AsiaVision

Investment thesis

I recommend going long Hims & Hers Health (NYSE:HIMS). There are several positive things going on for HIMS: the large TAM, strong brand position and value proposition, business model, and growth momentum. I believe that as long as management does not mess up on execution, it should be able to continue capturing share in this space.

Business overview

HIMS provides a multi-specialty telehealth platform that puts patients in touch with doctors in various fields, including mental health, dermatology, primary care, and more.

US healthcare system is not efficient

In 2021, total healthcare expenditures in the United States hit $4.3 trillion and is projected to rise further. Despite this, it is unclear what the average consumer actually gains from these astronomical expenditures. In my opinion, all parties involved in the healthcare system, including patients, can benefit from a shift to a new model that prioritizes the patient experience.

The current healthcare system in the United States does not address the needs for the average patient despite the country’s massive spending on healthcare. It is plain to see that the United States is lagging behind other developed countries in terms of life expectancy and health indicators. Despite vastly more money being spent on healthcare overall, the United States ranked lower in several common health metrics among developed countries.

There is a severe lack of coordination and efficiency in the current healthcare system, as well as a lack of information and a hostile attitude toward the patient. Too many people in the United States go without the care they need and deserve because of problems with insurance or other financial obstacles. When patients can’t get the care they need when they need it, health outcomes suffer under the current system.

Telehealth is an essential piece of the puzzle

The demand for and supply of telehealth services are both on the rise, propelled by liberalizing regulations and structural changes in society. Telehealth allows for the better distribution of underutilized clinical resources. Considering the growing healthcare needs of an aging population and the widespread familiarity of the younger generation with digital devices, telehealth is a cost-effective method of making the most of scarce healthcare resources. It seems to me that the telehealth industry is primed for rapid expansion in the years to come. Younger generations have made it clear that they want access to telehealth services by saying they prefer to look for advice online than go to a doctor in person. When you consider that today’s youth are the healthcare consumers of tomorrow you can see why this is such a promising sign for the field’s future.

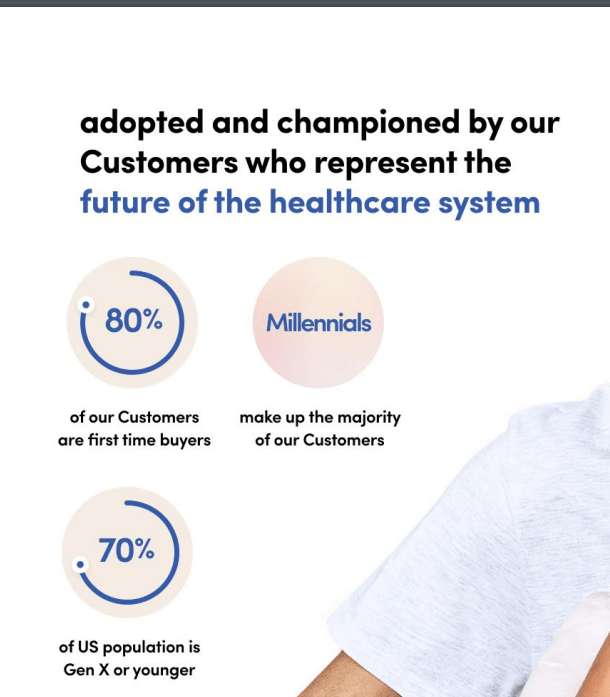

Strong brand recognition with next-gen of patients

Customers from the millennial generation, who are seen as the healthcare system’s future, have embraced and become advocates for HIMS products. The HIMS app and website are so user-friendly that they have broken down barriers of both accessibility and stigma. Evidence of this is found in the fact that roughly 80% of HIMS users report seeking medical help for their illness for the very first time. These are the kind of customers who will likely remain loyal to HIMS over time, becoming advocates for the company and helping to propel significant organic growth by expanding the HIMS community.

