art Photo

Shares of Ireland-based Horizon Therapeutics (NASDAQ:HZNP) have risen by 237% since my 2016 recommendation identified the company as an attractive Core Biotech-type selection. However, so far in 2022 shares have lost 40% of their value.

I’ve had this rare disease player on my radar for quite a while as a possible addition to our current Core Biotech portfolio. One would think fair value is considerably higher than the current $14 billion market capitalization, considering growing Tepezza sales in the lucrative TED market ($3B+ peak potential), Krystexxa sales hitting an inflection point to help patients suffering from gout and pipeline contains drug candidates with $10B+ in peak sales potential across a range of diseases and settings.

As share price and valuation have hit relative lows, I think it’s time I revisit this one to see if it’s ready for us to add to the Core Biotech portfolio.

Chart

FinViz

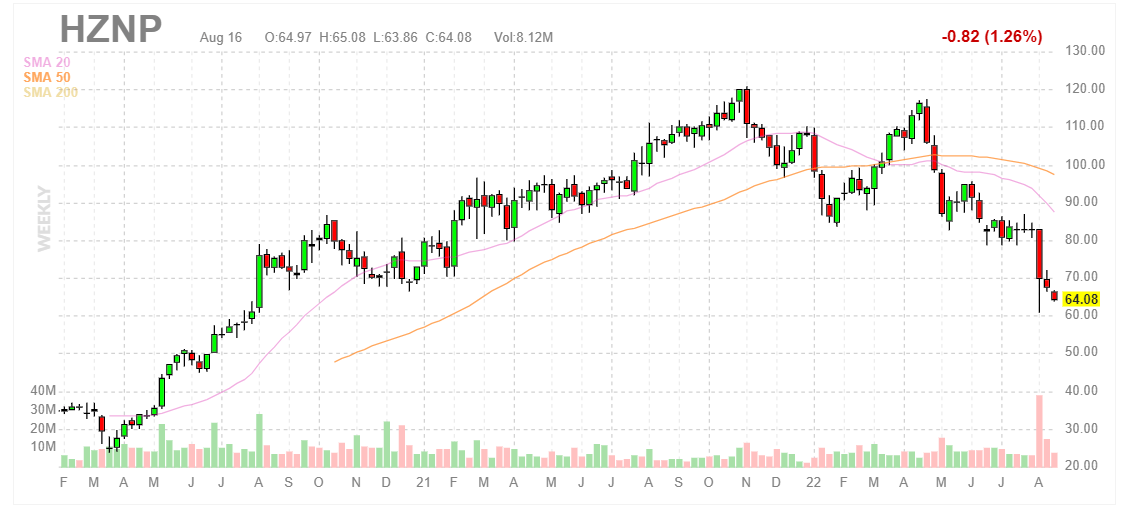

Figure 1: HZNP weekly chart (Source: Finviz)

When looking at charts, clarity often comes from taking a look at distinct time frames in order to determine important technical levels and get a feel for what’s going on. In the weekly chart above, we can see share price top out at the $120 level twice in late 2021 and again in 2022. From there, they’ve steadily drifted south after multiple disappointing quarters as pessimism takes over. Current range in the low $60s appears to be establishing a near-term low, but I would not overestimate the ability of short sellers to take this one lower still. My initial opinion is that long term investors would do well to accumulate a pilot position in the near term, adding further exposure spread out across Q3 and Q4 reports in order to encourage patience and possibly attain a better average cost.

Overview

Management presentation at Goldman Sachs Healthcare Conference is a worthwhile listen to gain better understanding of the present picture:

