onurdongel

Investment Thesis: Hilton Worldwide Holdings could continue to see growth in overall RevPAR with the reopening of the Chinese market and anticipated growth in hotel bookings.

In a previous article back in November, I made the argument that Hilton Worldwide Holdings (NYSE:HLT) has seen strong RevPAR growth, along with net debt to EBITDA having fallen back to 2019 levels and an attractive P/E ratio – factors that I cited as being behind my decision to go long the stock.

While the stock has been seeing steady gains – price still remains below the $160-170 range seen at the beginning of 2022:

investing.com

The purpose of this article is to assess whether my reasons for being bullish on the stock still hold, and whether we could expect further upside from here.

Performance

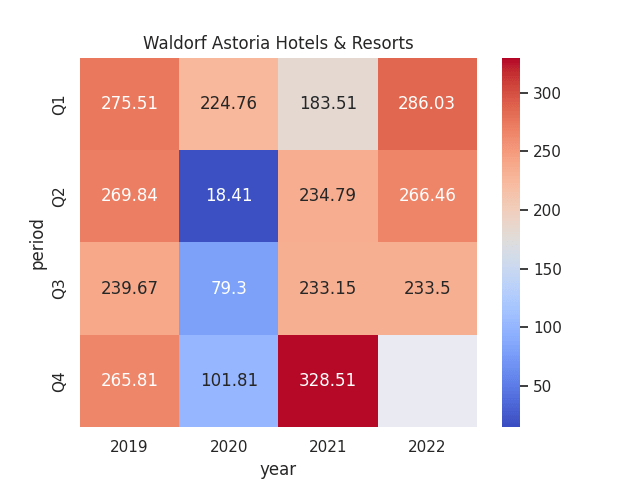

I had previously stated that should we continue to see RevPAR across high-priced brands such as the Waldorf Astoria continue to increase – then this could be a catalyst for upside as it would signal that demand is continuing to grow in spite of inflationary pressures.

With that being said, we can see that RevPAR would Q3 2022 was at the same level as Q3 2021.

Figures sourced from previous Hilton Worldwide Holdings Quarterly Reports. Heatmap generated by author using Python’s seaborn library.

Additionally, it is also notable that the ADR (or average daily rate) for the Waldorf Astoria was $500.93 for Q3 2021, while it had fallen to $422.47 for Q3 2022.

Given that RevPAR has remained the same as that of the same period last year – this may be an indication that RevPAR growth could not be sustained at the ADR level seen last year – and prices may have needed to decrease to keep RevPAR at current levels.

While I had previously argued that Hilton could have significant scope to continue bolstering revenue across higher-priced hotels outside peak season and would have the capacity to raise prices in spite of inflationary pressures – the latest data may indicate that this is not necessarily the case.

Moreover, we can see that Q4 2021 showed strong RevPAR performance for the Waldorf Astoria at $328.51. However, growth has largely moderated since then. Should we see RevPAR for Q4 2022 come in lower than last year, then this may give investors pause as to the degree to which Hilton Worldwide Holdings can continue to grow RevPAR. This concern could also apply to mid-priced brands, where customers are likely to be more price-sensitive.

The risk of a downturn in economic growth and subsequent pressure on RevPAR growth was a reason cited by Jeffries for its downgrade of Hilton as well as competitor Marriott (MAR).

Looking Forward

In my view, Q4 will be a significant telling point as to whether RevPAR can continue to see growth in spite of fears that the recovery for hotel bookings has peaked in the face of inflation.

With that being said, even if we should see revenue growth peak across the U.S. and Europe – the lifting of COVID restrictions across China could provide a sizable RevPAR boost across the Asia Pacific region as a whole.

When looking at Q3 2022 performance by brand once again, it is noteworthy that the Asia Pacific region comprised 14% of the total room portfolio for the Waldorf Astoria:

Hilton Worldwide Holdings Q3 2022 Earnings Results

For Hilton Hotels and Resorts, the Asia Pacific comprised over 20% of the total room portfolio for this period:

Hilton Worldwide Holdings Q3 2022 Earnings Results

For the Asia Pacific region, overall RevPAR in Q3 2019 was $90.92 whereas it was $66.46 for Q3 2022. In this regard, I take the view that revenue growth for this region still has significant room to rebound, and the reopening of China after a zero-COVID policy could significantly boost RevPAR performance across Asia Pacific as a whole going forward. China remains Hilton’s largest market in the Asia Pacific, and the 400 new hotels opened in the Asia Pacific in 2021 have been in China.

Conclusion

To conclude, Hilton Worldwide Holdings has seen a significant post-COVID recovery. However, concerns are mounting that such a recovery may have run its course and that revenue growth could plateau from here.

In spite of the macroeconomic risks, I take the view that overall RevPAR growth still has room to run given growth potential across the Asia Pacific with the “reopening” of the Chinese market. In this regard, I continue to take a bullish view on Hilton Worldwide Holdings.

Be the first to comment