Dean Mitchell/E+ via Getty Images

Healthpeak Properties (NYSE:PEAK) is a real estate investment trust (“REIT”) and S&P 500 (SPY) component that owns and operates healthcare properties across the U.S.

The company’s portfolio includes three core asset classes: Life Science; Medical Office (“MOB”); and Continuing Care Retirement Communities (“CCRC”). About 90% of their total adjusted net operating income (“NOI”) is attributable to Life Sciences and MOBs.

Similar to other healthcare-related REITs, PEAK has been and will continue to be a beneficiary of favorable long-term demand drivers, such as an aging senior population and growing global pharmaceutical drug sales, which benefits both their MOBs and Life Sciences buildings, respectively.

The company’s total overall portfolio is well diversified with over 200 tenants. Their top five include some of the largest companies in the industry, such as Amgen (AMGN), Johnson & Johnson (JNJ), and Pfizer (PFE), to name a few.

Complementing their portfolio is a strong balance sheet that is comprised of significant available liquidity and limited near-term debt maturities. Their positioning is also investment-grade rated from all three of the major reporting agencies.

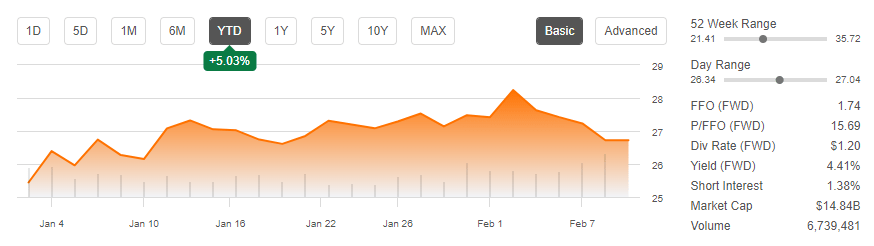

YTD, shares are up about 5%. And though they are still down about 20% over the past year, the losses are lower relative to others in the sector.

Seeking Alpha – Basic Trading Data Of PEAK

For investors, the stock offers modest upside potential of about 15% and a reoccurring dividend payout that is currently yielding about 4.4%. While this may be sufficient for some, others may need more than that to compensate for the losses incurred in 2022.

Q4FY22 Earnings Recap

PEAK’s portfolio remained fully occupied at year end, with an overall occupancy rate of 99%. And in their new developments, they were at a pre-leased rate of 78%.

Within individual segments, their Life Sciences unit, which represents over 50% of their total NOI, ended the year with an occupancy rate of 98.9%. Their MOBs, on the other hand, which together with Life Sciences represents about 90% of total NOI, turned in a year end rate of 90.2%.

Q4FY22 Investor Supplement – Overall Portfolio Metrics

In the same-store portfolio, occupancy in Life Sciences was up 180 basis points (“bps”) YOY, though down 40bps on a sequential basis.

Q4FY22 Investor Supplement – Same-Store Portfolio Metrics

The unit’s high occupancy levels came on 1.4M SF of leases executed during the year, 68% of which were attributable to new signings. In addition, 79% of the total volume was to existing tenants. And on renewals, the company fetched 35% cash re-leasing spreads. Furthermore, the portfolio still has a mark-to-market of 25%, providing additional runway for further growth.

In addition to occupancy gains, retention held at 82%. Limited near-term lease maturities further insulates them from tenant turnover risk. But at the same time, it is also a limiting factor for their organic growth potential.

Looking ahead to 2023, the limited maturities are in fact baked into projected results. In Life Sciences, for example, management expects same-store growth of 3% to 4.5%, driven almost entirely by rent escalators in the low 3% range.

And in Medical Offices, management sees growth ranging between 2% to 3%, which is in line with their historical average despite what is expected to be difficult YOY comparisons.

Liquidity and Debt Profile

At year end, the financial foundation remained on solid footing. And in the final months of the year, the company was active in the capital markets, raising over +$1.3B through two debt transactions, the settlement of their forward equity agreement, and property dispositions at a 5% cap rate.

This was made possible in part by their investment-grade rating with a stable outlook from all three major reporting agencies. The positive ratings facilitate access to the capital markets that would otherwise be locked for most other participants.

