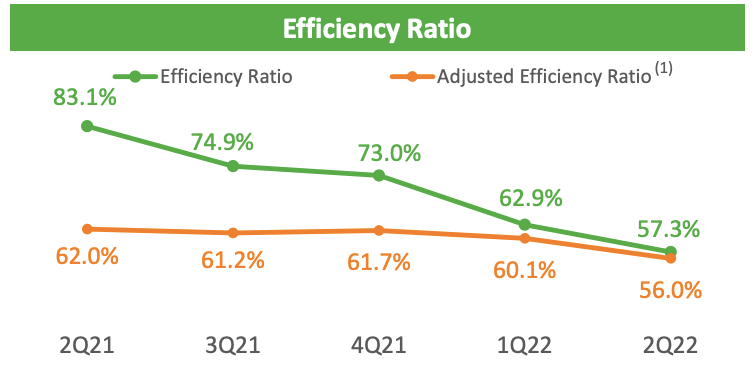

Moreover, the ROTCE (return on tangible common equity) was 20.6% in 2Q22 with an adjusted efficiency ratio of 56%, which makes the bank one of the most efficient with strong earnings power.

Huntington Bancshares 2Q22 Investor Presentation

Organic growth was strong with total loan growth of 2.5% in 2Q22 (versus 1Q22). Excluding PPP loans, growth was 3.0%.

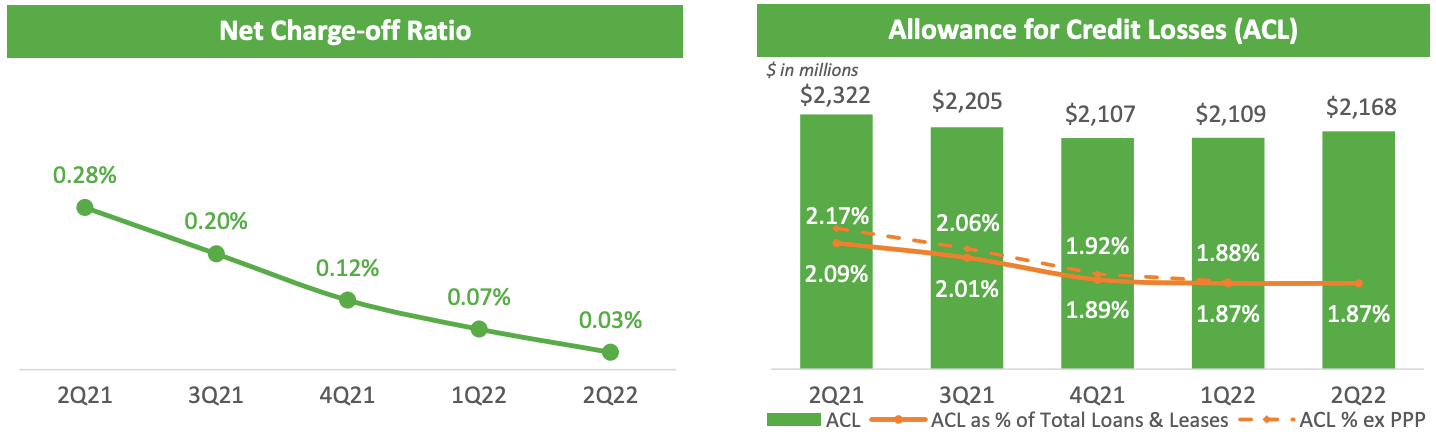

Even more important than loan growth is financial stability. Total net charge-offs were 0.03%. NPAs declined to 59 basis points.

