imaginima

Overview

Hess Midstream LP (NYSE:HESM) is a little known pipeline spun out of Hess Oil (HES) in 2017. In the five years since the spin-off, HESM’s price appreciation has outperformed virtually every other pipeline company in the market.

HESM is closely related to HES via ownership of HESM units. In fact, Hess Midstream LP Chairman of the Board and CEO is none other than John Hess who is also CEO of Hess Oil.

A little-known fact is HES’s outperformance on both a price and total return basis compared to other pipeline stocks.

In this article, I will compare HESM to 5 other well-known pipeline companies Energy Transfer (ET), Enterprise Products Partners (EPD), Enbridge Inc. (ENB), Kinder Morgan Inc. (KMI), and MPLX LP (MPLX).

Note I use the terms “distributions” and “dividends” interchangeably.

Who is Hess Midstream?

HESM is a small pipeline/service company spun off from Hess in July of 2017.

Here is HESM’s description of their services:

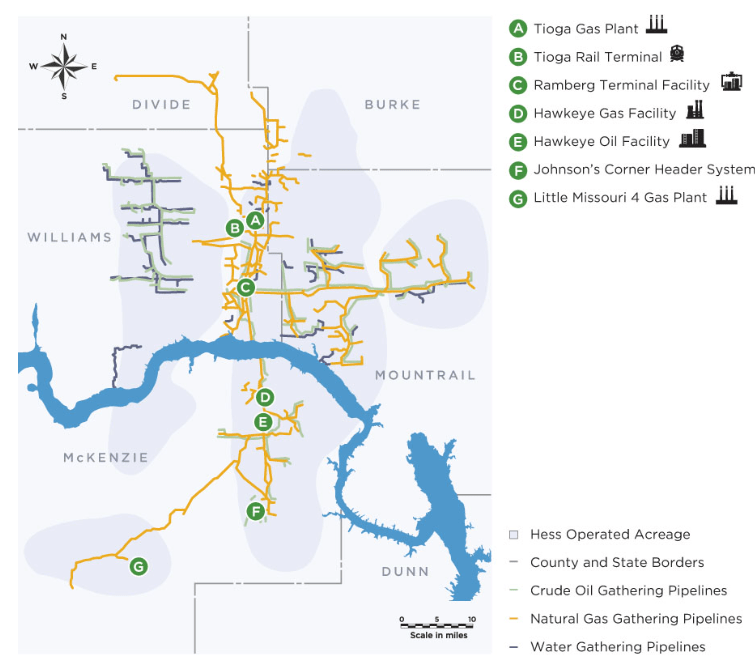

Hess Midstream provides a midstream value chain from the well pad, to the gathering system, to processing and storage, terminaling and export, which ultimately provides attractive access to the market. Our integrated systems in crude oil, natural gas and water services offer operational capability and export optionality to both Hess and third parties. Source: Hess Oil

HESM is mainly located in the Bakken area and mainly, although not exclusively, services Hess Oil production.

Hess Midstream

Financial Comparisons

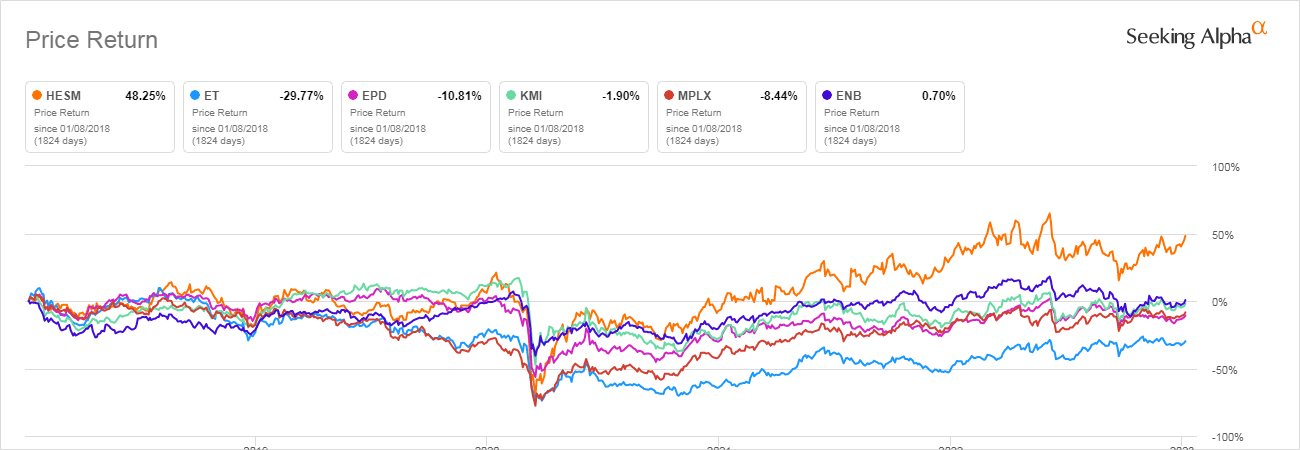

The first thing we will look at is the price performance over the last 5 years.

