Sean Gallup

The current bearish market is sparing no one, not even Alphabet (NASDAQ:GOOG) (NASDAQ:GOOGL), one of the world’s top companies. The macroeconomic environment is experiencing a period of great uncertainty, and tech companies in particular are paying the price. Although Alphabet has proven to be a cash machine in recent years, there is no question that sentiment is changing. The advertising industry is having a downturn, while OpenAI’s new ChatGPT is threatening the efficiency of the Google search engine.

Is there really cause for concern or is this an opportunity to exploit information asymmetries?

First problem: declining advertising

According to the latest quarterly report, about 79% of Alphabet’s revenues come from Google advertising, so this gives an idea of how important advertising is for this company. Also, it is true that the Google Cloud segment is growing strongly, but Google advertising remains the only profitable segment at the moment.

This means that when the advertising industry is on the rise, Alphabet has no problem increasing profits and margins, but when a turnaround occurs there are problems in terms of margins. At this moment in history we are just experiencing that reversal mainly for 2 reasons:

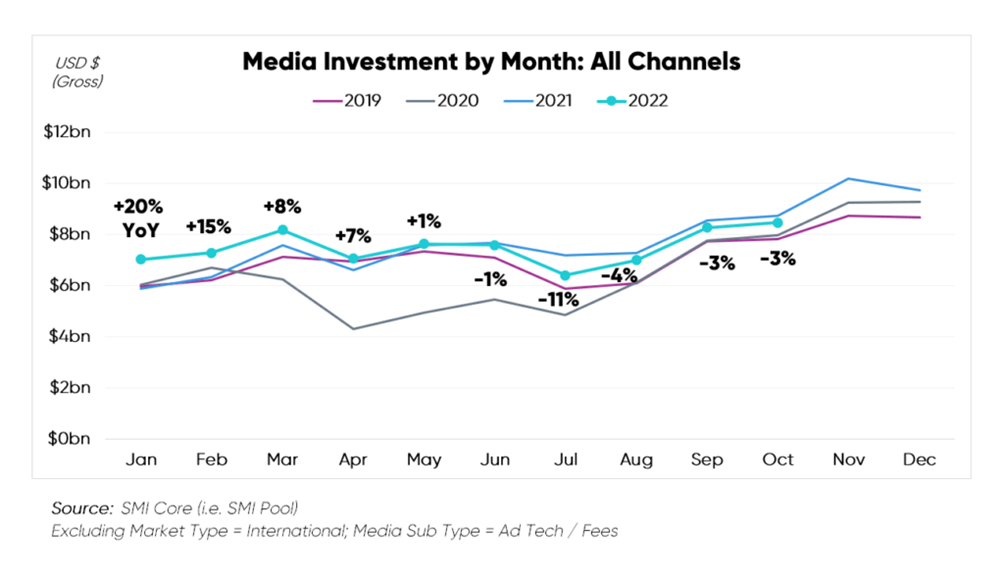

The first is due to a normalization of the industry since 2021 was an extremely good year for the advertising segment. In fact, just think that digital advertising revenue increased by 35.40% year-on-year, the highest growth since 2006. This greatly affected Alphabet’s growth, in fact from generating revenues of $182.52 billion in 2020 it generated $257.63 billion in 2021. Such growth, for a company of this size, is obviously not sustainable in the long run, so it is inevitable that its growth rates will have to scale back after such a sprint. Looking at the Standard Media Index, we can see that the normalization process has already begun as of mid-June.

Standard Media Index

The second reason is related to the current macroeconomic environment that does not encourage investment in advertising. Major central banks raising interest rates are making access to credit more complicated, and high inflation still remains a problem. According to the World Bank, the estimate of global GDP growth in 2023 will be only 1.70%, while only 6 months ago 3% growth was expected. In my opinion, what is most worrisome is not the low growth rate, but in how little time the estimates have deteriorated so much.

