Land drillers have been in the dog house the last 4-5 years. Day rates were in the low teens and did not meet capital requirements to maintain the fleet. Since December of last year, the dynamic has shifted and the land drillers have rallied.

One we have followed for a few years, Nabors Industries, (NBR) has nearly doubled from the low $90’s to the mid-$160’s in share price since our last article on them in early January. If that seems high, remember they were the subject of 1:50 reverse split to avoid NYSE delisting several years ago. It’s hard to keep recommending a drilling stock in the $160’s as the downside is so severe. I am not suggesting NBR is over-valued in this market and at that price, but I am not adding to my position at these levels. That started me looking for another high class drilling outfit to examine.

H&P came to mind.

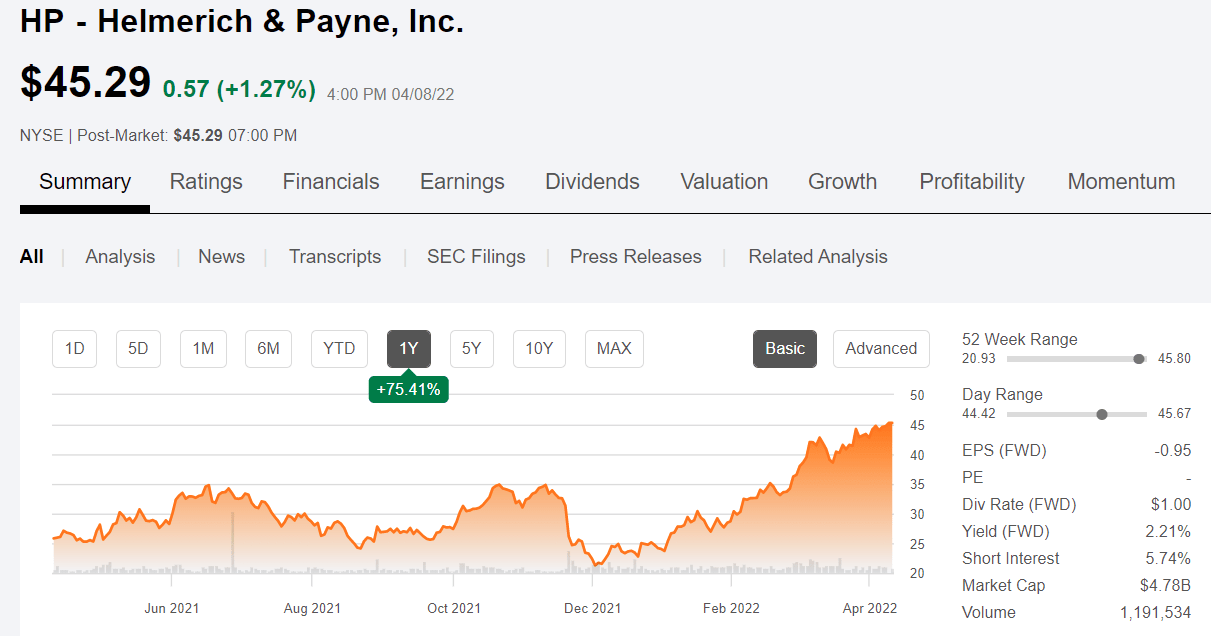

H&P Price Chart (Seeking Alpha)

Helmerich & Payne, Inc. (NYSE:HP) is a legendary driller whose roots go back to the 1920’s. The company has a comparatively clean balance sheet, and a fleet of easily convertible Flex rigs that can move about the location as dictates require. (Have a look at the HP video linked above.) By its own estimate, the company currently has a 26% market share in U.S. Land.

H&P is paying a modest dividend and has been buying back shares with cash flow to enhance shareholder returns. We think the company is perhaps getting a little ahead of itself and investors may want to sit on the sidelines for a while. Curiously, the shares have almost doubled since the end of last year, and only the strength of the pivot to drilling can account for that. We rate H&P a hold.

The thesis for H&P

The oilfield is a boom and bust business. It has always been this way, and nothing I’ve seen the last couple of really good years! changes this viewpoint one whit. We are currently in the beginning stage of a boom. Yay! What people lose sight of in the boom phase is the parabolic shape of these cycles if you track them. You hear people saying, “It’s different this time.”

The first time I heard that was in 1980 during a Saudi Arabia-led, sharp inflection higher in oil prices. The market was reeling from $40 oil prices and American drillers did what American drillers do. They drilled. That year, the rig count peaked around 4,500 before crashing over the next several years to ~800 or so. Fortunes were made and lost and will be again. It’s never truly different.