Huntington Bancshares 2Q22 Investor Presentation

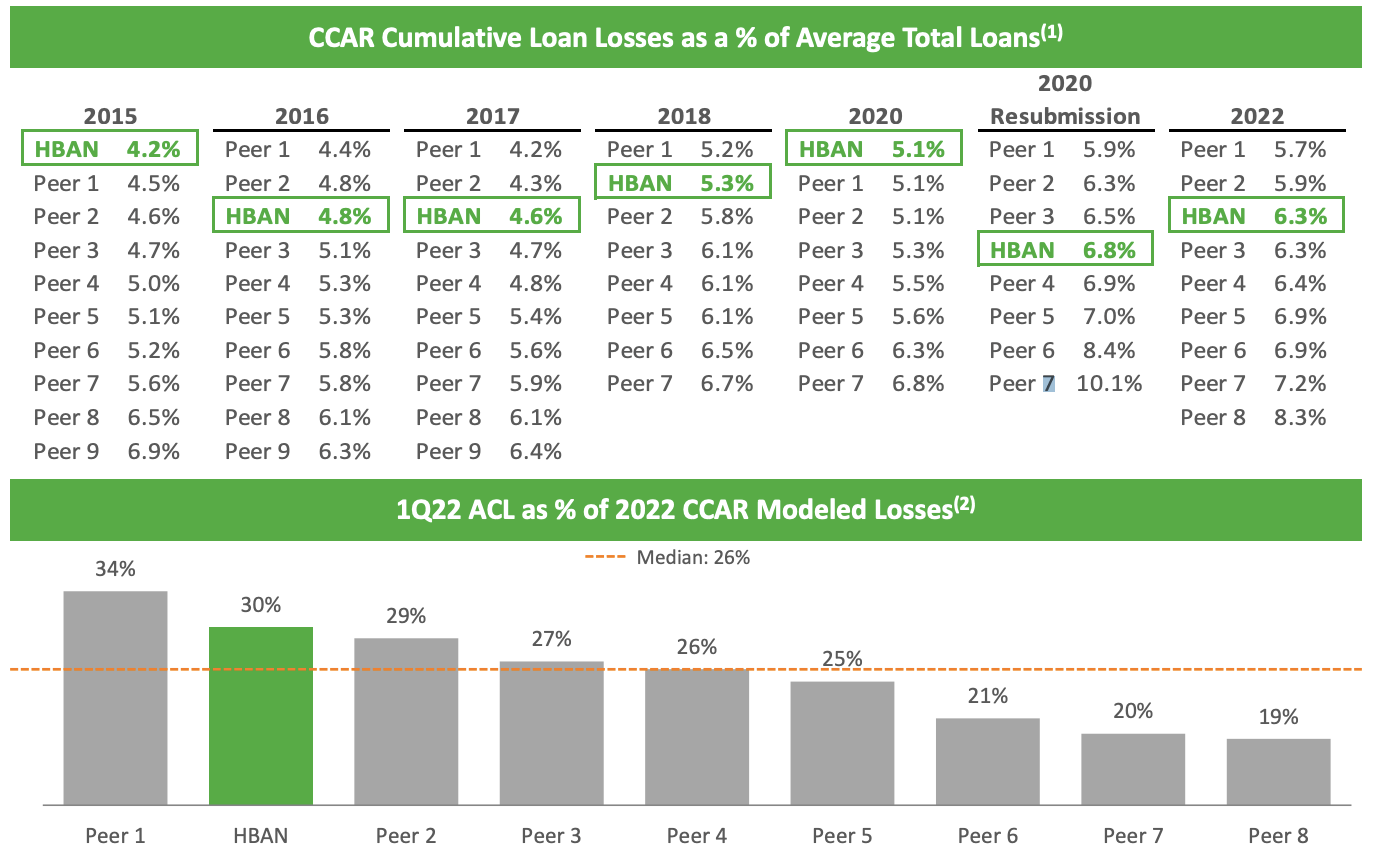

HBAN isn’t just doing well, it is even doing very well compared to its peers when it comes to loan quality.

Huntington Bancshares 2Q22 Investor Presentation

Moreover, the company has achieved all of its median-term financial goals.

- Total revenue growth above nominal GDP growth (5% in 2Q22 versus 1Q22).

- Return on tangible common equity of more than 17% (20.6% in 2Q22).

- Efficiency ratio of 56% – down from 62.0% in 2Q21.

- A CET1 ratio between 9-10%.

The company is also doing quite well when it comes to integrating Capstone Partners. This deal was closed on June 15 and it adds more investment banking exposure to HBAN’s portfolio. Capstone is a middle market investment bank and advisory firm with knowledge of 12 industry groups. Headquartered in both Boston and Denver, this company has more than 175 employees across 12 offices.

This deal could increase HBAN’s capital market fees from $168 million (annualized as of 1Q22) to more than $260 million.

This deal adds roughly 10 thousand mid-market clients who have so far benefited from Capstone services as well as expertise in aerospace & defense, energy, and FinTech, which is a big deal for HBAN as it is looking to become way more efficient and leaner.

