Pgiam/iStock via Getty Images

We have not covered Houlihan Lokey (NYSE:HLI) in a while. It is relevant now because we are having concrete credit events. Discussion around restructuring has mainly been maturity management, some minor liquidity concerns, and the famous ‘dialogue’ where no action was really needed with clients. The collapse of SVB Financial is going to create lots of issues, and regional banking broadly taking a hit means that as banks recalibrate with markets, they’ll be stricter with lending and companies are not going to be able to refinance as easily or at all. HLI is quite unique in that its roots are West Coast and not Wall Street, as shown in the stock image to this article, and with mid-cap being an area HLI addresses well, as especially with expertise in helping companies monetise illiquid assets, HLI is actually relatively well positioned for this crisis which is starting in the West and will generally concern less established businesses first. However, we would not pay the current multiple given the extent of resilience we expect from the decently large dedicated HLI restructuring business. The normal activity could truly crater now, even in mid-cap which has been resilient, and confidence in a sponsor return should be very low considering the non-linear dangers in markets.

Quickly on HLI’s Q3

They have pretty recent Q3 results that we’ll blaze through. Compared to Greenhill (GHL), which we recently covered, everything looks terrible. Greenhill grew sequentially while HLI didn’t, Greenhill didn’t fall much YoY on either the 3 month nor the 9(12) month basis compared to HLI, which fell more than any peer we’ve covered. Greenhill is more idiosyncratic and can have specific business wins buck industry trends while HLI less so.

However, HLI had absolutely monster 2021 results compared to 2020, while Greenhill didn’t do very well at all in that regard, barely growing. Still, the sequential difference is notable, and does not play to HLI’s favour, likely highlighting the fall off of sponsors this year.

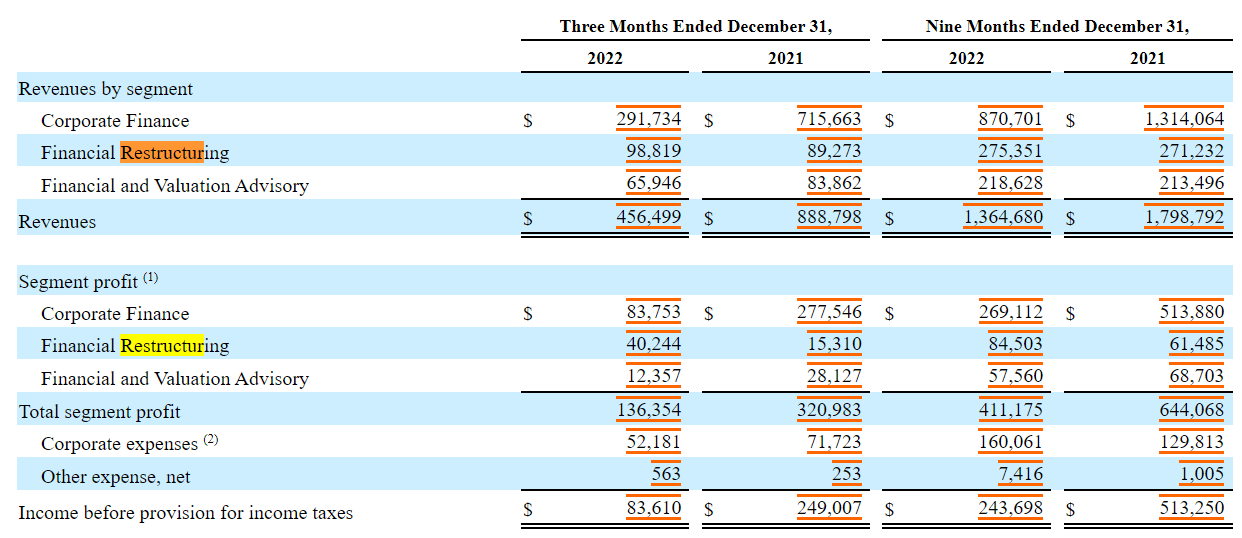

HLI saw little growth on the restructuring side of things, consistent with what we hear from peers, but with the return to more normalised levels in the corporate finance and fairness opinion businesses, we are getting a larger rep of restructuring in the HLI mix at around 20% as of the latest run-rate figures. Not as much as in 2020 but not bad.

Segments (10-Q HLI)

Restructuring

Restructuring is the thing to look at now, because it’s countercyclical. Everyone knows that. 20% is a decent hedge, since a huge boom in restructuring activity could mean this triples in absolute terms, and takes over the mix as corporate finance activity plummets.

We think that CF activity is going to struggle this year even more than last. While mid-cap was a hold out after megadeals died and sponsors shied away from markets due to the death of the LevFin markets with the rate hikes as well as impaired investments from an exuberant 2021 allocation, they will not continue to do well, especially as financing conditions deteriorate with the higher rates now distinctly hitting the credit cycle.

Restructuring could pick up the slack and more, because these deals can be very big, and with a lot of trouble in the financial world, complex balance sheets may shine a light on HLI which is especially good with weird assets. Moreover, HLI is originally a West Coast IB, which is unusual, and could have an advantage with most of the issues in the US economy starting to sprout from California with the regional bank runs and what is going to be a mess of a startup and early stage environment. With innovative businesses also being the most exotic, HLI may have even more of a role to play as a leading restructuring player. They have good FIG relationships in smaller caps, have been growing their general FIG exposure, and are generally mid-market focused so they have things going for them since that’s where issues are going to be focused, not larger companies and institutions that have better capital market access and can avoid major issues like restructurings.

We don’t know deeply their regional quirks, but their Bay Area office also seems to be pretty big compared to LA or NYC, compared to other companies of a similar size, which are more NYC or LA heavy in terms of headcount. Certainly it has a similar presence on the West Coast as the East.

Finally, government finances are more stretched lately, and it’s possible rate hikes need to continue regardless of some of these credit events. Moreover, there’s the debt ceiling issue, and a lot of other factors that could impact credit markets. Restructuring is more likely than at most times to have a heyday as companies require help and connections to succeed in managing their financial situations.

Bottom Line

The problem is multiple. You’re paying over 20x on trailing earnings in PE, and on broadly held forecasts you’re still paying around 20x. They could be resilient with restructuring, but it’s more than likely earnings will fall and the net situation will be negative if more credit events are in store for the US. There are other resilient businesses out there with lower multiples. Buy those instead. Nonetheless, we think that HLI should have better earnings performance than many of its peers. While FIG isn’t its biggest focus, they are big on restructuring, and restructuring could become an important market. Other companies can shift their personnel over to restructuring, but HLI’s dedicated presence should be an advantage.

Be the first to comment