The fact we have some exacerbating circumstances now – supply chain, under-investment, a government that would prefer to ask sworn enemies of our country, like Iran, for more oil than make things simpler for domestic energy producers, climate-oriented delusions about green energy – only appears to modify the maxim I reference above: In the long run it’s never different. What goes up, will come down.

For now, we are going to pivot to drilling, and that’s good for drillers. I discussed this in my paid-service The Daily Drilling Report, a few months back. Here is some of that commentary.

Capital always seeks its highest return. That is an almost unquestioned maxim of economics. Shale production, with breakeven costs in the upper $20’s for big producers, has reached a point where output must rise, in part from the margins that today’s prices for WTI offer. It would be negligent on the part of oil company managers not to allocate more capex toward pumping more out of the ground in this scenario.

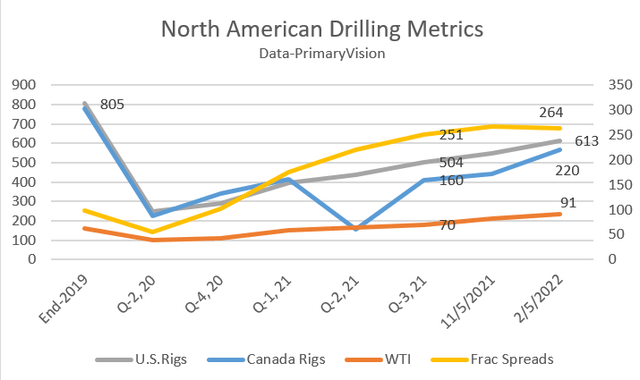

This is going to drive land drilling rig utilization, and rig margins substantially higher as operators look to ramp up their output. Let’s start with the all-encompassing number the EIA projects at about 800K BOEPD by next year, which would push U.S. production back toward the ~12.5 mm BOEPD seen in late 2019. The EIA Drilling Productivity Report-DPR from January 18th notes a rig-weighted average of ~1135 BOEPD of new oil per rig. Simple math suggests that if that target is reached it will require the support of ~700 additional rigs to obtain. (Note-let’s understand this calculation is way over simplified, but we have to start somewhere.) For reference, over the past two years we have added about 400 rigs, from the mid-2020 bottom of 253. (Gray line on chart below)

We’ve added about a 100 rigs so far this year and are bumping 700 active rigs. If you extrapolate that, we will add ~300 for the entire year. If oil prices remain supportive, by the end of 2023 we could be knocking on the 1,300 rigs level we’d need to meet the EIA forecast.

The pivot to drilling is on the rise as I began discussing last year. The DUC count is down around 4,000 and soon to maintain production – which everyone wants to do in this $100+ oil price environment, drilling is going to increase. Oil operators are adjusting their outlook for higher prices as the reality of oil at and above $100 sinks in.

The result is more rigs going to work. As of Friday, the count stands at 689 rigs, and 275 frac spreads are putting us on track to field about a 1,000 rigs at EOY. With its inventory of Flex rigs ready to go to work, H&P stands to benefit from this pivot at a greater rate than competitors, in line with the market share gains it has already seen this year.

H&P Global Fleet (H&P.com)

If you read the drilling company conference call reports, you soon learn that “Walking Super-spec” rigs are sold out. Idle inventory now consists of older rigs that have to be upgraded to the tune of $20 mm a pop to be walkers, so they sit bleaching in the sun.

Walking rigs have become the industry’s preferred model, but H&P has found clients willing to accept their version, the Flex Rig which are primarily “skidding rigs.” John Lindsay, President and CEO commented in the Q-1 call-

H&P remains the market leader within the industry, with the largest fleet of active rigs, as well as the most super spec rigs available to be deployed to satisfy future demand. Our strategy for new capital investment going forward will be tightly aligned with that of our customers and we’ll continue to be disciplined and return focused.