In light of such an uncertain economic environment, it is inevitable that companies will try to reduce “unnecessary” spending as much as possible in order to have the readiness to deal with any recession. Advertising, while important for any company, is one of the first expenses to be cut since it is not necessary for corporate survival. However, this does not mean that until macroeconomic conditions improve no more will be spent on advertising, but that in my opinion it is reasonable to expect a reduction in this type of expenditure.

Regarding the forecast for advertising spending in 2023, an interesting survey was conducted by WFA and Ebiquity concerning the size of the advertising budget for this year. This survey was administered to 43 multinational companies, 5 of which were among the top 10 companies spending the most on advertising. Here are the results:

- 29% already planned a budget reduction for 2023.

- 40% said they would leave the budget unchanged for 2023.

- In addition, 75% of the sample said their budget is under heavy scrutiny, with marketers required to justify the investment. EMEA is most at risk, where 30% of respondents said they are planning a major decrease of at least 10%. However, there is also positive news: almost half of the respondents plan to cut offline investments, a segment in which Alphabet has no exposure.

So, after such pessimism, it is not surprising that Alphabet collapsed so much, precisely 45%. Estimates of future growth have shrunk, and consequently so has its fair value. The value of any company is represented by discounting its future cash flows, and if those future cash flows decline, consequently its fair value also declines.

In any case, it is undeniable that this is not a golden time for Alphabet, but is such a slump really justified? In my opinion, no, because overall this is not a potential long-term threat, but only a temporary moment of difficulty.

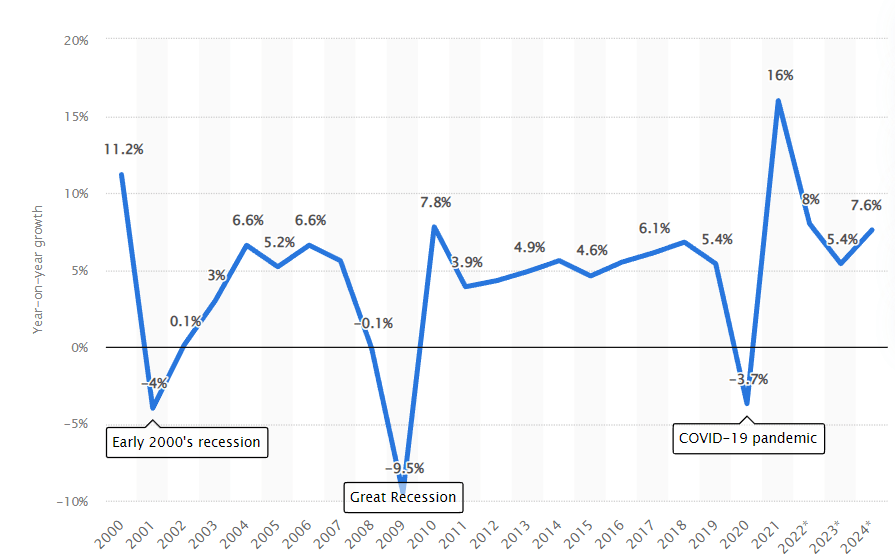

Statista

With the exception of particularly bad years, growth in global advertising spending from 2000 to 2021 has always increased, which is a sign of the resilience of this industry. There may be times of difficulty, but there has always been a recovery. Also, breaking down this industry, we can see that the growth of online advertising is literally outpacing other methods of advertising. Basically, only a few types of advertising are driving the growth of the entire industry, while the others are in steep decline.

