manaemedia

For those who follow Warren Buffett, it’s always nice to be able to pick up a stock at a cheaper price than what he paid for it initially through Berkshire Hathaway (BRK.A)(BRK.B). This actually happens more often than not, and was the case for Apple (AAPL), which dropped (and since rebounded) after he initiated a position years ago.

That’s because it’s hard to time the market and find an absolute bottom, and chances are good that you won’t find an absolute bottom on most of your picks either. This brings me to HP Inc. (NYSE:HPQ), which is a dividend stock that’s now trading below what Buffett had initially paid.

As shown below, HPQ’s share price has stagnated as of late and trades far closer to its 52-week low than its high of $41.47 achieved in June of last year. In this article, I highlight why value and income investors may want to considering layering into the stock at current levels, so let’s get started.

HPQ Stock (Seeking Alpha)

Why HPQ?

HP Inc. is a leading company in the design and manufacture of personal computers, printers, and imaging equipment. It came to its present form after the original Hewlett-Packard was split into HP Inc. and Hewlett Packard Enterprise (HPE), which focuses on products and services for enterprises. While most think of HP as being just a consumer business, it also does meaningful business with enterprises to equip corporate workforces.

In recent years, HP has been focused on expanding its presence in the global market. The company has been actively expanding its distribution channels and building strategic partnerships with other companies. Additionally, HP has been working to improve its supply chain and logistics operations to improve efficiency and operating leverage.

Make no mistake, however, that HP is a cyclical company. After seeing very strong results in 2021, driven by work from home trends, HP is seeing challenging comps as the good times don’t last forever and the PC market is slowing down.

This is reflected by HP’s fiscal fourth quarter net revenue being down by 11% YoY (8% decline constant currency) to $14.8 billion. This was driven primarily by a decline in HP’s core PC business, which made up $10 billion of revenue and down by 9% YoY constant currency.

Looking forward, I would expect for PC sales to remain pressured. This is supported by recent analysis from an industry analyst at IDC, who noted that PC inventories continue to remain high, with potential overhang in the first half of this year.

However, I see potential for HP to emerge from the current downturn in stronger shape as a more efficient enterprise. Management recently gave an update on its FutureReady program, which has delivered $1.2 billion in annual savings, ahead of the $1 billion that was originally planned.

Plus, make no mistake that HP is a cash flow generating machine in a mature industry, with relatively stable market share. The PC market is dominated by the top 3 players Lenovo, HP, and Dell (DELL), in that order. In fiscal 2022, HP generated $4.5 billion in operating cash flow and had a strong 87% free cash flow conversion, resulting in $3.9 billion worth of FCF.

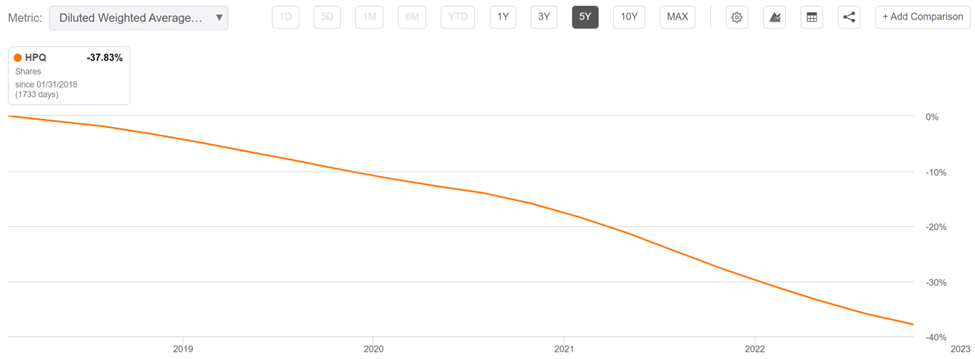

It’s also returning significant amounts of cash to shareholders, with $1.0 billion worth of share repurchases during fiscal Q4 alone, and raised the dividend by 5%. As shown below, HP has retired a whopping 38% of its share count over the past 5 years alone.

HPQ Shares Outstanding (Seeking Alpha)

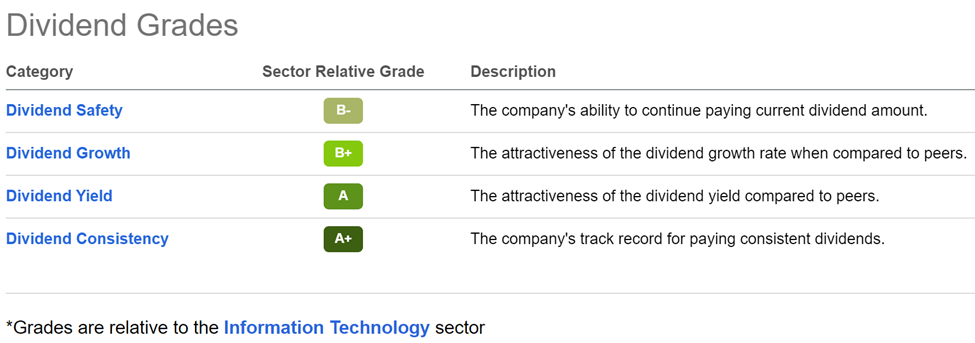

HP has also raised its dividend every year since becoming its current form in 2017. At present, HP pays a 3.8% dividend yield that’s well-protected by a 25% payout ratio. It also comes with a 5-year dividend CAGR of 13.5%. As shown below, HP scores A and B grades for dividend safety, growth, yield, and consistency.

HPQ Dividend Grades (Seeking Alpha)

Lastly, I find HP to be attractive at the current price of $27.69 with a forward PE of 8.4. This appears to be too cheap for a company that’s returning significant amounts of cash to shareholders at an attractive earnings yield. Plus, while analysts expect a rebound in business next year with estimated EPS growth of 11%. As such, I believe HP has the ability to generate strong shareholder returns from current levels for investors willing to be patient.

Investor Takeaway

HP Inc is a mature computer and peripheral device company with strong cash flow generation capabilities. It’s making good progress on reshaping its operating platform to become more efficient, and is returning significant amounts of cash to shareholders through share repurchases and dividend payments. While near-term headwinds remain, they appear to have been largely baked into the share price already, presenting long-term value investors an excellent opportunity to layer into the stock.

Be the first to comment