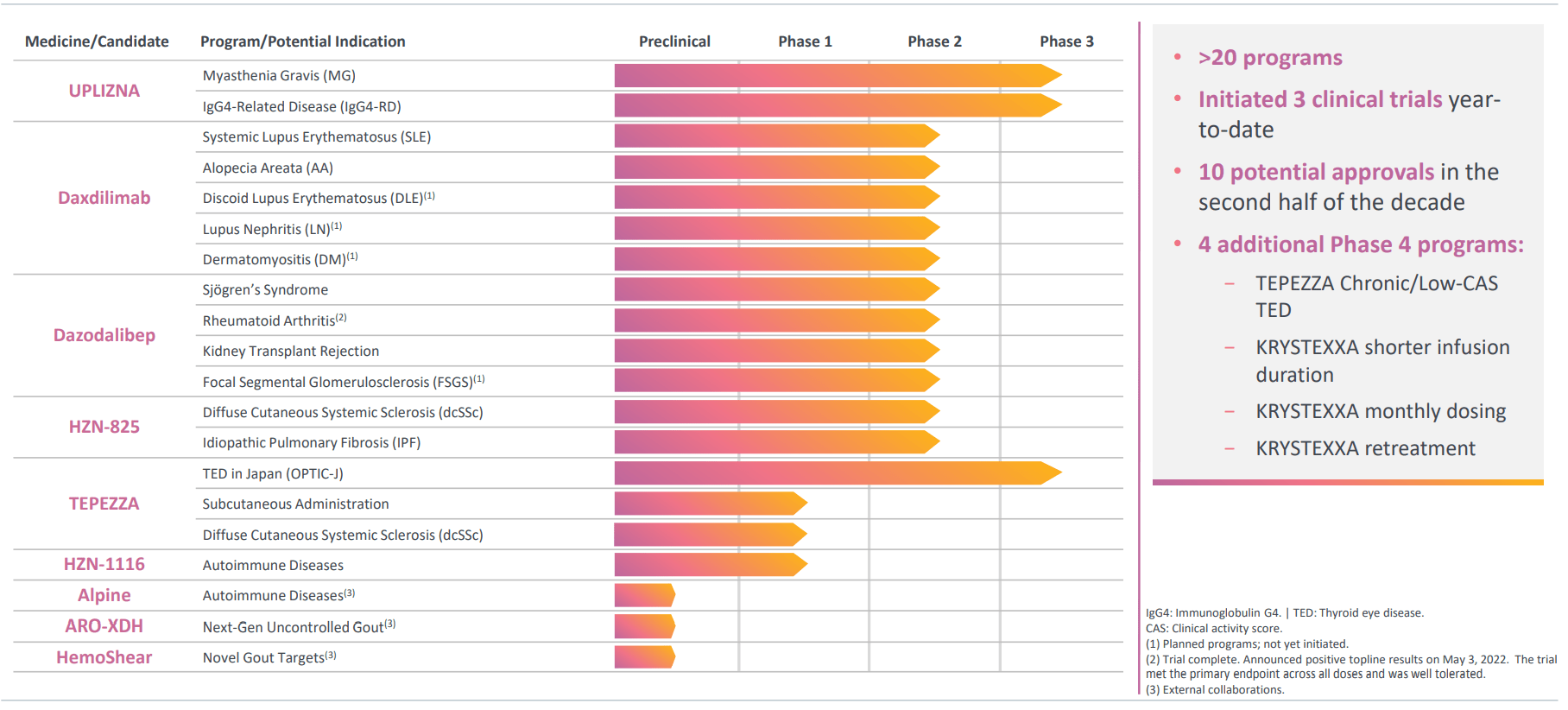

- Long term growth is being driven by 3 lead approved rare-disease drugs with combined $5.5 billion in peak sales potential (Tepezza in TED, Krystexxa in gout and Uplizna in MG). Behind these, the company has 20+ clinical programs ongoing with combined peak sales potential of over $10 billion.

Corporate Slides

Figure 2: Deep pipeline (Source: corporate presentation)

- Management has a strong track record in savvy business development and knows how to get deals done. They always start with the question of whether the opportunity being examined is strategically aligned with their objectives as a rare disease company. They are currently looking at individual assets to expand the pipeline, looking at growth into late 2020’s and beyond. They are scaling geographically as well, with Tepezza being the anchor of these efforts.

- They do evaluate larger bolt-on deals from time to time as well, IF they meet the derisking criteria such as coming with a commercially approved product plus a pipeline for diversification. Management asks themselves whether they can add value to what they receive, such as Uplizna and the 2021 deal to acquire Viela Bio for $3.05 billion with opportunity inherited to expand to additional indications.

- They are VERY disciplined from a valuation standpoint. Management notes that the overall XBI may be 60%+ off from its peak, with some smaller cap stocks down 70% to 80% which could be cheap but NOT attractive. Other companies sport more attractive valuations that have not fully reset yet. They are confident in their commercial capabilities in the rare disease business model, providing support and specialty marketing efforts which they do very well. They are thoughtful and intentional in thinking about how to develop products, get a good regulatory outcome and position them for successful launch.