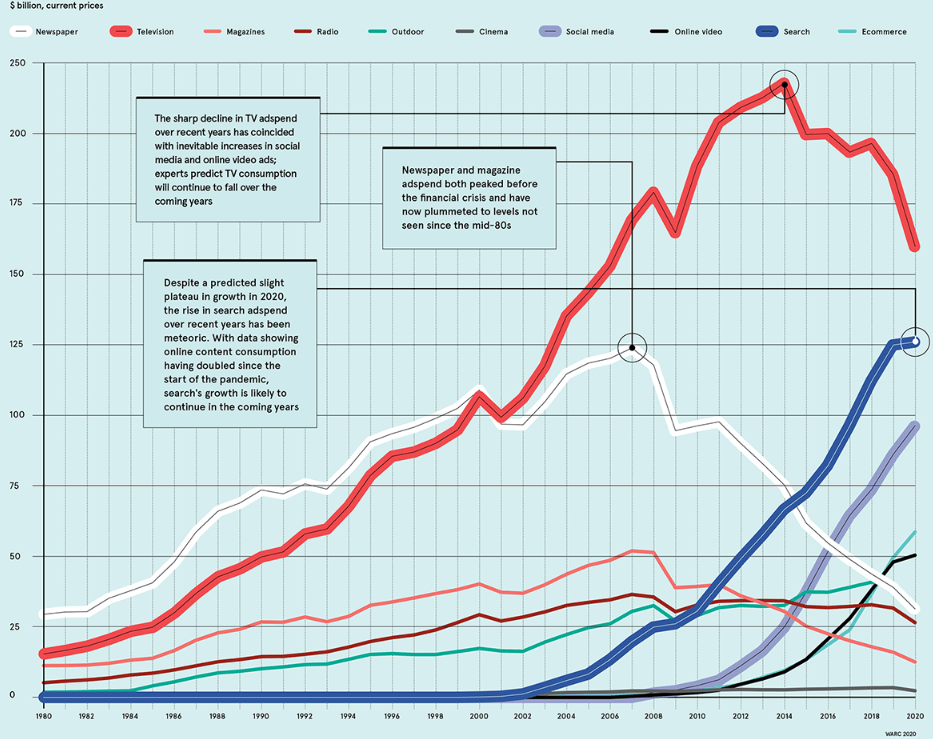

www.raconteur.net

The long-term trend of spending on television advertising is declining, as is spending on magazines and newspapers. The Internet has practically disrupted this industry, and Google has been the main architect as we can see from the positive slope of the curve related to search advertising. Moreover, in terms of future growth, this segment has by no means ended its growth. According to Statista, advertising spending in search advertising is expected to grow by 11.20% from 2023 to 2027, reaching a market volume of $204.10 billion. Benefiting from this long-term growth will obviously be Google in particular, being by detachment the most widely used search engine in the world.

gs.statcounter.com

Overall, it is clear that this is not one of the best times for Alphabet, but personally I am not worried about this company from a long-term perspective. The resources at its disposal are huge, as is its technological and innovative advantage over its competitors. Even big companies have moments of weakness, and that is the right time to buy them, not least because they don’t always collapse by 45%.

Second problem: ChatGPT will destroy Google

Over the past two months there has been nothing but talk about ChatGPT, and I have noticed that not a few people believe that Google will soon become obsolete. ChatGPT ‘s efficiency has surprised the public and apparently Google as well since it issued a code red after the rise of this chatbot. In any case, although these premises are not rosy, in my opinion it is highly unlikely that ChatGPT will destroy Google and now I will explain why. First, however, better to put it in context.

ChatGPT is a chatbot launched by OpenAI in November 2022, an American company operating in the artificial intelligence industry. ChatGPT’s success was immediate, in fact within a week it had already surpassed one million users, certainly not bad. Microsoft (MSFT) had already seen potential in this company in 2019, when it decided to invest $1 billion. To date, much has changed, and after the rise of ChatGPT Microsoft would seem intent on investing an additional $10 billion bringing OpenAI’s valuation to about $29 billion. The aim is to integrate ChatGPT’s technology within the Bing search engine in order to counter the absolute dominance of Google. But how feasible is this plan? In my view there are three obstacles, one of which is almost insurmountable.

ChatGPT may be overrated in my opinion

That this chatbot has remarkable capabilities is beyond question, but are we sure it is worth that much? After using it several times, I noticed mainly three major flaws:

- Not having access to the Internet, ChatGPT does not know the latest information; in fact, its memory is currently limited to 2021. This means that if you want to get updates on the latest thing that happened, you will not be able to do so through ChatGPT. In light of these considerations, it only makes sense to use it if you want to know about events that occurred before 2021, such as a history topic. Or, another common use is for programming and content creation.

