sergeyryzhov/iStock via Getty Images

Published on the Value Lab 3/9/22

Putting things together on markets is how you come up with good angles. We think we have one with Hillenbrand (NYSE:HI). Private markets are more likely to rebound in terms of capital markets activity than public markets. Hillenbrand’s death care business is going to sell very easily. Getting love historically from Private Equity for one reason only, it prints cash, will reward HI shareholders. If it sells at a multiple like 15x EV/EBITDA, which is entirely plausible, that implies a pretty low valuation on the industrial businesses – lower than what plastic businesses on the heavily shorted and fundamentally beleaguered Hong Kong markets get. Seems unreasonable, so HI is a buy.

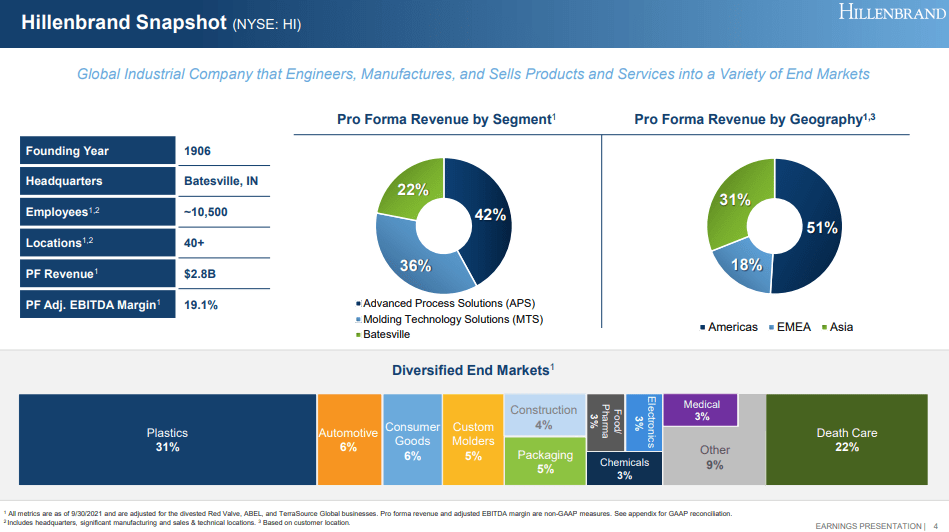

HI in Broad Strokes

Hillenbrand provides the equipment used in extrusion and injection molding to make all sorts of plastic parts, pipes, etc. as well as other equipment for industry. Clearly, their exposures are industrial. The following are their end-markets.

Breakdown (Q3 2022 Pres)

Backlogs are growing in the plastic molding businesses but also in APS, and China is surprisingly strong despite macroeconomic headwinds supporting MTS in particular, showing continued strength in the market for industrial capacity which HI provides.

Outside of the two industrial segments is Batesville, which provides caskets and other funeral services products to major funeral services customers. They are managing this business for cash and looking for potential strategic options with it.

Batesville had slight volume hits that affected scale, while the plastic equipment businesses managed to pair higher volume despite pressure brought on by lengthening lead times with pricing to achieve overall growth. Revenue and EBITDA both grew by about 5%.

Aftermarket sales also helped the APS business, both to preserve margins and create revenue on a growing installed base. But cost pressure did bring EBITDA down by 3%. The winning segment this quarter was the MTS segment, which benefited from more hot-runner equipment in the mix as well as higher volumes and price. This segment tends to be higher margin and benefits from the need to build out capacity to produce plastics. Indeed, this is the segment that dominates the plastic end-markets exposure, while APS covers in revenue most of the others besides death care. MTS great 11% in revenue and 11% in EBITDA. What’s great is that mix effects would have been even better in MTS if it wasn’t for China lockdowns. It is still a strong market, but absent those hot-runner equipment would feature even more highly.

Conclusions

Let’s hope straight into valuation. A funeral business like Hillenbrand’s easily gets the standard 15x LBO opportunity multiple. You’d see this as a rule-of-thumb multiple in any PE or M&A textbook, and it would come up in a target multiple analysis based on DCF logic as well. Even looking at peers and applying a control premium gets you to 15x. The margins are great at a little under 20% for EBITDA and the demographics improve for the business with America working through a bulge of people coming into dependency age. People die, so it’s a safe bet.

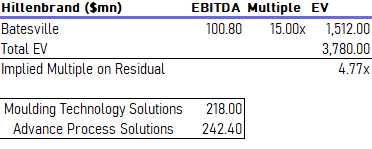

Supposing that multiple, look how the valuation turns.

Valuation based on annualised Q3 figures (VTS)

A 4.7x EV/EBITDA is implied for the industrial businesses, and a 5.4x if you use Service Corporation International’s (SCI) 12x multiple, which is the 15x without the control premium. Is this fair? Not on a relative basis.

Looking at Haitian (OTC:HAIIF) which also sells plastics injection equipment, the better grower of HI’s segments, it trades at a much higher multiple, at 7.6x actually. This is strange considering the heavy short going on Hong Kong markets, and also a greater exposure to China, which while a strong segment now is a little more uncertain from a macro point of view. In any case, even assuming the same geographic profile, Haitian has a multiple more than 50% higher than HI’s.

On an absolute basis, it’s more unclear whether HI is a good buy. Plastics get recycled, and that pressures manufacturing of new plastic. Moreover, they are in the process of falling demand as the goods boom subsides. Indeed, this ramping up of capacity that is happening, benefiting HI for now, is coming with cooling demand and that could mean pain for the >30% plastic exposure, and already is in terms of pricing of their commodified products. Rising gas prices, crude oil and energy costs are no help to the industry either. These are pretty high leverage cycles that HI is exposed to, so a downturn will matter. Still, the businesses look cheap at 4.7x, especially while they’re still doing well.

Maybe the timing could be better, but HI looks like value to me.

Be the first to comment