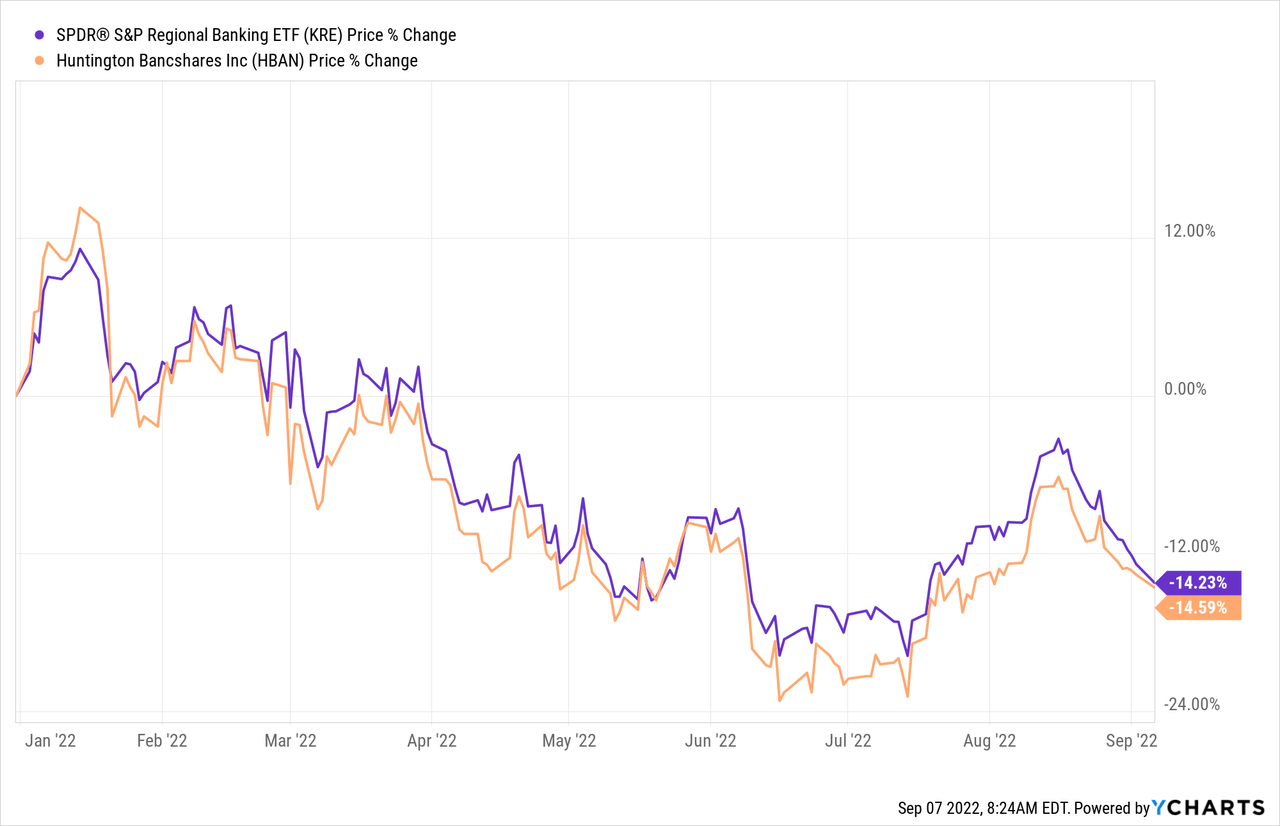

Unfortunately, despite all the good news, the company has not outperformed its peers year-to-date (excluding dividends).

This does by no means indicate that HBAN’s investments aren’t paying off. It does show that regional banks are slow-moving vehicles. They are truly snails who do go in the right direction, but very slowly. After all, the single biggest influence of regional bank charts is the macro environment.

Hence, I do believe that HBAN will continue to outperform its peers. But it’s not going to be noticeable when looking at short-term intervals like the YTD chart above.

But that’s OK. After all, we’re not buying for rapid capital gains here. I have other stocks for that with way more exposure.

What I need from HBAN is a decent yield and a good price in case I want to buy more. Right now, the price is good.

