Robert Way

Investment Thesis: Hugo Boss (OTCPK:BOSSY) could see further long-term upside as a result of strong sales growth in the face of inflationary pressures as well as bolstering inventory levels to meet demand.

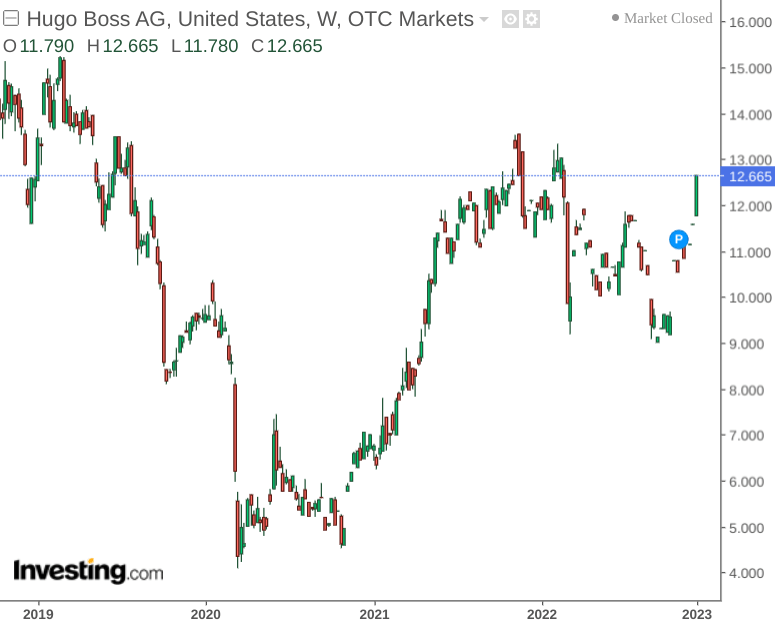

As a major apparel brand, Hugo Boss has seen a recovery in price to near pre-pandemic levels – after COVID-19 placed strain on the industry as a whole:

investing.com

With that being said, inflationary pressures and supply chain concerns placed pressure on the apparel industry as a whole in 2022.

The purpose of this article is to investigate whether Hugo Boss could continue to see longer-term upside in spite of such inflationary pressures.

Performance

When looking at the geographic breakdown of sales – taking Q2 2019 and Q3 2022 for comparison purposes – we can see that the European market now accounts for nearly 65% of sales in the most recent quarter as compared to Q2 2019, while sales for the Asia/Pacific market have declined from just above 16% to just below 12%.

| Europe | Americas | Asia/Pacific | Licenses | Total sales | |

| Q2 2019 | 60.44% | 20.59% | 16.30% | 2.67% | 100.00% |

| Q3 2022 | 64.42% | 21.11% | 11.90% | 2.57% | 100.00% |

Source: Calculations made by author – original net sales figures sourced from Q2 2020 and Q3 2022 Hugo Boss Quarterly Statements.

Additionally, when looking at actual growth in net sales over this period – we can see that Europe has showed the highest growth while that of Asia/Pacific has shown virtually none:

| Europe | Americas | Asia/Pacific | Licenses | Total sales | |

| Growth from 2019 to present | 47.30% | 41.73% | 0.91% | 33.33% | 38.22% |

Source: Calculations made by author – original net sales figures sourced from Q2 2019 and Q3 2022 Hugo Boss Quarterly Statements.

From a balance sheet standpoint, we can see that the company’s quick ratio has also decreased slightly over this period. Given that the quick ratio remains below 1, this indicates that Hugo Boss is still not in a position to meet its current liabilities using existing liquid assets.

| Jun 2019 | Sep 2022 | |

| Current assets | 1135 | 1523 |

| Inventories | 641 | 910 |

| Current liabilities | 806 | 1105 |

| Quick ratio | 0.61 | 0.55 |

Source: Figures sourced from Q2 2019 and Q3 2022 Hugo Boss Quarterly Reports. Figures provided in EUR millions, except the quick ratio. Quick ratio calculated by author as current assets less inventories all over current liabilities.

With that being said, we observe that inventories have seen a significant increase since 2019. The company justifies the increase in inventories as ensuring adequate supply for upcoming seasons including the Fall/Winter 2022 and Pre-Spring 2023 collections.

With group sales up by 18% in Q3 2022 as well as an increase of 27% as compared to 2019 levels – I am reasonably optimistic that Hugo Boss can bolster its quick ratio in future quarters as inventories come back to a more reasonable level. I take the view that given strong sales growth – it is better for the company to have a temporarily higher level of inventory to ensure demand can be met as opposed to not being able to meet sales demand due to lack of supply.

Additionally, we can see that non-current financial liabilities relative to total assets has decreased from 2019 to 2022 – indicating that long-term liabilities have been decreasing.

| Jun 2019 | Sep 2022 | |

| Non-current financial liabilities | 187 | 108 |

| Total assets | 2773 | 3014 |

| Non-current financial liabilities to total assets ratio | 6.74% | 3.58% |

Source: Figures sourced from Q2 2019 and Q3 2022 Hugo Boss Quarterly Reports. Figures provided in EUR millions, except the non-current financial liabilities to total assets ratio.

Looking Forward

Going forward, I expect that Hugo Boss is in a good position to continue bolstering sales. Even in spite of inflationary and other macroeconomic pressures – sales growth has not showed signs of slowing and I expect that the company can comfortably sell its existing inventory.

Moreover, given that we have seen a lower contribution of the Asia/Pacific region to total sales – I expect that this trend will continue as Hugo Boss continues to focus on the European and American markets.

Additionally, with the company having taken steps to expand its supply chains in Europe to reduce dependence on the Asia-Pacific region, Hugo Boss is positioning itself to be less vulnerable to the slowdowns in global supply chains that we have seen coinciding with the COVID-19 pandemic and an era of higher energy prices.

The main risk to Hugo Boss at this time is a particularly acute slowdown in economic activity which results in a drop in consumer demand. This would result in higher than expected levels of inventory for Hugo Boss which would take longer to sell and impact profitability. However, performance to date has been strong in spite of inflationary pressures.

Conclusion

To conclude, Hugo Boss has shown strong sales performance in the face of inflationary pressures.

While lower than expected sales growth could be a risk if economic conditions become particularly acute – I take the view that Hugo Boss has shown strong resiliency in the face of rising prices.

In this regard, I take a bullish view on the stock.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment