Mrinal Pal

Not to be confused with the parent company HP (HPQ), which now trades under the ticker symbol HPQ, Hewlett Packard Enterprise (NYSE:HPE) is a component of a 2015 enterprise split-off plan in an attempt to increase organizational efficiency and improve branding. However, we think HPE’s split-off is proving relatively unsuccessful as the business hosts disappointing operating metrics.

Although we don’t see this asset as a hard sell, we believe it could underperform the broader stock market in the foreseeable future; here’s why.

Operational Update & Key Metrics

Qualitative

Even though this is primarily a bearish article, I’d like to start off by pointing out a few positives to juxtapose our negative outlook. Hewlett Packard Enterprise recently beat its fourth-quarter earnings estimates with a revenue surge of 7.03% year-over-year. HPE’s Q4 revenue settled at $7.87 billion, with the firm’s intelligence edge division adding $965 million at 18% year-over-year growth. Furthermore, Hewlett Packard Enterprise’s computer revenue (its largest division) climbed by 16% in the past year. Even though the firm experienced growth across most of its business units, its computing and artificial intelligence slumped by 14% year-over-year.

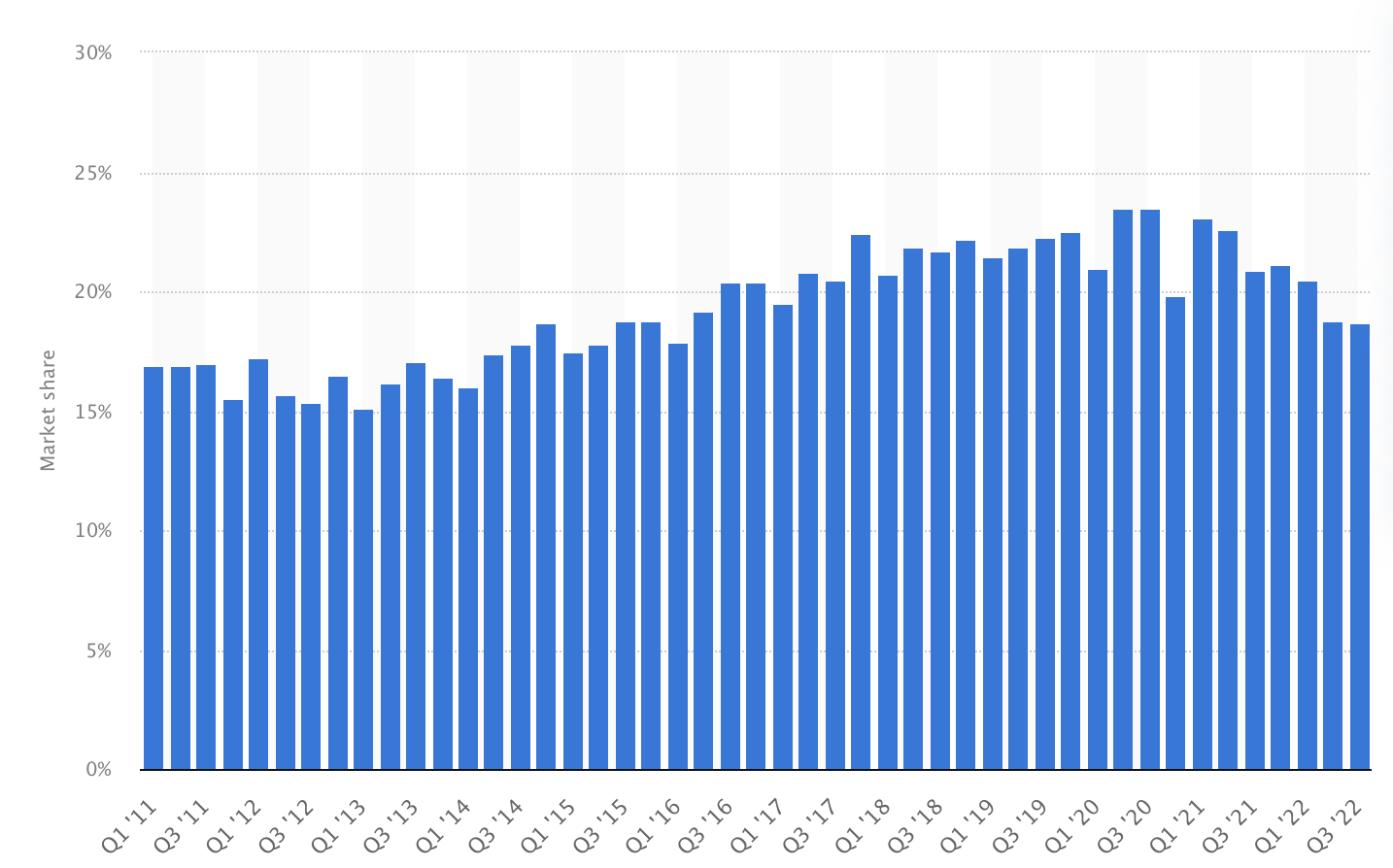

We do not think computer sales will proliferate throughout 2023 on the premise that corporate consumers might be skeptical of upgrading their hardware during a period of economic uncertainty and peak inflation. Most individual consumers will probably wait for more economic clarity before spending their disposable income, whereas corporates might hang fire until their earnings enter another growth phase.

HP Computer Market Share (Statista)

Furthermore, we found it confusing that HPE’s intelligent edge and AI segments experienced uncorrelated sales growth during Q4 because AI and data analytics are systemically cointegrated. Nevertheless, we believe both segments will grow once the economy stabilizes, as low-latency systems and AI integration is pivotal for modern business decisions. In addition, the world’s industrializing in a manner that emphasizes job growth among “tech-savvy” employees.

Collectively, we think the company’s personal computing sales might stagnate for the foreseeable future, and although it provides innovative solutions with AI and edge computing, its revenues are inconsistent, which could remain the case as competition heats up in the industry.

Quantitative

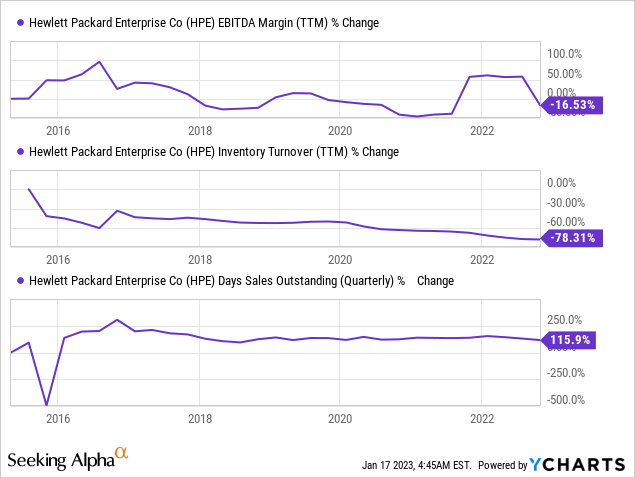

A quantitative overview of the company paints a grim picture. Hewlett Packard Enterprise’s EBITDA margin is shrinking at a constant rate, indicating diminishing shareholder value.

Conventionally speaking, the EBITDA line item speaks volumes when analyzing technology companies’ profitability as it backs out inconsistent amortization and often irrelevant depreciation. Moreover, tech companies often exhibit fluctuating capital structures, which provides an EBITDA observation with even more substance.

Furthermore, HPE’s inventory turnover ratio has declined during most of the past decade, suggesting that its inventory build-up has exceeded sales growth in most years. On top of that, the company’s days sales outstanding metric has exacerbated, implying a drag on liquidity.

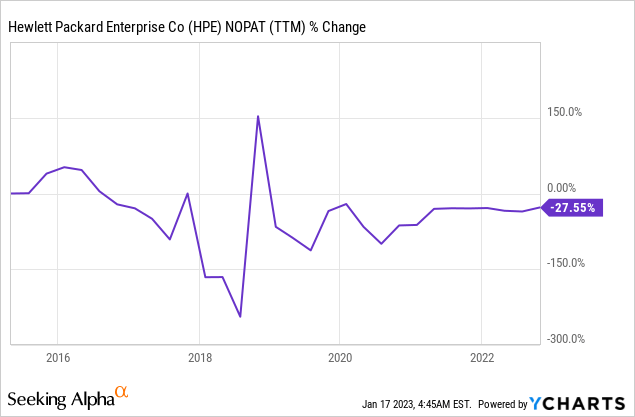

Another facet to worry about is HPE’s net operating profit after tax. The ratio’s shrinkage implies that working capital efficiency is lacking. This could be due to poor management or an organically receding income statement.