Valuation

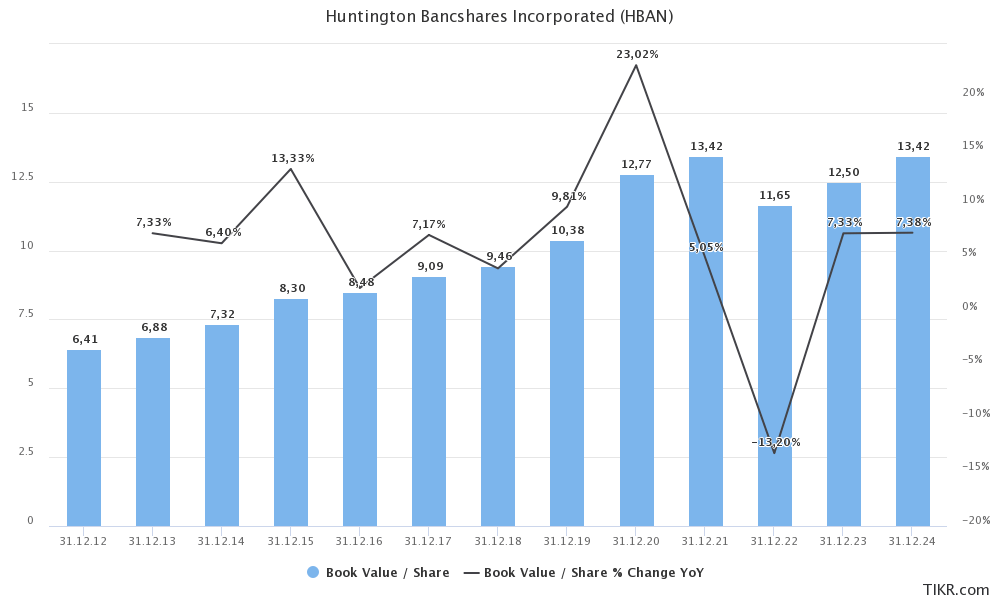

Between 2012 and 2024E, Huntington Bancshares is growing the book value per share by 5.8% per year. That’s a more than decent number supporting dividend growth and capital gains. Because the pandemic caused the book value to surge due to HBAN being a major player in government-backed loans, we probably won’t see record levels until at least 2024. But that’s okay. In 2024, HBAN is expected to end with a book value of $13.42. This would imply that HBAN is trading below its expected 2024 book value.

If we use 2023 numbers, the bank is trading at 1.05 its expected book value.