Seeking Alpha

HESM has vastly outperformed the other 5 pipeline companies with a price increase of almost 50%. For the other 5, only Enbridge actually has a positive return and it is less than 1%. All the others are negative with the worst one being ET down almost 30%.

If we add dividends to the price (Total Return) HESM outperforms even more with an increase of 117% over the 5 years.

Seeking Alpha

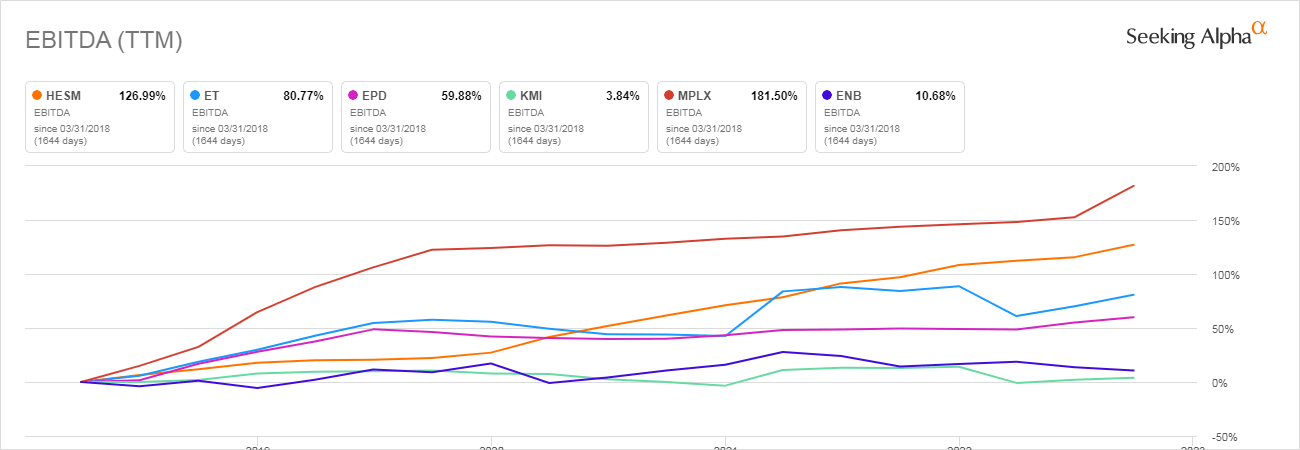

On an increased EBITDA basis, HESM also shines, outperformed only by MPLX.

