seewhatmitchsee/iStock Editorial via Getty Images

Groupon (NASDAQ:GRPN)? Really? The restaurant discount company that peaked almost 10 years ago? That’s how I reacted the first time I saw Groupon suggested as a great 2023 opportunity, and I’d imagine you’re thinking the same thing.

But companies change, and while still focused on discount deals, Groupon the company and the stock are far different than what you likely remember.

The Company

If you are 30 or older, you are probably familiar with Groupon. It took the ecommerce world by storm, and there were Groupons for everything from restaurant takeout to massages. These coupons were premised on buying in bulk and bringing new customers to local businesses, and they were wildly successful. There were also unintended consequences with deals sometimes too cheap for restaurants to survive or volume that overwhelmed services and had them booked up for months in advance.

In 2011, Groupon realized that selling discounts to local merchants was not going to provide the long term growth it needed, so it launched Groupon Goods for discounted products. After lackluster results, the company fired its co-founder Andrew Mason in 2013 and hired a company insider Rich Williams in 2015. In 2016, it launched Groupon Stores, directly competing with Amazon by offering a centralized marketplace for independent merchants to sell their own discounted products. Neither was particularly successful, and Groupon Stores was shuttered by 2020. While Groupon continued to excel in its core competency – experiences – the pandemic crushed that market and sales plummeted. By the end of 2020, Rich Williams was out.

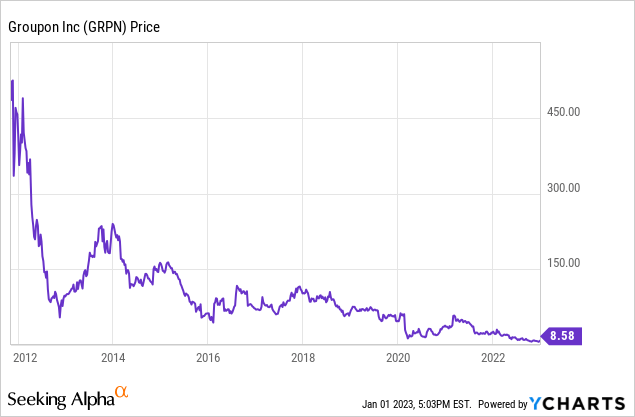

Stock History

Groupon went public in 2011 with a $700M IPO valuing the company at almost $13B and $20 per share. Trading opened at $28 but never hit that price again. Almost immediately, the original investors began to exit their positions, growth began to taper, and the stock price began a steady march downward. Within a year it was below $5 per share and culminated in a 1-for-20 reverse split in 2020 when it was dangerously close to delisting. The split brings the adjusted IPO price to $500 per share!

For anyone owning Groupon over the last decade, it’s been a disaster.

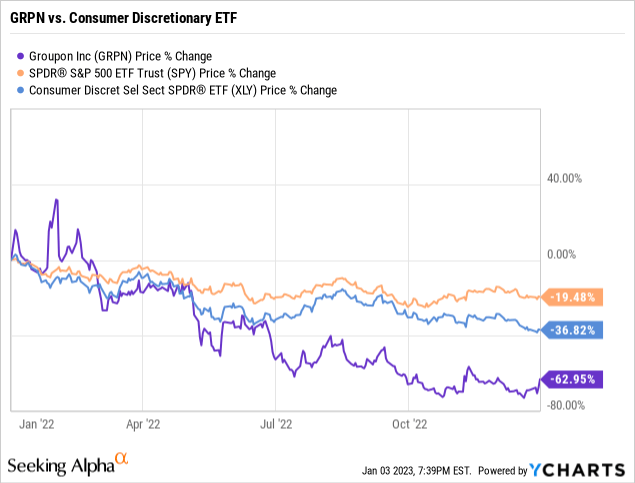

Stock Performance in 2022

More recently, the stock has been extremely volatile. While there has been a general selloff in almost all the names in the consumer discretionary sector, GRPN and other online retailers have been hit particularly hard. The S&P500 was down almost 20% in 2022, compared to 37% for the SPDR Consumer Discretionary ETF (XLY), but more than 60% for Groupon.