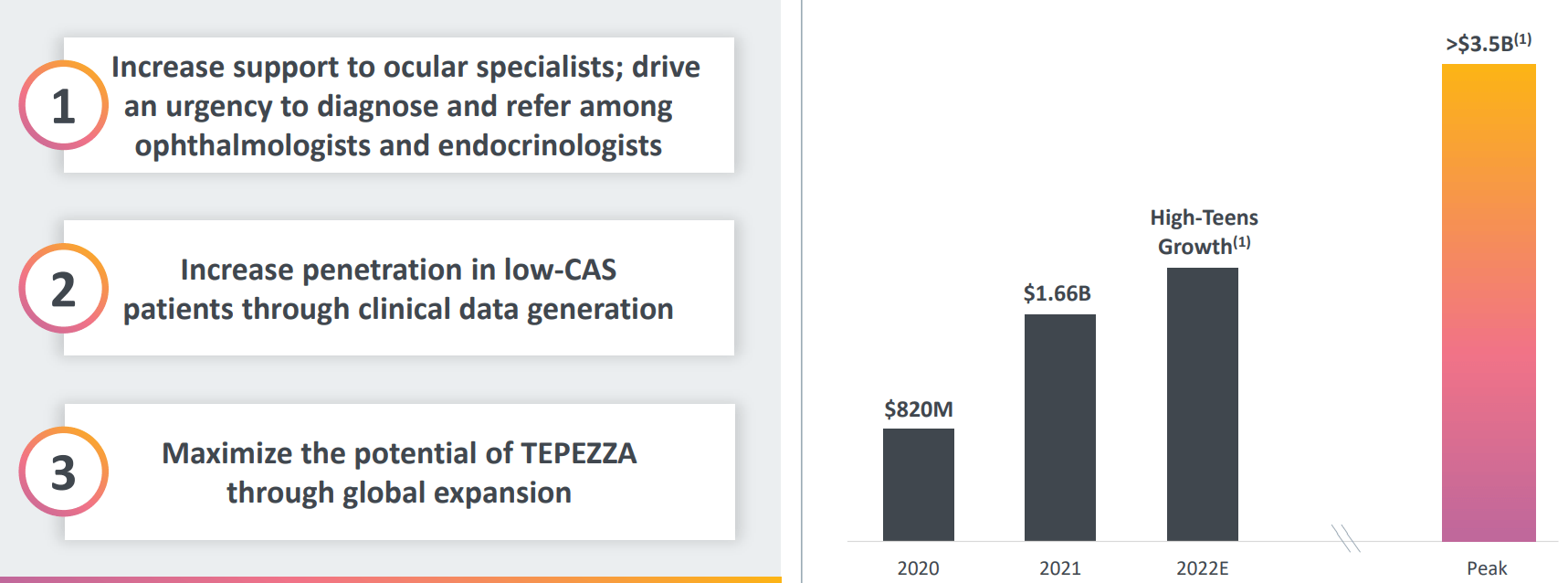

- Focusing on core asset Tepezza in TED (Thyroid Eye Disease) market, management expects sales to reaccelerate in the back half of 2022. They have expanded the field force to call on a broader range of targets. Simply put, more resources will drive greater conversion and they will provide more support to help patients come onto the funnel and get care. Success in chronic TED could be a catalyst to grow sales as well, demonstrating benefit in patients with low activity scores. 2 years into launch management found out there are not discrete phases of disease such as acute and chronic, as they come across patients with range of symptoms since diagnosis. On the con side, management will not commit to revisiting their long-term guidance so perhaps there’s insufficient clarity there.

Corporate Slides

Figure 3: Key growth drivers for Tepezza and projected peak sales ramp (Source: corporate presentation)

- As for Krystexxa launch in combination with immunomodulators to expand the market opportunity in uncontrolled out, management notes that this overall gout market consists of over 9 million patients growing at single digits annually. Krystexxa is appropriate for over 100,000 patients and tapping a low % of that currently, so there’s lots of upside from here. 4% infusion reaction (patients more comfortable when considering whether to go on treatment) and 71% complete response are encouraging. They are also expanding efforts to address gout via collaboration with Arrowhead Pharmaceuticals (siRNA) and other drug candidates, with the goal being to address the hundreds of thousands of patients for whom current therapies do not work, are contraindicated or have safety concerns with existing products. The goal over time is to bring a portfolio of products forward to address the broader need and create a really powerful gout franchise.