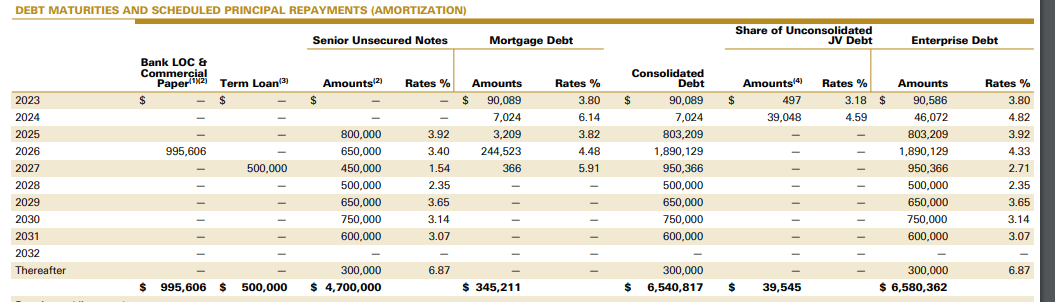

Altogether, PEAK currently has +$2.5B of available liquidity. This sizeable balance of unrestricted funds is paired with no significant debt maturities until 2025 and a fully funded development pipeline.

Q4FY22 Investor Supplement – Debt Maturity Schedule

And as a multiple of EBITDA, net debt stood at 5.3x at year end. This is comparable to targets, and it represents a manageable load for the company. In addition, their floating rate exposure is just 5% of their total stack. This minimizes risks pertaining to volatile interest rates.

PEAK is also well within compliance of all required covenants with ample cushion to take on additional capacity. Their fixed charge coverage ratio, for example, is 5.4x. This is significantly above their minimum requirement of 1.5x.

Dividend Safety

PEAK currently provides a quarterly payout of $0.30/share. This is unchanged from recent prior periods and is down about 19% from the $0.37/share payout provided in 2020.

Seeking Alpha – Recent Dividend Payout History

At the beginning of 2021, management cited the reduction as a necessary action in realigning their payout ratio with their targeted portfolio strategy, which resulted in annual savings of +$150M.

Presently, the payout yields about 4.4% at current trading levels, about 100bps below the yield that would have been obtained under their payout levels prior to 2021.

From a coverage standpoint, the payout ratio, as measured to reported funds from operations (“FFO”), was just shy of 70% for both the quarter and for the year. This is improved from the 75% payout at the end of 2021.

But on an adjusted FFO basis, which incorporates reoccurring capital expenditures, the payout ratio was about 83% for both the quarter and for the year. While this still represents full coverage, it is elevated relative to the sector average, which currently is about 75%.

Though investors don’t appear to be in danger of a cut, the likelihood of future hikes higher is limited, given current coverage levels.

Main Takeaways

Demand for PEAK’s properties clearly remains robust. Overall occupancy at year end stood at 99%, and it was 98.9% in their Life Sciences unit, their largest segment. The strength there was supplemented by their MOBs, which sported occupancy levels of 90% and boasted about 17M visits during 2022, according to management commentary.

Favorable long-term demand drivers, specifically an aging population, will remain supportive of current occupancy levels in both the medium and long term.

The strong occupancy rates translated to full year same-store NOI growth of 5.1% and 5% in Life Sciences and MOBs, respectively. These growth rates came despite challenging comps that included best-in-sector growth in 2020 and 2021 in both segments.

In addition, for the quarter, the company turned in results that exceeded their full year growth rates. This provided the company with solid momentum into 2023.

While the demand environment has slowed from levels experienced in 2011, the industry appears to be on solid footing. The NIH budget was recently increased by 6% and the Biotech sector remains well funded. And in 2022, through three reported quarters, R&D spending was over +$100B and was on pace to be the highest year ever. This will likely be confirmed when the final numbers are released.

The healthy funding environment and the favorable demand drivers set up PEAK positively for future growth. While organic opportunities for occupancy and rate growth appear limited due to near full rates and limited upcoming maturities, the company still has a sizeable development pipeline, which is fully funded, and nearly 80% pre-leased. This should provide accretive earnings growth as they are placed in service.

From a valuation standpoint, recent property dispositions commanded cap rates of 5%. This is about 100bps lower than the implied rate of the shares. At a 5% implied cap rate, shares would be fairly valued between $30-$32/share. That’s in the realm of 15% upside from current trading levels. This would be on top of a quarterly dividend that is currently yielding in the mid-4s.

While the upside remains, there could be greater opportunity elsewhere. Medical Properties Trust (MPW), for example, trades at less than 7x forward FFO and comes with a dividend yield of nearly 10%. This contrasts with PEAK’s forward multiple of 15.7x. While the outlook is positive, the upside may not provide enough justification for new initiation for investors seeking more significant gains.

Be the first to comment