Torsten Asmus

Bonds have been a very tricky asset class over the last year. With the Fed raising rates at a historical pace after decades of being near the zero bound, bonds of all duration suffered through 2022 as the prices eroded. Even the traditional stalwart 60-40 equity/bond split portfolio took it on the chin in 2022.

The recent rise in short term rates has started to make bonds interesting again, especially against a backdrop of historically high inflation that the Federal Reserve is attempting to tame through interest rate increases. With short term rates now at 4.5% and the Federal Reserve seemingly committed to further hikes, albeit at a slower pace than the .75% hikes in 2022, the coupon rates on short term bonds will start to look attractive against the historic equity return rate of 7%.

Bonds can range in duration; the further out you go the more risk there is built in, whether it be geopolitical, currency or interest rate risk, just to name a few. I believe the best way to go about this is to go with shorter duration where we are more focused on the short term interest rates. I believe there is a short to mid-term skew down in interest rate risks which will make bonds issued currently more valuable over that time frame.

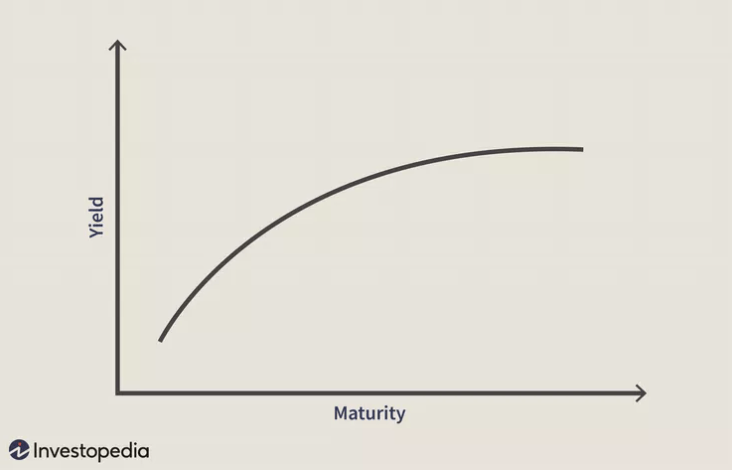

The Yield Curve

The yield curve is a graphical representation of the yields paid on bonds as time goes on. As noted above, the longer out the duration of a fixed income instrument, the more risk comes into play. In most instances during the business cycle, investors are compensated for this duration risk with higher interest.

Normal Yield Curve (Investopedia)

There exist periods of time during business cycles where the yield curve inverts with short term rates exceeding long-term rates. This occurs because the near term is considered substantially more risky to investors so they are shifting resources out of short-term instruments and into longer term maturities, bidding up the value of long term bonds and reducing the yield on them. This is usually a pre-cursor to recessions as capital is leaving the system and seeking safety amid concern about near term economic prospects. As we can see below, the current US treasury yield is inverted, which is a very good predictor that a recession is likely to occur:

US Treasury Yield Curve (Ustreasuryyieldcurve.com)