Corporate Slides

Figure 4: Impressive improvement in CR rate leads to increased use of immunomodulation (Source: corporate presentation)

- Moving on to Uplizna and the NMO opportunity, they are in the process of relaunch (Q4) and positioning with expanded sales team and reinforced infrastructure around the brand. Goal is to help folks get on treatment faster and help physicians get through reimbursement more efficiently while continuing to generate data through the field support team. They are seeing that the majority of patients are switchers, but they do have a decent amount of treatment naive patients as well. This reinforces management’s belief that Uplizna is a next generation B cell depleter and physicians are buying into that as they switch from rituximab. Also, they are able to provide a more constant regiment with 2x/year dosing and more certainty to have disease under control. This is especially important considering that a single attack can cause irreversible blindness or paralysis (no partial recovery such as with multiple sclerosis). The myasthenia gravis landscape also allows them to differentiate from novel FcRns like Argenx (ARGX) where patients are getting weekly infusions four times then waiting 80 days to see if they need further infusions. Data also positions Uplizna to be studied in MuSK patients and they will have the largest data set to show efficacy in this population. Another unique feature they offer is steroid taper, to show many patients weaned off of steroids and thus avoid their long term health consequences.

Other Information

For the second quarter of 2022, the company reported cash and equivalents of $1.89 billion as compared to $2.6 billion in debt outstanding and positive operating cash flow of $249 million.

Shares took a hit when Q2 earnings were released considering that full year guidance was below estimates, with company expecting full year net sales of $3.53B – $3.60B versus prior guidance of $3.9B -$4B. Also, they now expect Tepezza full year net sales percentage growth in the high teens versus prior guidance of mid-30s percentage growth.

Key development programs moving forward included:

- Anti-ITL7 monoclonal antibody daxdilimab in phase 2 study for systemic lupus erythematosus (SLE), disease in which the body’s immune system attacks its own tissues and organs. Phase 2 trial in alopecia areata, phase 2 study in discoid lupus erythematosus (DLE), phase 2 study in lupus nephritis and phase 2 study in dermatomyositis (rare autoimmune disorder characterized by rashes, debilitating muscle weakness and interstitial lung disease).

- CD40 ligand antagonist dazodalibep in multiple studies in autoimmune diseases, including phase 2 study in Sjögren’s syndrome, phase 2 study in rheumatoid arthritis, phase 2 study in kidney transplant rejection and phase 2 study in focal segmental glomerulosclerosis.

- Oral lysophosphatidic acid receptor 1 antagonist HZN-825 in pivotal phase 2b study in diffuse cutaneous sytsemic sclerosis and phase 2b pivotal study in idiopathic pulmonary fibrosis.

- Anti-CD19 humanized monoclonal antibody Uplizna in phase 3 study for myasthenia gravis and phase 3 study for IgG4-related disease.

- Tepezza phase 4 study in chronic/low-CAS TED, phase 3 Japan study in moderate-to-severe active TED, subcutaneous administration phase 1b study and phase 1 study in diffuse cutaneous systemic sclerosis.

- Krystexxa phase 4 trial evaluating methotrexate combo over shorter infusion duration in uncontrolled gout, monthly dosing phase 4 study and retreatment phase 4 study (patients who were not complete responders to monotherapy).

- HZN-1116, fully human monoclonal antibody that neutralizes function of FLT3-ligand in phase 1 study in patients with autoimmune diseases.

Moving on to the conference call, management highlights 13% growth in orphan disease segment of the business and 30% growth for Krystexxa. For TEPEZZA in TED, market research confirmed estimates of over 100,000 patients in the US appropriate for treatment in the US (segmented based on disease severity and clinical activity score or CAS). They estimate more than 20,000 patients with high CAS and key severity symptoms such as high proptosis and diplopia. This is the market where they have highest penetration rate at 20%. They also estimate more than 80,000 patients in the next segment of TED with low clinical activity score with high proptosis or diplopia (seen low single digit penetration of this segment today). The challenge here will be to address low awareness of the disease with ophthalmologists and endocrinologists. The company expects more meaningful uptake based on data sets generated beginning in 2024.

Moving onto Krystexxa, again they saw 30% year-over-year growth driven by growing adoption in both rheumatology and nephrology market segments as well as uptake with immunomodulation (running at 50% of new patients). Expanded label is allowing them to promote the benefits of methotrexate for the first time and management remains confident in attaining peak annual sales of more than $1 billion.

Uplizna delivered another strong quarter as well with net sales of $39M, with commercial launch underway in Germany. Management remains confident in global peak annual net sales expectation of over $1 billion across all indications.