- ChatGPT’s answers do not always turn out to be accurate, and this could spread misinformation. There are multiple examples on the web, and I myself have experienced that it sometimes fails to solve even simple logic problems. In addition, since there are no sources cited in the answers there are often questions about their truthfulness.

- Speeches are often tedious and emotionless. Moreover, if you try to get a different answer relative to the same topic, ChatGPT will always give you the same one. On the other hand, I found it useful when you ask him to create something out of nothing based on a set of elements, such as a story in a certain style.

Personally, after using ChatGPT for a couple of days, my interest ended there. Beyond the initial amazement I had no interest in using it on a daily basis, partly because Google manages to provide me with both current and past information, moreover, directing me to websites whose reliability of sources is universally recognized. Having always used Google, it is difficult to change a habit created over the years. The latter is simply my personal consideration, I am curious to read yours in the comments to understand how much and how you use ChatGPT.

Its monetization will not be easy

ChatGPT’s success can also be attributed to the fact that it is a completely free service at the moment, but sooner or later OpenAI will monetize its chatbot since it costs them about $100K each day. There is no information yet on how much the premium version will cost and whether there will still be a free version. Either way it could be a problem since Google is free.

Alphabet knows how to counterattack

Honestly, I was surprised how ChatGPT was mentioned as a “Google killer” but without considering that Alphabet may already have an answer to this threat. In my opinion, it is very superficial to believe that a chatbot created by a semi-unknown company can destroy a behemoth that generated $67 billion in free cash flow in 2021 and has been investing in artificial intelligence for decades. But then, why has there been no response from Alphabet so far? Where is its response to ChatGPT?

The answer is there, but further verification is needed in order to avoid any reputational risk. Alphabet is a company worth $1.20 trillion, a world leader and synonymous with security and reliability, so, having much more to lose than OpenAI, it must necessarily provide an excellent service and not a mediocre one. Just think of the consequences of a Google chatbot spreading fake news, or worse, likely to generate disturbance in the people with whom it interacts. In addition, Alphabet is still trying to understand the monetization aspect being a new business segment. How will the chatbot affect profit margins? How will the chatbot be integrated? These are all questions that OpenAI is also asking, but they obviously carry significantly less weight than the Mountain View giant. That said, Alphabet’s answer is called Sparrow and it may come sooner than expected because of the immediate success of ChatGPT.

Sparrow is an artificial intelligence-based chatbot developed by DeepMind, a subsidiary of Alphabet. Its CEO, Demis Hassabis, revealed in a recent interview that Sparrow will be released for a “private beta” in 2023. The delay in the chatbot’s release is due to a desire to improve its learning-based features as much as possible, as well as provide the ability to cite sources. This would help reduce the risk of spreading misinformation, as well as improve the credibility of responses. In addition, Sparrow will have access to the Internet through Google, which will allow it to keep up-to-date unlike ChatGPT. In short, overall Sparrow has traits that make it more reliable, and the fact that it is backed by Alphabet is another point in its favor.

In light of all these considerations, integrating ChatGPT to Bing I believe is not the solution to weaken Google, at least not in the long run. There may be a general excitement in the coming months that will cause ChatGPT to gain more and more acceptance, but once Sparrow is released I expect all the hype toward it to fade. In my view, Alphabet’s problem will not be so much competing with ChatGPT, but figuring out how to monetize Sparrow and make it profitable enough that it does not reduce the profit margins of the entire company. Chatbots could be the future, but the problem is figuring out how to best integrate them.

Before I move on and make a quantitative valuation, I want to point out one thing to avoid misunderstanding. I do not think ChatGPT is useless and only spreads misinformation; on the contrary, it is very useful and more and more people are using it, even in the business world. With ChatGPT, an epochal turning point could begin where our method of searching for information will totally change and search engines will become increasingly obsolete. In any case, I don’t see another company with more possibilities and resources than Alphabet to excel in this area. Of course, I could be wrong; I certainly don’t have a crystal ball.