After a dramatic spike in January to $30 per share based on speculation about its stake in SumUp, GRPN has been on a steady downward trajectory. At the time, SumUp was exploring a financing round at a $20B valuation, and there was some uncertainty about Groupon’s ownership level.

New Management, New Focus

The last few years have also marked a change in strategy and approach both with respect to the core business and the stock. What was a failed growth story, has become an undervalued cash flow machine. Groupon owns a valuable online marketplace and with new management and investors, it is looking to monetize its digital real estate instead of constantly chasing growth. This transition is what now makes the company an attractive opportunity.

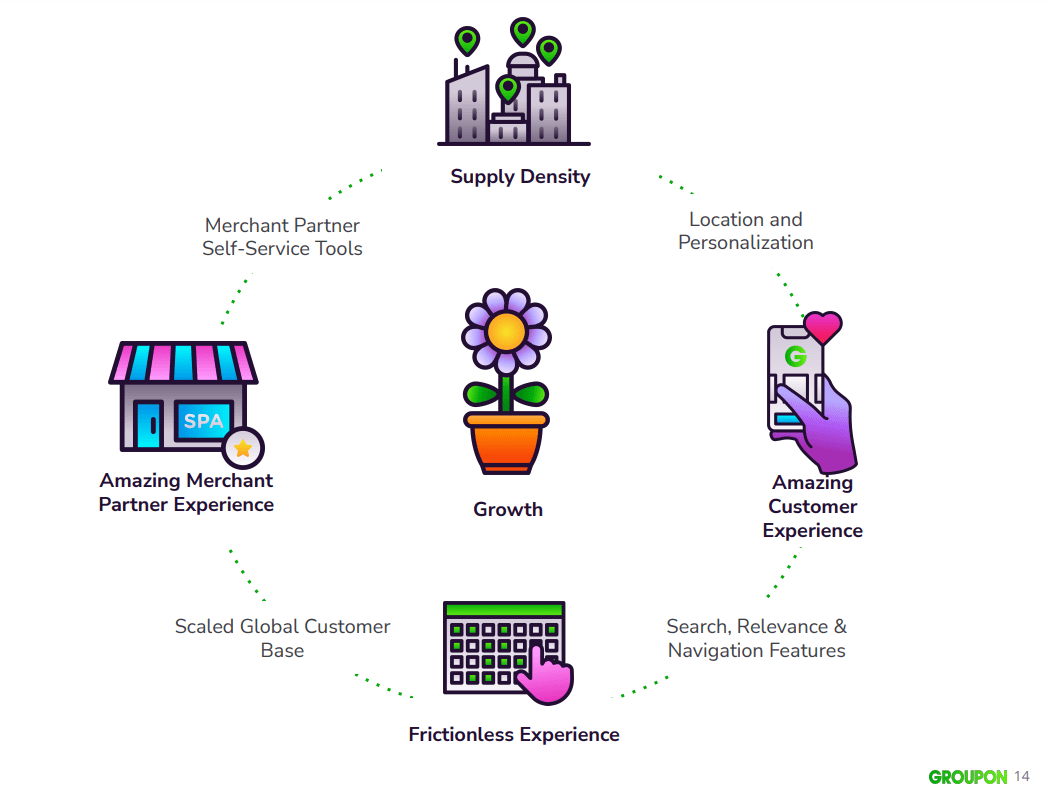

After Rich Williams left the company, the board began an exhaustive 21-month search for a replacement. In December 2021, they finally recruited Kedar Desphande, who had been leading Zappos as CEO. Kedar immediately set about prioritizing Groupon’s core competencies as seen in the below slide from the Q4 2021 earnings presentation.

Groupon Q4 2021 Earnings Presentation, Page 14

By the end of Q1, the company identified 3 core areas of focus to stabilize growth and drive cash flow:

- Reduce costs by automating process and merchant onboarding, i.e. layoffs of tech and sales staff.

- Fix the marketplace by focusing on inventory in successful markets via “increased density.”

- Focusing the goods platform on beauty and wellness where the company was already excelling and had carved out a niche.