As for prior financings, March 2019 secondary offering took place at $24.50 (less than half the current share price and a reminder that management has successfully created shareholder value over the past few years).

Accumulated deficit (retained earnings) now stands at positive $318 million, which I think is quite impressive considering the company was founded way back in 2005.

As for insider holdings, President and CEO Timothy Walbert owns ~435,000 shares or over $26 million worth.

Management appears highly experienced, with the CEO serving as Division VP and General Manager of Immunology at Abbott during HUMIRA launch and Director of CELEBREX launch (and arthritis team leader) in other regions. Chief Medical Officer Jeffrey Sherman served prior as Senior Vice President of Research & Development and Chief Medical Offier at IDM Pharma (acquired by Takeda).

As for executive compensation, I’m pleasantly surprised to see stock award packages in the range I would expect ($2M to $15M) as these larger life sciences companies can often be known for their corporate largesse. On the con side, I think the cash portion of salary of CEO at over $1.1M is excessive.

Proxy Filing

Figure 5: Executive Compensation Table (Source:Proxy filing)

The important thing is to avoid companies where the management team is clearly in it for self-enrichment instead of creating value for shareholders, and looking at compensation is one of several indicators in that regard.

As for useful nuggets from the ROTY community, DSJ.2018 states the following:

A little math for Horizon Therapeutics: If the enterprise value is around $14 billion today, sales around $4 billion (I believe) with a huge profit margin, the stock is selling for less than 10x earnings. That makes zero sense, especially with the market for thyroid eye growth. Now, there’s a competitor, Viridian, and I am not sure what kind of threat they really pose but their drug appears to be far behind.

As for IP portection, Tepezza patents are set to expire between February 2023 and April 2039 (also has biologic exclusivity covering the drug in the US until 2032). Krystexxa patents are set to expire by 2030 (excluding any additional coverage obtained). Upliza patents are set to expire between 2026 and 2032. So, I will concede here that I wish intellectual property portfolio had longer duration (ie. to the late 2030s).

Final Thoughts

To conclude, I think Horizon Therapeutics is an attractive cornerstone position for investors looking for attractive commercial-stage ideas in the biotech space. The company has multiple long term growth drivers and management has a track record of executing savvy business acquisitions at reasonable prices. Acquiring River Vision in 2017 for $145M upfront was a stroke of genius considering the drug could generate $3 billion+ in peak sales and did initial full year sales of over $800 million. Conversely, near term pain could continue if anticipated challenges with reinvigorating Tepezza sales further stall in the back half of 2022.

For readers who are interested in the story and have done their due diligence, HZNP is a Buy and I suggest accumulating a pilot position in the near term. A logical plan could be to await quarterly reports in Q3 and Q4 to incrementally add further exposure as rebound in sales is confirmed and to potentially get a lower cost average.

Risks include financings at disadvantageous terms and competition in certain diseases such as TED (think Viridian Therapeutics with recent data for VRDN-001 which showed better than expected efficacy and safety profile, but remains several years behind in development. There’s also the potential that management overpays in future acquisitions or amasses assets that fail to pay off with sufficiently positive clinical data or failed launch. As noted prior, IP portfolio has some key expirations later this decade and early 2030s (earlier than I would like). Also, from data sets generated so far I am unable to gauge probability of success for earlier stage assets in the pipeline.

While as an investor I leave price targets to the analysts, I do look at a blend of technicals, enterprise value, upcoming catalysts and future prospects to provide a realistic guess of potential upside in the medium term. If Tepezza sales are reinvigorated, I could see share price returning to the midpoint between here and previous highs at the $90 level. That would put them around the $20 billion market capitalization range, which seems reasonable for a deep pipeline and portfolio of 3 lead drugs set to do up to $5 billion in peak sales.

For our purposes in the Core Biotech portfolio, I will keep tabs on this one in my watch list for possible entry in the back half of the year (should valuation get even cheaper OR we see sufficient strengthening of the story). Due to IP situation and possibility of management failing to meet sales guidance for Tepezza in the near term, I am still not fully convinced on establishing a position here in the Core Biotech portfolio. Again, I will keep an open mind with an eye on management execution in both the clinic and commercially in the Q3 report.

Author’s Note: I greatly appreciate you taking the time to read my work and hope you found it useful. I look forward to your thoughts in the Comments section below. Lastly, be aware that most of my articles appear first to members of the ROTY community.

Be the first to comment