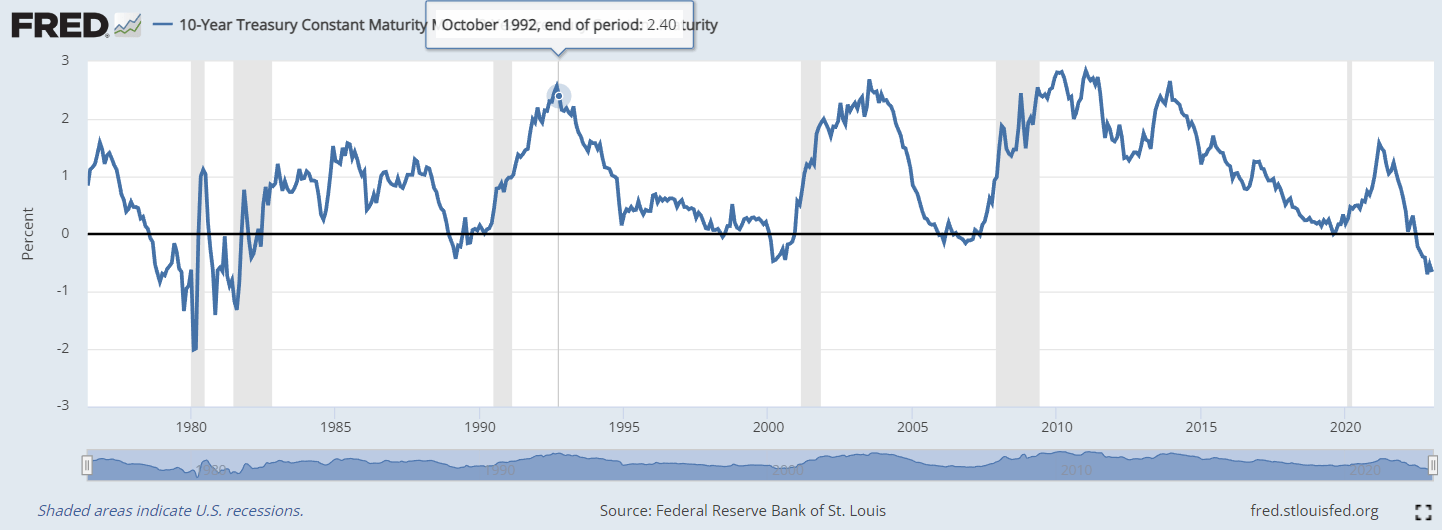

If we pull out and look at economic performance over the last 4 decades, we can see that this inversion of the yield curve has in fact been predictive of a recessionary outcome in the near term:

Yield Curve Inversion (St. Louis FED)

This inversion between the 10 year and 2 year bonds has been in place now since July and is the deepest inversion since 1980 when Paul Volcker was dealing with the massive inflation coming out of the Carter Administration and raised rates to 20% to get it under control.

This potential fear is the biggest risk to investing in bonds in the near term; increasing interest rates decrease the value of existing bonds due to the fixed coupon rate. There has also been a substantial narrative in the media where they compare the government’s CPI rate to the Fed Funds interest rate with the assumption that the CPI rate needs to be below the interest rate in order for the Fed to stop raising rates or to in fact reverse course. These are very different denominators and the biggest issue is the CPI is being driven less by demand and more with global supply issues.

Raising interest rates essentially transfers spending from the real economy to debtholders. However, inflation is being felt most in the basics for people, such as food, shelter and energy. Those costs can’t be avoided so a rising interest rate environment simply increases the overall costs on those that can least afford it.

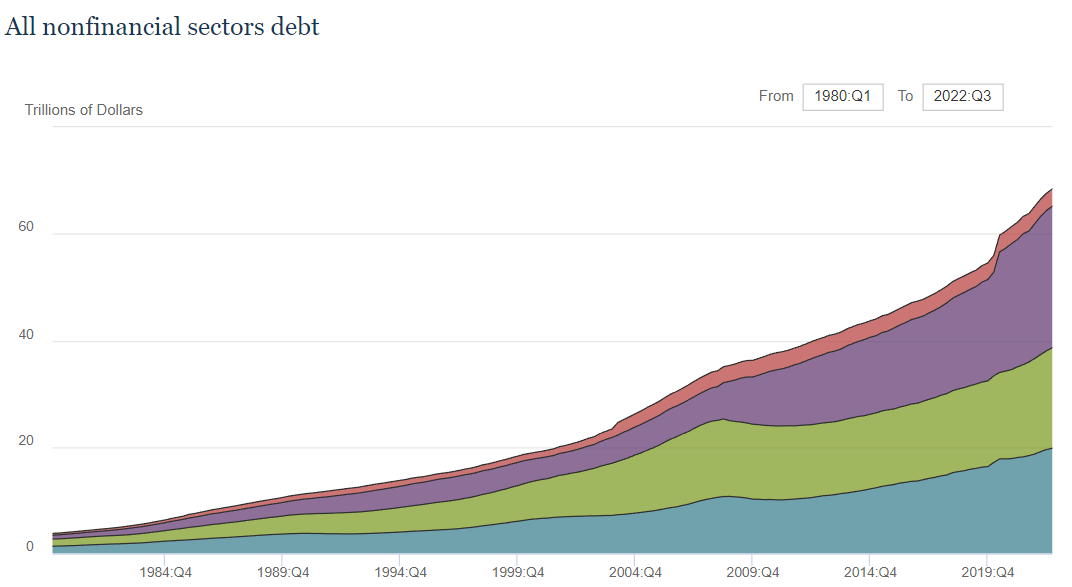

The sensitivity of the economy to interest rate increases is also substantially higher than the 1980 time period due to the massive level of debt throughout all economies. We can see below that the absolute debt value in 1980 was $3.8T and has not increased to over $68T through all levels of the economy, including the public sector. These costs are borne both through taxes and interest costs.

Non-Financial Debt Levels (federalreserve.org)

During this same time period, the population has increase from 223m to 340m. This is a massive explosion of debt through all levels of the economy. Government debt has been the primary driver of this as there has been little to no effort to ever balance the budgets. However, even at the private debt level, the average debt load has increased threefold during this same time period:

Debt to GDP levels (IMF)

This means that Powell’s Fed is already getting very close to having the same impact on the economy that Volcker did back in 1980. If we then consider the anemic rise in wage rates until recently, it can be argued that we are in as tough or worse a situation right now than in 1980.

Yes, But Why Should I Buy Bonds Then?