While I am confident in management’s ability to deliver on #1 and #2, I have my doubts about the long term viability of its goods platform. However, my investment thesis isn’t dependent on a return to growth. The company simply needs to stop the bleeding to turn its share price around.

New Ownership

In addition to a new CEO, Groupon has also attracted an activist investor in Pale Fire Capital and its founders Jan Barta and Dusan Senkypl. Jan founded a domain name marketing company which would acquire generic domains and monetize the web traffic before building an online insurance and financial services platform with Dusan. More importantly, they have experience running discount deal platforms in eastern Europe. Specifically, Slevomat was built with Groupon as its model for success. Pale Fire Capital has shared Slevomat’s success with both discounted and full price offerings and encouraged Groupon to focus on experiences – restaurants, hotels, city tours, etc.

In addition, Pale Fire Capital has recruited Vojtěch Ryšánek as interim CTO from Aukro.cz. Aukro was a turnaround story in the Czech Republic that was broadly successful.

Jan only began disclosing his stake in Groupon in April, at which point he collectively owned 10% of the company with his firm and partners. They continued to accumulate shares with current holdings at 6.7 million. Most of those purchases were made at prices from $10 to $20 per share, so this represents approximately $100M in capital invested. Marked to market at today’s stock price, it’s a $57M position.

Sitting next to these kinds of committed investors dramatically increases the likelihood of success for this turnaround plan. Pale Fire has the experience and know-how to increase Groupon’s margins and drive positive cash flow, and they have the influence to change management if they aren’t delivering.

Valuation

Now that we know where the business is headed, let’s take a look at the valuation. At its core, the Groupon investment opportunity is built around a stock price that has fallen way too far. Whereas previous investors were buying a high-growth ecommerce story, new shareholders are looking for cash flow and efficiency.

Current enterprise value is approximately $340M using the September 30th balance sheet and stock price of $8.58 as of December 30th.

| Market cap | $260M |

| Cash | $308M |

| Debt | $388M |

| Enterprise Value | $340M |

There is also a 2.3% minority interest in SumUp, a UK based mobile payments company. SumUp last raised capital at €8B in June, a significant down round from their €20B valuation at the beginning of the year. That represents $184M in value, but we can further discount it to $150M due to lack of marketability of the securities. Even at that level, it’s approximately $5 per share of value to Groupon.

That gives us an adjusted enterprise value for Groupon of $190M. If you believe Kedar Deshpande and his team are going to achieve even half of his targets, this is a steal.

Groupon is targeting 2023 sales of $1.3B, or 60% of its 2019 billings, the most recent full year without a Covid impact. Additional targets include 15-20% EBITDA margins and $100M in free cash flow.

If Kedar can get Groupon to $200M in run-rate EBITDA and $100M in FCF, what is a fair value for the business? Due to my long term no-growth expectations for Groupon, I’m using conservative multiples of 5x EBITDA and 5x FCF. SeekingAlpha’s median multiples for Consumer Discretionary are 8x and 10x, respectively. Using 5x 2023 EBITDA or FCF, the business is worth $17 to $30 per share with an additional $5 per share from liquidating its holdings in SumUp.

| Multiple | Forward multiple | GRPN value | Implied value | Implied Share Price |

| EV / EBITDA | 5 | $195M | $975M Enterprise Value | $30 |

| Price / FCF | 5 | $100M | $500M equity value | $17 |

I recognize this is an extremely wide range, but the absolute values are not what’s important here. What I am focused on, and I would encourage you to pay attention to, is that even the conservative estimate is more than 2x the current share price. If you add in SumUp, Groupon should be trading at least $20 per share. As Buffett would say, we have a substantial margin of safety in the current company valuation.

As to how to position yourself, I am long both shares and April call options. The April contracts will let the company publish Q4 results and provide guidance for Q1 before expiry. I believe once it’s clear the company is generating cash flow in the 4th quarter and reaffirms its guidance for 2023, the stock will quickly bounce back up to the $15-20 range it was in for the first half of 2022. The stock has already moved up from its low at $6.30.

In my opinion, the biggest risk to this investment over the next 3 months is general market sentiment. If you are going to use options as I have, size your position conservatively, so as to preserve capital if market timing doesn’t work out.

Be the first to comment