A Bit of Anecdote

The following observation is anecdotal and applies to HP as a whole instead of Hewlett Packard Enterprise alone. Nonetheless, it contextualizes the zeitgeist among HPE’s customers.

HP’s Hello Peter ratings are underwhelming, to say the least. Based on observation, customers complain about both hardware and software implications, which isn’t a good sign if you’re invested in either Hewlett Packard or Hewlett Packard Enterprise.

It’s often simple observations that provide a true indication of a company’s future performance, and Hewlett Packard’s poor customer retention could be the observation many market participants have been on the lookout for.

Product Reviews (Hello Peter)

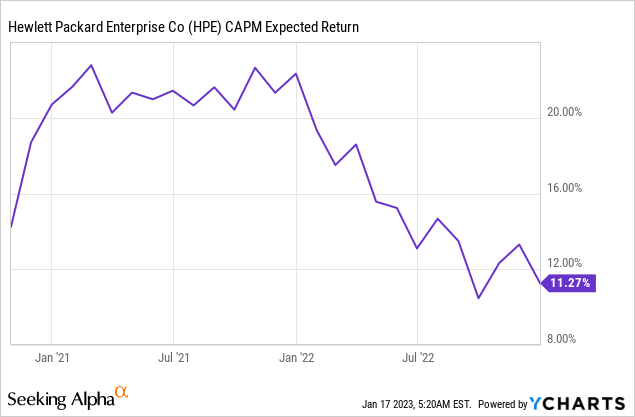

Expected Return

Valuation

Our multistage residual income valuation model suggests that HPE’s stock is slightly overvalued or fairly valued in a best-case scenario. Additionally, the stock remains in fair value territory under an expanded PE valuation formula, assuming an earnings-per-share target of 2.03 for year-end 2023 and a cyclical PE ratio of 8.81.

Author’s Calculations

Here are the input variables we used to create the multistage residual income valuation model.

- The stock’s current market price was divided by its price-to-book ratio to establish a beginning book value per share.

- Seeking Alpha’s database was used to derive expected EPS and dividend payouts. However, the terminal year’s values were assumed at normalized averages to account for cyclicality.

- A cost of equity percentage was used in line with CAPM, which was multiplied by the beginning book value to derive an absolute figure. On top of that, a persistence factor of 0.2 was phased into the terminal year to account for moderate earnings resilience.

Dividends

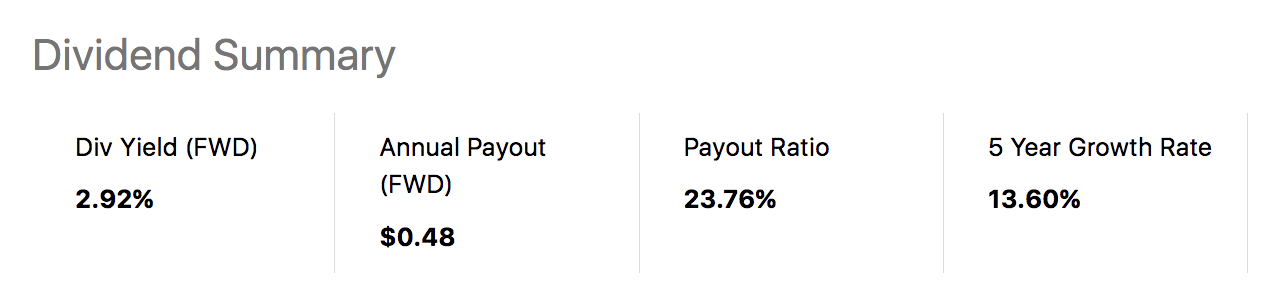

Despite the stock’s shaky valuation, it hosts a respectable dividend yield. We believe that the asset’s forward dividend yield of 2.92% is desirable, and its dividend coverage ratio of 4.17 could ensure consistency.

Seeking Alpha

Final Word

Despite Hewlett Packard Enterprise’s sizable market share in certain segments and its impressive fourth-quarter earnings, the company and its stock will likely provide underwhelming results in the coming years. Key metrics suggest waning operational efficiency and inconsistent revenue growth in innovative segments, which is worrisome. Additionally, our valuation models imply that the stock is fairly valued with limited scope from a price-based returns point of view.

Be the first to comment