DESPAC DECK

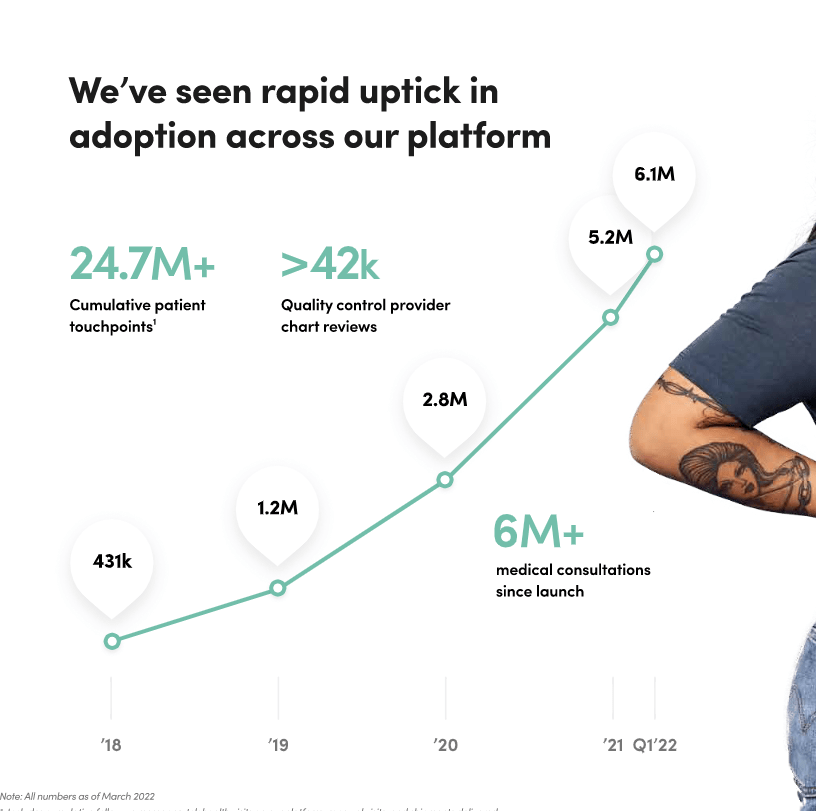

The astounding growth of HIMS since its 2017 launch (provided more than 6 million cumulative telehealth consultations since then), when it began powering telehealth consultations, is another indication of the system’s success. My opinion is that HIMS’ experience in cultivating direct connections with millennials, who will be responsible for the lion’s share of future healthcare spending, is a crucial strategic asset, given that a large percentage of the US population is of Generation X or younger.

