mirsad sarajlic

Earlier this year, Griffon Corporation (NYSE:GFF), a holding company with a market cap of $1.6 billion, was hit with a proxy contest initiated by Voss Capital. It has been a catalyst for change and is well received by the market if we look at the one-year stock price increase of 27.34%. Furthermore, there has been a significantly large amount of insiders buying the stock over the last year.

One Year Stock Price Overview (SeekingAlpha.com)

Since my previous article in August 2022, the stock price has increased by 8.19%. At the end of November, GFF will release the Q4 financial results and announce strategic solutions to increase shareholder value. The activist shareholders are considering many options; merging or selling are two alternatives discussed.

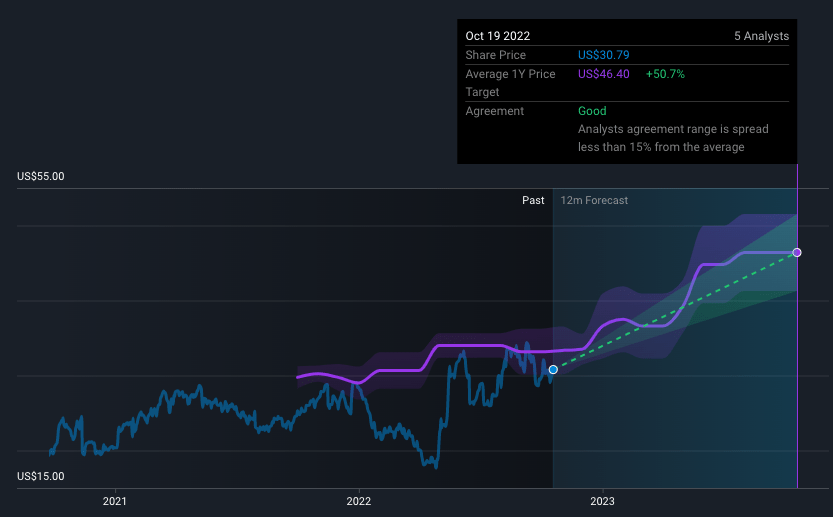

Although we should be cautious of the high debt intake versus the company’s cash flow, I believe there is a lot more upside potential for this fundamentally strong company with a one-year target estimate of $46.40. Increasing shareholder value is the company’s focal point, and activists have already addressed necessary topics such as overly large executive compensation packages and requirements for new faces to enter the very longstanding and possibly outdated board. This stock pays out quarterly dividends and recently provided an additional special dividend payout of $2.00 on July 2022. Therefore, I believe investors may want to take a bullish stance on this company.

Company performance

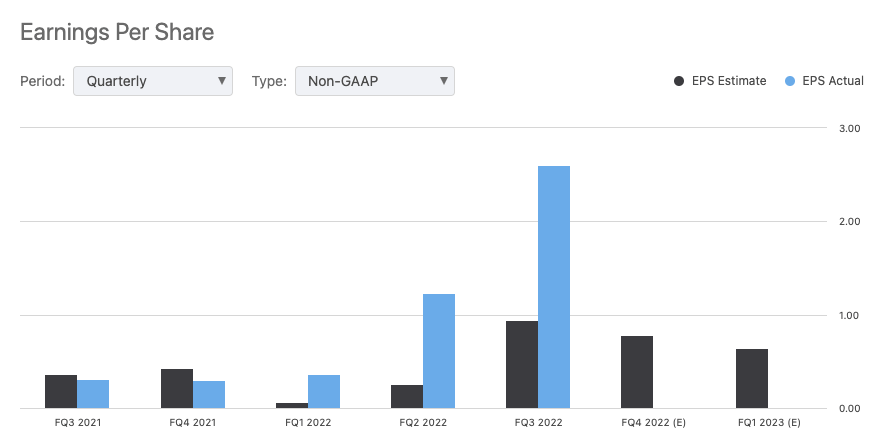

My previous article gave an overview of GFF and its two main segments. The first segment is Consumer and Professional Products (CPP), which brings in $1.2 billion in annual revenue, with an EBITDA of $115 million, and is operated through AMES. It focuses on storage, outdoor lifestyle goods and landscaping tools and products. The second segment is Home and Building Products (HBP) which is operated through Clopay and brings in slightly less at $1 billion in annual revenue but with a higher EBITDA of $181 million. It is focused on the garage and rolling steel doors. The company has beaten EPS expectations for the last three consecutive quarters.

EPS Expectations versus Results (SeekingAlpha.com)

Earnings have been growing in an upward trend, with an overall growth of 111.4% over the last year. This bottom line performance is a positive sign toward the stock price following suit.

A catalyst for change, activist Voss Capital

In the last six months, Voss Capital has increased its ownership in GFF from 2.3% to 5.17%. Voss Capital is a small and young hedge fund based in Houston. Although they are not traditional activists, they have had previous success in other firms in earlier years. After the proxy contest, Charles Diao successfully gained a board seat for Voss on GFF. The activists aim to increase the stock price to $50 through five key action points. They sold off the Defense Electronics business, which took place earlier this year; they want to improve CPP margins; reduce debt by using cash and paying out special dividends. Lastly, they want to minimise corporate overhead costs and investigate alternatives for the HBP sector.

Valuation

Various analysts are optimistic regarding this stock and its future growth potential. Looking at the average price year target, we can see that it is well above the current share price. GFF has a price-to-sales ratio of 0.58, indicating that investors pay less than a dollar for every dollar the company makes in revenue. Furthermore, we have a consecutive quarterly EPS growth trend to back up the predictions.

Average Year Target and One year Forecast (SimplyWallStreet.st)

If we look at Seeking Alpha’s Quant Rating and specifically at the growth of GFF versus other peers in the market, we can see that the company has impressively grown its top and bottom line performance.

Quant Peer Evaluation (SeekingAlpha.com)

Risks

One issue we cannot disregard is the company’s debt-to-equity ratio of 2.87. The outstanding debt is almost three times higher than the company’s equity. It could negatively impact earnings if there are additional costs regarding interest expenses and put the business at more risk if the industry underperforms financially. Furthermore, it has a meagre return on equity of 21.06%. On the more positive side, the company has delivered a return on equity of 21.06% this year.

Another issue to consider is the potential total costs involved with a proxy contest. On average, the cost of a proxy contest campaign can minimise the gains. Investors should be aware of the expenses that can increase if further disagreements exist between the activists and the board of directors.

Final Thoughts

I believe that Voss has opened up the doors to exciting times for GFF. It is a well-performing company that needed a fresh new approach and a review of current practices, especially around corporate governance. Some significant steps have already been taken, such as selling the Defense Electronics business, a Voss board member to the boardroom and a public announcement to strategically review the company. The board will likely have a fresh new look early next year, with nine of the fourteen board members up for election. For this reason, I believe that investors may want to take a bullish stance on this company.

Be the first to comment