TIKR.com

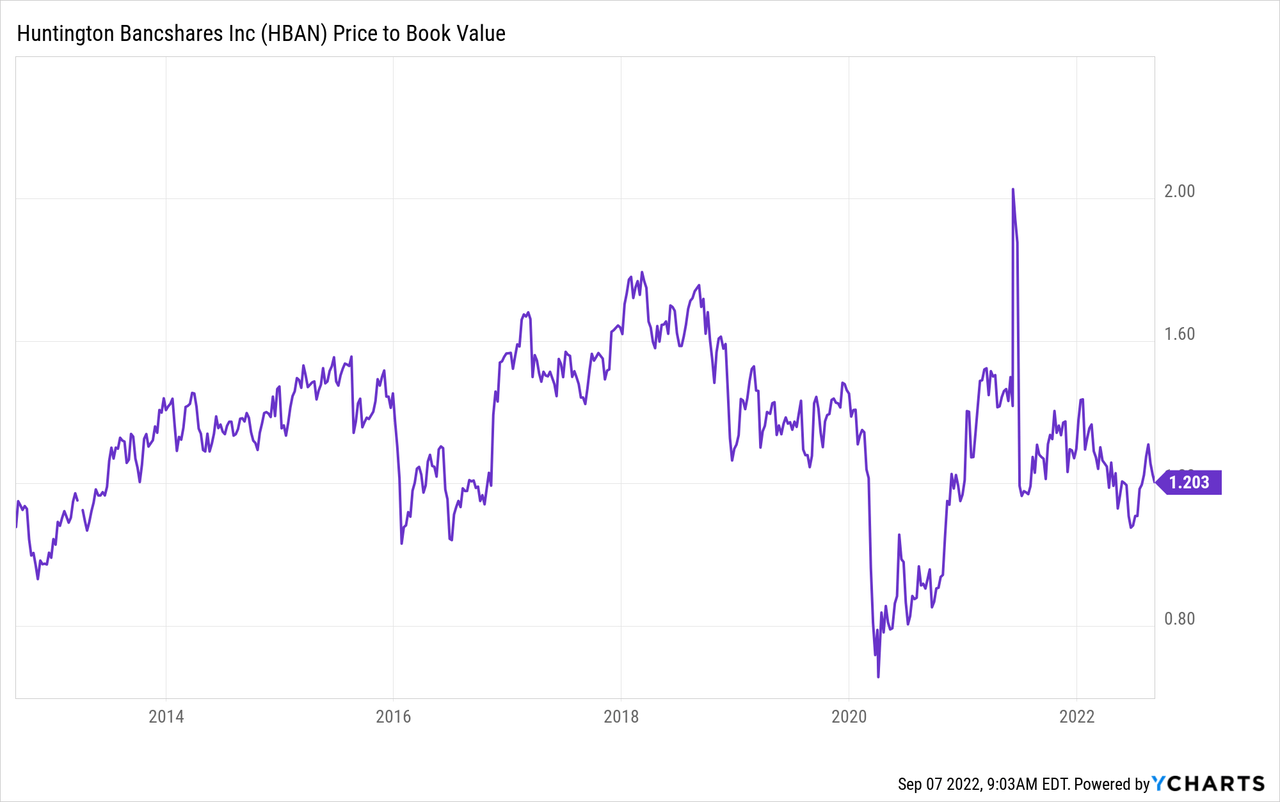

What this means is that if we’re not in for a devastating recession, the bank has a lot of room to grow its market cap/stock price.

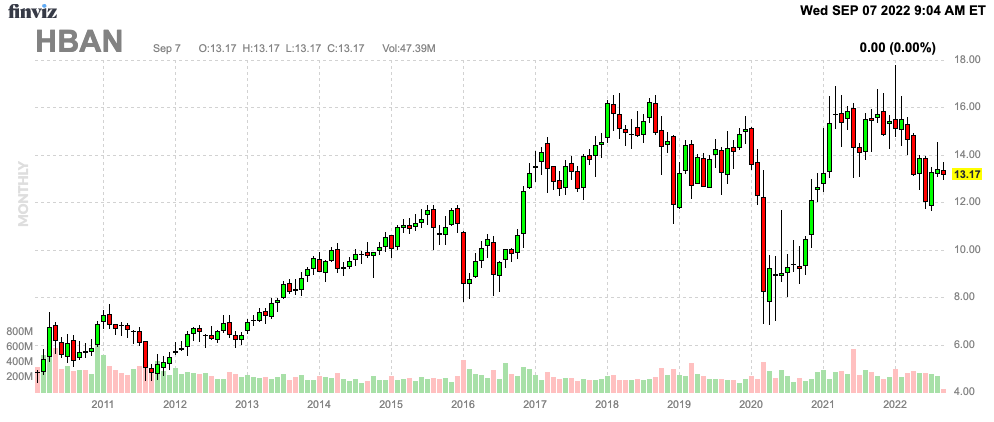

I would make the case that HBAN should not trade below 1.4x book, which means over the next 1-2 years, I expect a return to the $17-$20 range.

FINVIZ

Even if I didn’t like HBAN, I wouldn’t sell at a price below that range.

Takeaway

Huntington Bancshares is one of the most boring stocks in my portfolio. Like a typical regional bank, capital gains are somewhat underwhelming and the business model is everything except exciting.

But that’s OK. HBAN offers a great yield of 4.7%, and it has a history of satisfying dividend growth backed by a high-quality business with industry-leading credit quality numbers.

Right now, the stock is suffering from macro headwinds, yet if anything, it offers buying opportunities for income-seeking investors. Hence, I believe the stock is way too cheap given its earnings potential.

Going forward, I expect HBAN to outperform its peers and even the market as a whole given that the starting point is once again macro-related weakness.

However, as much as I like HBAN as a quality high-yield play, please keep your exposure limited. I am not a fan of investing “a lot of money” in regional banks – or any banks in general. HBAN does not have a favorable low-volatility profile, which is what I am usually looking for when investing in dividend stocks.

(Dis)agree? Let me know in the comments!

Be the first to comment