3Q22 earnings

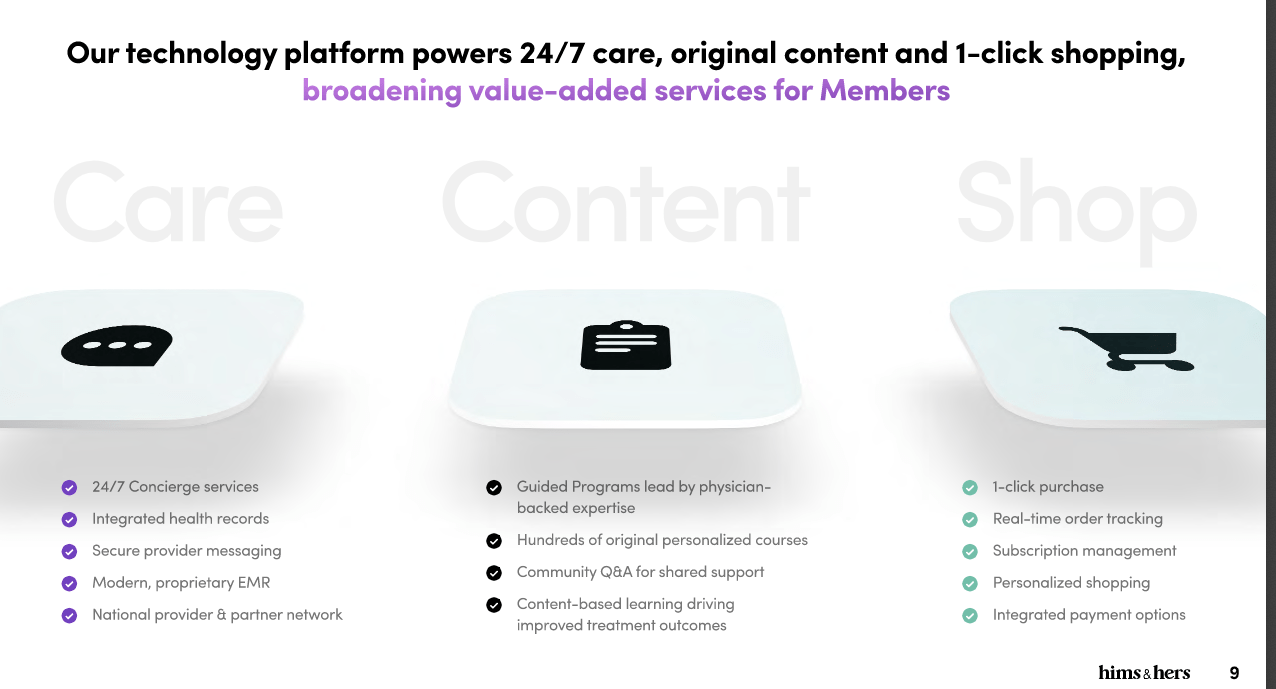

Proprietary technology and scalability

With the help of proprietary algorithms and an integrated technology stack, the HIMS platform provides a streamlined experience for both patients and medical professionals. In this way, HIMS can provide its customers with streamlined service and perform accurate, automated follow-up. In my opinion, this is a major competitive advantage for HIMS, as the hundreds and thousands of daily consultations conducted generate a virtuous data cycle that sheds light on the specific healthcare requirements of HIMS’s patients. As a result, HIMS is in a stronger position to roll out in-demand products and services that will better meet the needs of its customers as they develop.

3Q22 earnings

An additional advantageous feature of HIMS is its scalability. HIMS solutions are easily scalable and can be used to handle significantly larger volumes in a short amount of time. Plus, it’s a digital-native solution, so it can easily and rapidly incorporate new features and offerings. HIMS will have first mover advantage in comparison to rivals who are hampered by outdated back-end systems and consequently develop new products and services more slowly.

All of this should lead to a positive feedback loop that helps HIMS rise above the competition. With continued growth, HIMS is able to reinvest some of its earnings in research and development of brand-new products and enhancements to existing ones. As a result, it can increase its customer lifetime value while simultaneously reducing its customer acquisition costs. When examining HIMS’s financial results, it is easy to see that the strategy is successful.