All the above shows is that the Federal Reserve has already put in a very putative interest rate environment. It was done quickly because they had left such an accommodative environment in for so long that excesses were occurring in almost all areas of the economy and financial markets. I believe that if I, just some guy writing on Seeking Alpha, can pull the above together, so can they. The worry is that they are either dogmatic with the narrative of comparing CPI to the interest rate or that they have not waited long enough to see the impacts. As variable debt instruments reset and other debt comes rolling off both household and corporate balance sheets, this punitive interest rate regime will begin to have a drastic effect on the economy, which will force the Fed to drop rates and thereby driving bond prices up.

And How Should I Play This?

There are innumerable number of ETFs that allow you to invest in bonds. A lot involve corporate bonds as well, as they can give higher interest rates than sovereigns do. This does introduce individual corporate risk, but could juice your returns. Interest returns from ETFS will not match the current rate as they are setup where bonds are rolled over whatever time frame you are investing in so the higher rates will ease in over time, depending on the duration. There are also ETFs that support bond laddering with specific term end dates, but

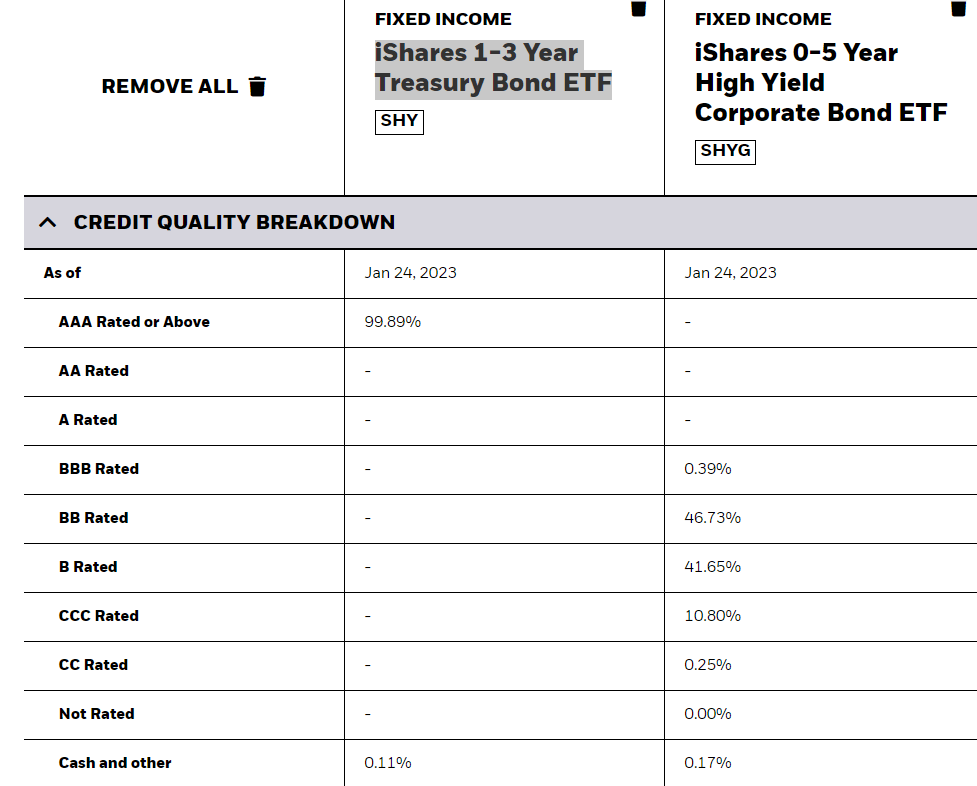

I have narrowed it down to two options: iShares 1-3 Year Treasury bond ETF (NASDAQ:SHY) and iShares 0-5 Year High Yield Corporate Bond ETF (SHYG). Both these are rolling in nature, so the higher interest rates will see a gradual increase to the dividends investors receive as the higher interest items. The credit quality for the High Yield is in the BB and B range, while the Treasuries are understandably the highest.

iShares Short Term Bond ETF Comparison (ishares.com)

We are trying to profit here from a reversal in interest rates rather than from the yield; if you are looking for some yield, using SHYG (in whole or in part) could be useful but I am going to use the SHY ETF in order to gain what I believe will likely be a relatively sharp interest rate reduction sometime over the next 12 to 18 months as the Fed realizes how punitive this interest rate environment now is. The yield will increase the longer the rates remain high as they roll these bonds. The duration of it is also 1.81. years which closely matches the time frame we are looking at while SHYG is 2.35, a little longer dated with some potential credit risk as well.

The Takeaway

With a likely recession coming and a potential reversal of the Fed’s interest rate policy, it will likely be a very difficult time for equities, especially the longer the Fed keeps the high cost of borrowing intact as earnings contract. SHY will provide an increasing yield as the bonds roll forward in the short term while also adding value when the Fed eventually reduces interest rates to support the economy when the recession takes hold. Straight treasuries are likely the best alternative, but this ETF gives some easier liquidity.

Be the first to comment