Seeking Alpha

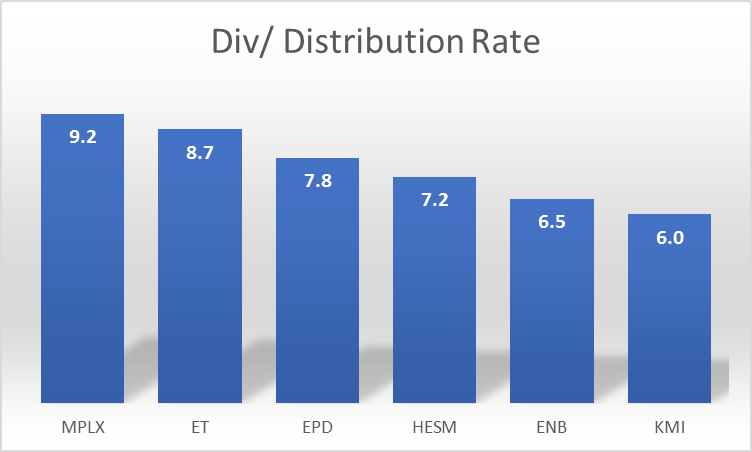

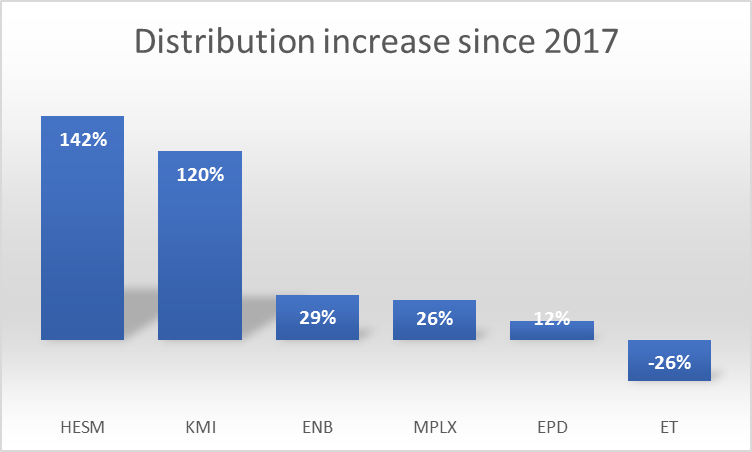

Hess Midstream also excels at distributions

If we look at the current rate of distributions, HESM falls in the middle of the pack with 7.2%.

Seeking Alpha and author

But digging further, if we look at the rate of increase since 2017, HESM once more jumps to the front of the pack with an increase of 142%. What this implies is that if HESM continues the rapid increase in distribution either the price will continue to rise or the distribution rate will trend higher. I think it will be the former.

Seeking Alpha and author

Risks and caveats

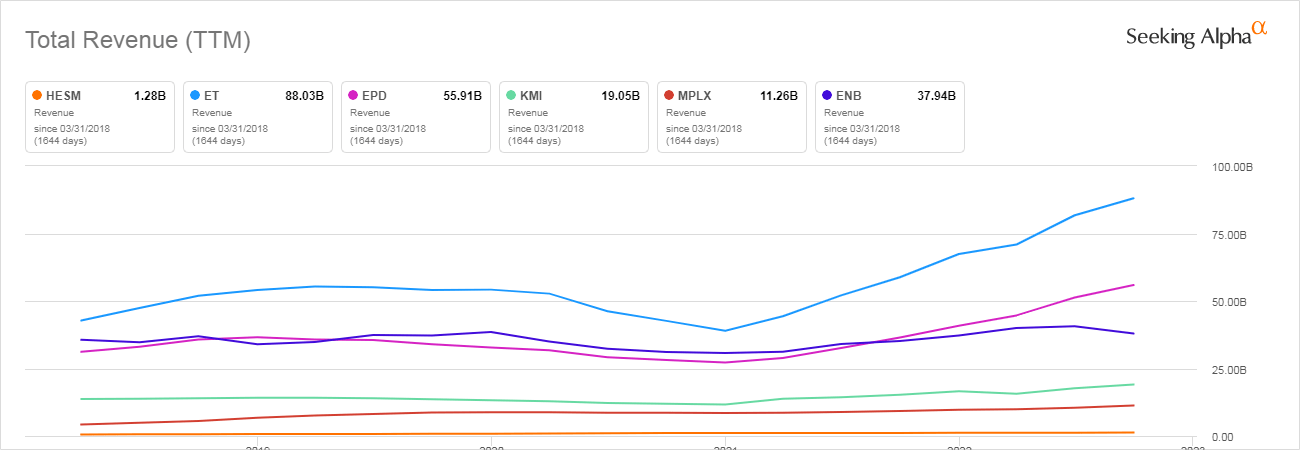

Obviously, one of the big issues with HESM is its small size relative to the others on this list.

Seeking Alpha

Note that the next smallest company on the list is MPLX with revenues almost 10 times HESM. The behemoths ET and EPD are really beyond reasonable comparison.

So if size matters to you, investment in HESM may be a concern.

Another concerning issue is HESM’s almost total dependence on Hess Oil for revenue. Having said that, Hess Oil is in an extremely strong financial position owning 30% of Exxon’s gigantic (10 billion barrels+) offshore Guyana assets. Would Hess Oil support HESM financially in difficult times? Nothing is for certain but it would seem likely.

These risks are outlined in Fitch’s credit report on HESM:

The outsized risks faced by a single basin-focused midstream service provider with high customer concentration are a concern for its ratings

– Source: Fitch

The other risks are the generic ones associated with all oil-related investments in a world of war, inflation, and a potential recession.

So please, do your own due diligence on every investment option including this one.

Conclusion

In the investment world, there are always opportunities lying in plain sight that we all overlook. I certainly overlooked Hess Midstream.

And although the risks are many, HESM’s brief history and substantial parental support make it look like a relatively safe investment assuming that oil-related markets in general do not disappoint.

So accordingly, I rate HESM a Buy for income-oriented investors but in limited proportion to other portfolio investments.

Be the first to comment