3Q22 earnings

Attractive business model

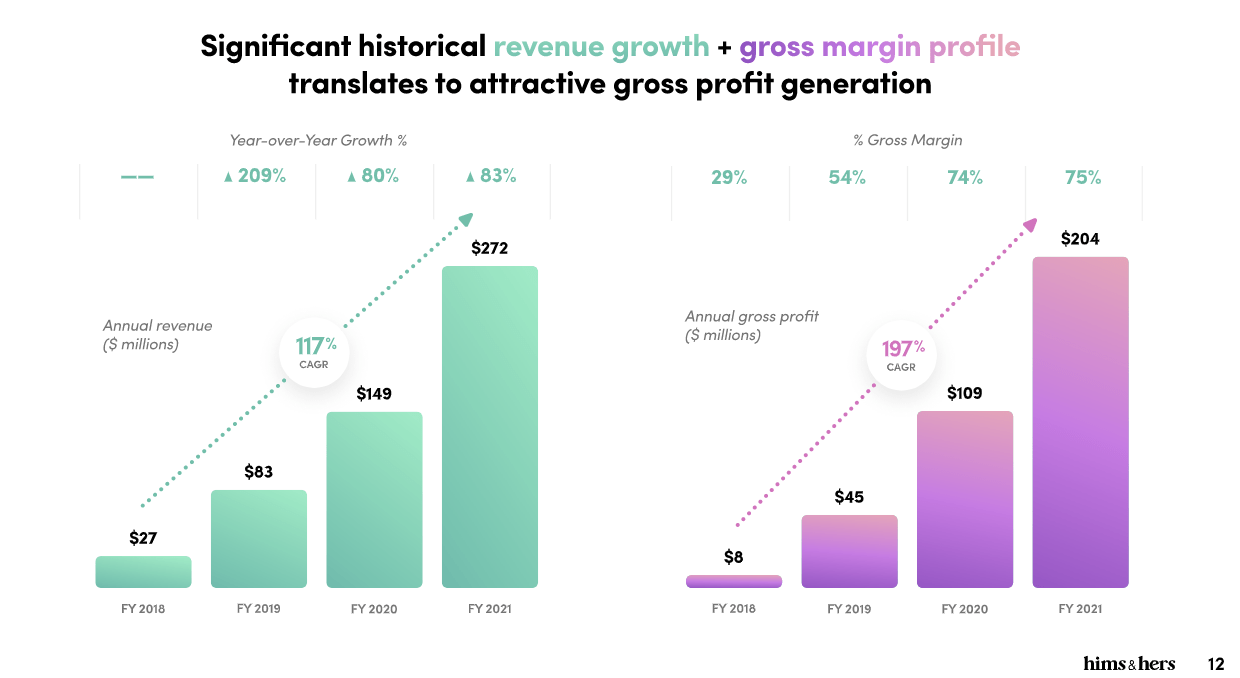

HIMS’s strong gross margins are the result of a compelling business model supported by recurring revenue. The majority of HIMS’s revenue comes from the sale of pharmaceuticals that are regularly prescribed. I think it’s smart of HIMS to zero in on conditions that require long-term drug use, as this provides more visibility into long-term growth.

HIMS also benefit from the shift toward multi-month subscriptions (launched in mid-2019), which increases customer loyalty and greater up-front revenue. While this may have resulted in fewer total orders in the short term, it should ultimately lead to higher AOVs in the long run. Considering the fact that the AOV has increased from below $50 to $83 as of 3Q22, it is safe to say that this strategy is successful. As such, even though HIMS’s current gross margins are in the 70s, I anticipate that they will grow even further in the future.