In addition to share count increases, the company expects the price is going higher, along with service bundling. John Lindsay, President and CEO, commented in the Q-1 call regarding their efforts to get pricing higher and build in additional profit centers to the daily rate:

Average rig pricing has improved only nominally up to this point. Our customers have benefited from higher commodity prices, but from an oil field service provider perspective and particularly as a driller, we need substantially higher pricing in order to generate the returns required to attract and retain investors Assuming oil prices remain strong, we plan to continue to push pricing in the coming quarters as the scarcity of readily available super spec rigs becomes more prevalent. We believe this upward rig pricing momentum should be commensurate with the value H&P delivers to the customer. Our rig pricing strategy is also dynamic, encompassing inputs derived from customer demand, pricing algorithms, reinvestment metrics and industry sentiment. As we look ahead to pricing in the strengthening and tight rig market, we see revenue per day needing to approach $30,000 or H&P to start generating margins that support cost of capital returns. And fortunately, several of our leading is rigs are beginning to approach this level of revenue today.

In summary, in an expanding market, H&P should continue to see growth as rig count moves higher. Profits should follow with higher daily rates and bundled services pushing the stock higher through the year if they are realized. As noted in the quote above, it hasn’t happened yet, although I think there is basis for it do so.

Analysts are a bit tepid on H&P with the consensus being a hold. The price range runs from $29 on the low side to $56 on the high side. These numbers seem a little out of date to me, and I’ll sprinkle some fairy dust around as we close out this article and see what our estimate might be.

Catalysts-AI assisted performance contracts

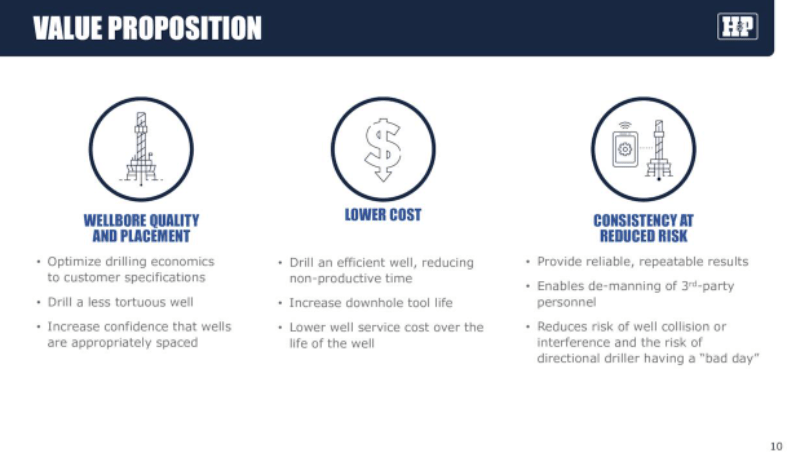

Operators are always looking for their providers to bring skill-sets and additional value to their projects. The challenge is always getting them to pay for it. AI is fairly mature now and provides operators with improved well construction-in siting, downhole directional drilling, pressure control, and other drilling parameters.

H&P Value Proposition (H&P.com)

It just makes sense that contract drillers have this technology, as they perform drilling tasks endlessly. John Lindsay, President and CEO, commented in the Q-1 call about how operators adopting their proprietary suite of AI drilling tools is changing the day rate model to a performance model that will bring enhanced profitability (emphasis added):

Our new promotion models are especially designed to include our automated software solutions that enable value creation through speed of execution and drilling times, and even more importantly by enhancing overall wellbore quality. As we’ve discussed on previous calls, the industry pricing model needs to evolve from a pure day rate to a commercial model that rewards performance, wellbore quality and value creation for the customer. We’ve grown our performance based contract model to approximately 40% of our active fleet and our teams continue to partner with our customers to drive better outcomes. We’ve taken a portfolio approach using different iterations of performance contracts to determine which types make sense for us and the customer under a variety of scenarios.

I think their penetration of the market with this approach is above par with their peers, and provides a platform for earnings improvement.

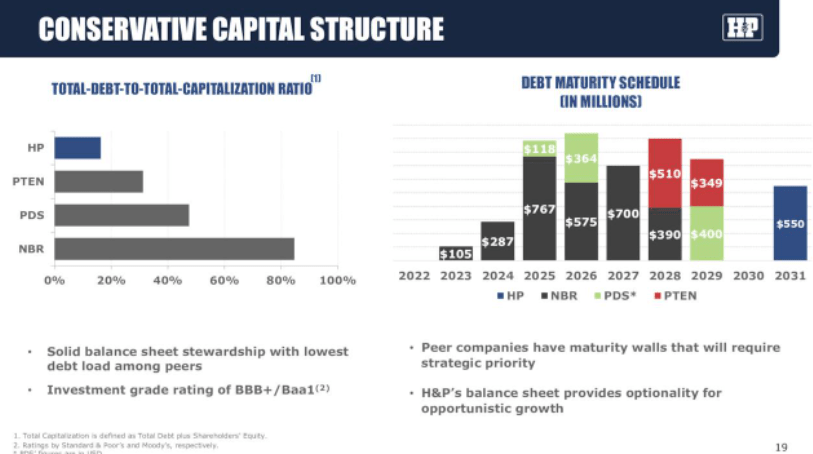

The company’s pristine balance sheet is also catalyst enabling them to fund JV’s similar to the ADNOC deal announced last fall, fund share buybacks, and raise dividends, when other companies are focused on paying down debt.