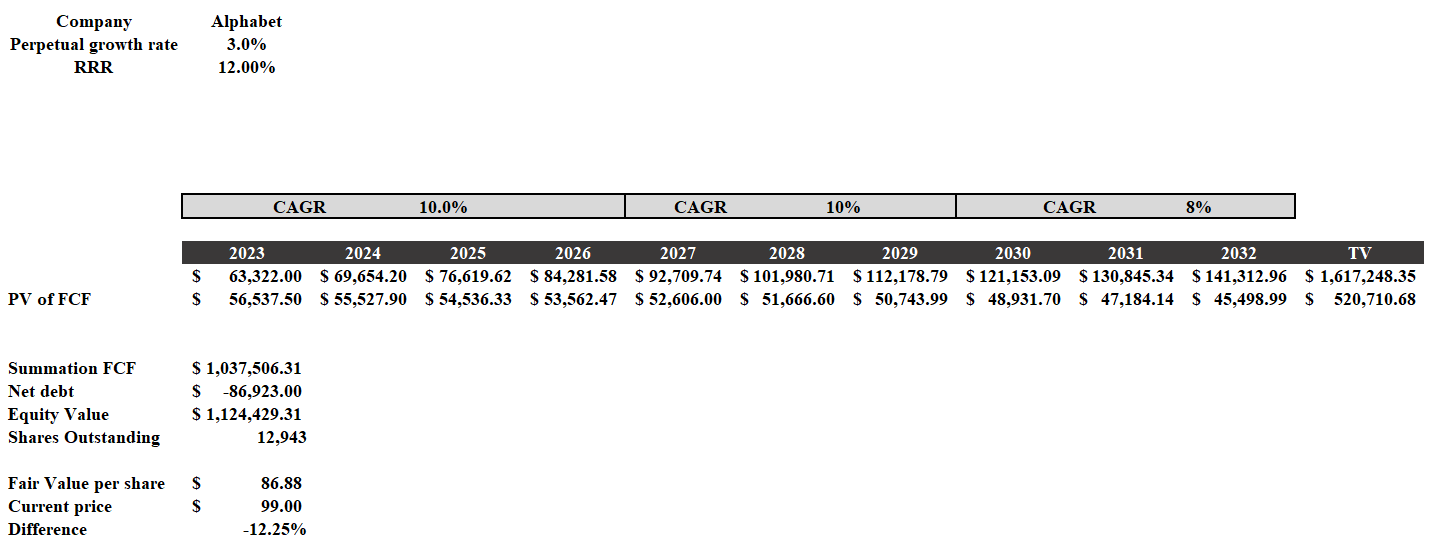

Discounted cash flow model

So far, I have been quite positive about the future of Alphabet, however it is not enough to justify an investment. A quantitative analysis is needed, and I will conduct it using a discounted cash flow model. This model will be constructed as follows:

- The FCF of the year 2023 was estimated by analysts at TIKR Terminal, and thereafter I considered an annual growth rate of 10% until 2029 and then reduced to 8% until 2032. In recent years Alphabet has been growing as much as 20-25% per year, becoming basically a giant, and I doubt it can achieve these growth rates in the future as well. Anyway, I recognize that I may have been too pessimistic, in fact TIKR Terminal analysts estimated that in 2026 the company will generate an FCF of $115.91 billion, not $84.28 billion. Estimates are often very subjective and I prefer to be quite conservative.

- The Required rate of return (RRR) will be 12% and represents the minimum annual return I would like to get from this investment. Investing in a single company is risky, so I require a higher return than a simple ETF that replicates the performance of the S&P500.

- TIKR Terminal is the source of net debt and outstanding shares.

Discounted cash flow

According to my assumptions, to achieve a 12% annual return it is required to buy Alphabet around $86 per share, so we are quite close to that price range. When I started writing this article I was intending to consider Alphabet as a strong buy, but after the recent surge in the last week I think it is more appropriate to consider it only a buy. In any case, buying Alphabet at $90 per share or $99 per share I think is almost irrelevant to those with a very long-term view. If Alphabet performs well over the next 10 years a price difference of $9 will change little.

Be the first to comment