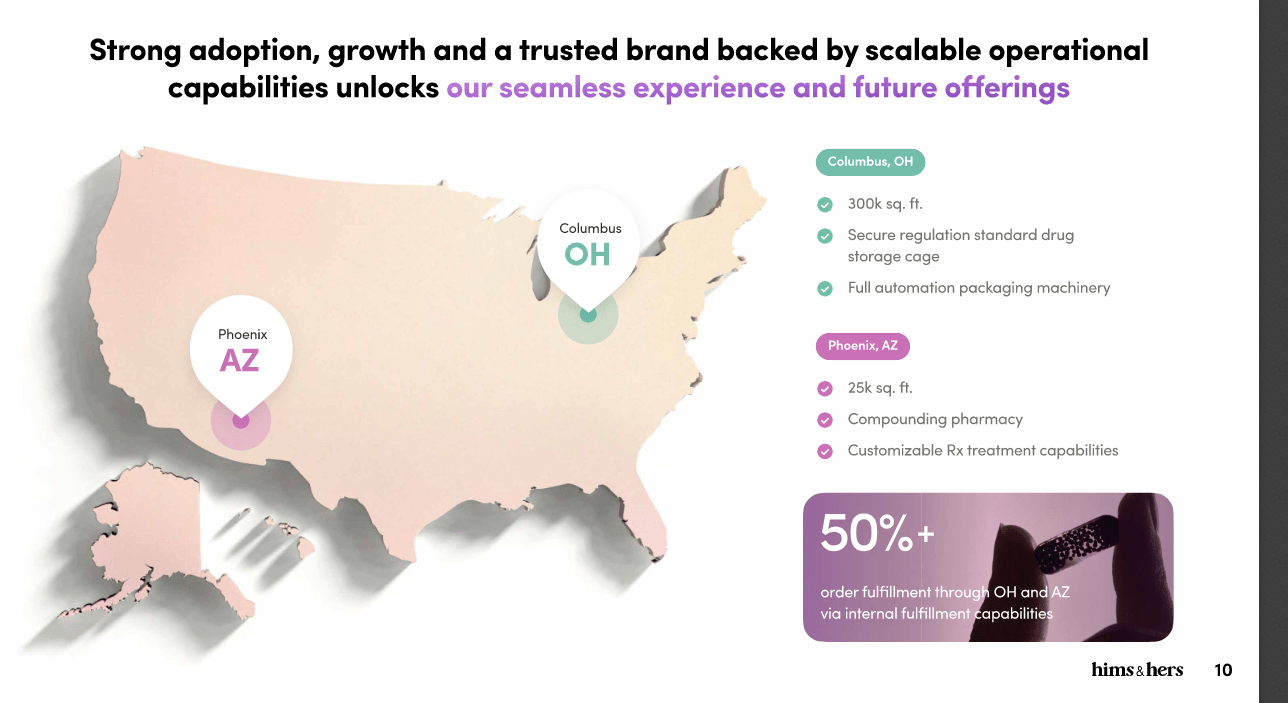

Meanwhile, the Ohio facility’s 300k square feet should allow for more streamlined drug distribution, resulting in increased operating leverage for the company.

3Q22 earnings

3Q22 continues to show momentum

Revenue of $144.8 million for the quarter was well above the $130.2 million expected by consensus, as strong growth in online sales more than made up for weakness in the wholesale channel. While rivals cut back on marketing, HIMS has persisted with its plan to increase its market share by investing a little more in expanding into new channels. Record-breaking quarterly net new subscription growth of 174k for HIMS can be attributed to the scale and significance of the company’s marketing efforts. With more time spent per order and a more varied product offering, the average order value jumped by 13% to $83. Increases in operational efficiencies, sales volume from affiliated pharmacies, and favorable revenue mix all contributed to a 200-basis-point increase in gross margin from the prior year.

Valuation

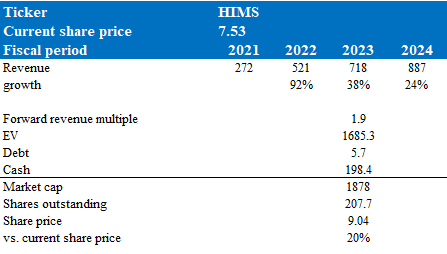

My model suggests HIMS is worth $9.04, if it trades at 1.9x forward revenue multiple in FY23.

Model walkthrough:

- Revenue to follow management full year guidance in FY23. Revenue growth should remain at a high level moving forward given the large TAM, HIMS brand position, and its business model which drives high recurring revenues. More importantly, the 3Q22 growth showed impressive momentum.

- HIMS used to trade at 4x forward revenue but I assumed valuation to continue trading at the current levels given the change in rates – which impacts valuation of high-growth-but-profitless companies like HIMS.

Own calculations

Risk

Low barriers to entry

HIMS faces stiff competition from a wide range of established healthcare providers and emerging telehealth alternatives. It’s important to note that HIMS isn’t the only telemedicine platform out there that focuses on the same health problems. These alternative channels also use cutting-edge promotional strategies to attract their target demographic of young adults.

Conclusion

HIMS offers a telehealth platform that connects patients with doctors across various specialties, including mental health, dermatology, primary care, and more. The current US healthcare system is not efficient, and telehealth is seen as a solution to improve it. There is a growing demand for telehealth services, and younger generations are showing a preference for it. HIMS has a strong brand recognition among the millennial generation, who are considered the future of healthcare. The company has had impressive growth since its launch in 2017, and its 3Q22 earnings are a positive indication of its success.

Be the first to comment