HP Capital structure (H&P.com)

Helmerich & Payne Q1 results

H&P achieved quarterly revenues of $410 million, versus $344 million in the previous quarter. As expected, the quarterly increase in revenue was due to higher rig count activity in North America Solutions as operators committed to calendar 2022 drilling activity. To summarize this quarter’s results, H&P incurred a loss of $0.48 per diluted share versus a loss of $0.74 the previous quarter.

Capital expenditures for the first quarter of fiscal ‘22 were $44 million below previous implied guidance. This was primarily due to the timing of spending, which has shifted to the remaining quarters. H&P consumed approximately $4 million in operating cash flow during the first quarter of 2022, generally in line with our expectations.

Let’s begin with the North America Solutions segment. H&P averaged 141 contracted rigs during the first quarter, up from an average of 124 rigs in fiscal Q4. They exited the first fiscal quarter with 154 contracted rigs, which was in line with guidance.

Demand for rigs continued to expand heading into calendar 2022 producer budgets. From October 1 through December 31 they added 27 rigs to the active rigs count, including two walking FlexRig Drilling rig conversions that were completed in fiscal Q1, and over 20 skidding rigs. Of note for rigs added in the U.S. market in calendar Q4 across the industry, H&P Skidding super spec rigs made up roughly 30% of all industry rig count additions account to the inverse rig count.

Their U.S. onshore market share increased in the first quarter and was approximately 26% at calendar year end ‘21 for total horizontal active rig count and 35% for super spec active rigs.

Looking ahead to the second quarter of fiscal ‘22 for North America Solutions, as I mentioned earlier they ended Q1 near the midpoint of previous guidance. As of today’s call, H&P has 164 rigs contracted and expects to end the second fiscal quarter of ‘22 between 165 and 175 contracted rigs. Their current revenue backlog from our North American Solutions fleet is roughly $493 million for rates on return contract.

Capital expenditures for the full fiscal year 2022 were still expected to range between $250 million to $270 million, with remaining spend distributed fairly evenly over the last three fiscal quarters.

H&P has cash and short-term investments of approximately $441 million at December 31, 2021 versus an equivalent $570 million at September 30, 2021 after backing out the 2025 bond extinguishment. The sequential decrease is largely attributable to their recent share repurchases, seasonal cash outlays and working capital lock up.

Through January 28, they have purchased approximately 3.1 million shares total for roughly $76 million. Approximately 2.5 million shares were repurchased in December under the evergreen annual share repurchase authorization of 4 million shares per calendar year. To-date in calendar ‘22, they repurchased about 600,000 shares under the calendar ’22, $4 million authorization. These recent repurchases augment the longstanding dividend as they allocate excess cash.

Including their revolving credit facility, liquidity was approximately $1.2 billion at December 31. The debt to capital at quarter end was approximately 16% and our net debt was approximately $101 million. They currently expect their trailing 12 months gross leverage turn to reach our goal of less than 2x outstanding debt during this fiscal year.

The company’s cash burn is troubling, as is the lack of operating cash flow. This is due to rising OPEX costs, now running about $15K per day, and the CapEx to put rigs back in the field. If the oil price were to decline substantially below $100 per barrel for any length of time, the shares could weaken considerably.

Your takeaway

Booking a loss for the quarter, so the usual EV/EBITDA and Cash flow metrics don’t apply. On price-per-sales basis, the company is trading at about 5X, and over time this should continue to improve.

The absolute key to this stock is their ability to get some additional margin onto their rigs in the field. I think the ingredients are there for this to happen, but until they demonstrate it, I would not touch the stock. At $45 per share, it is by no means in bargain territory, and that’s really the only place to buy drillers.

I would keep an eye on this one for a break below $30, a one-third-ish price drop from present levels. H&P has a lot of things going for it, but if they can’t get their margins up, it could turn into a barn fire.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment