Sean Gallup/Getty Images News

I’ve previously written a number of articles discussing the resiliency of Alphabet’s (NASDAQ:GOOG) (NASDAQ:GOOGL) business during a recession and why investors should not worry about the search engine giant however depressing the current macro narrative may be. Having repeatedly received questions as to what exactly will happen to shares of Google in a recession, I’ve decided to come up with an analysis of an absolute worst case scenario for 2023.

Digital advertising in 2022

It’s important to first understand the state of the digital advertising sector to get a sense of how things are progressing in a post-Covid environment. While all players in the space saw positive top-line growth in 1Q22, challenges began to surface in Q2 as companies lapped tough 2021 comps. More importantly, the outlook provided by most management teams was frankly terrifying.

Company, consensus estimates, Albert Lin

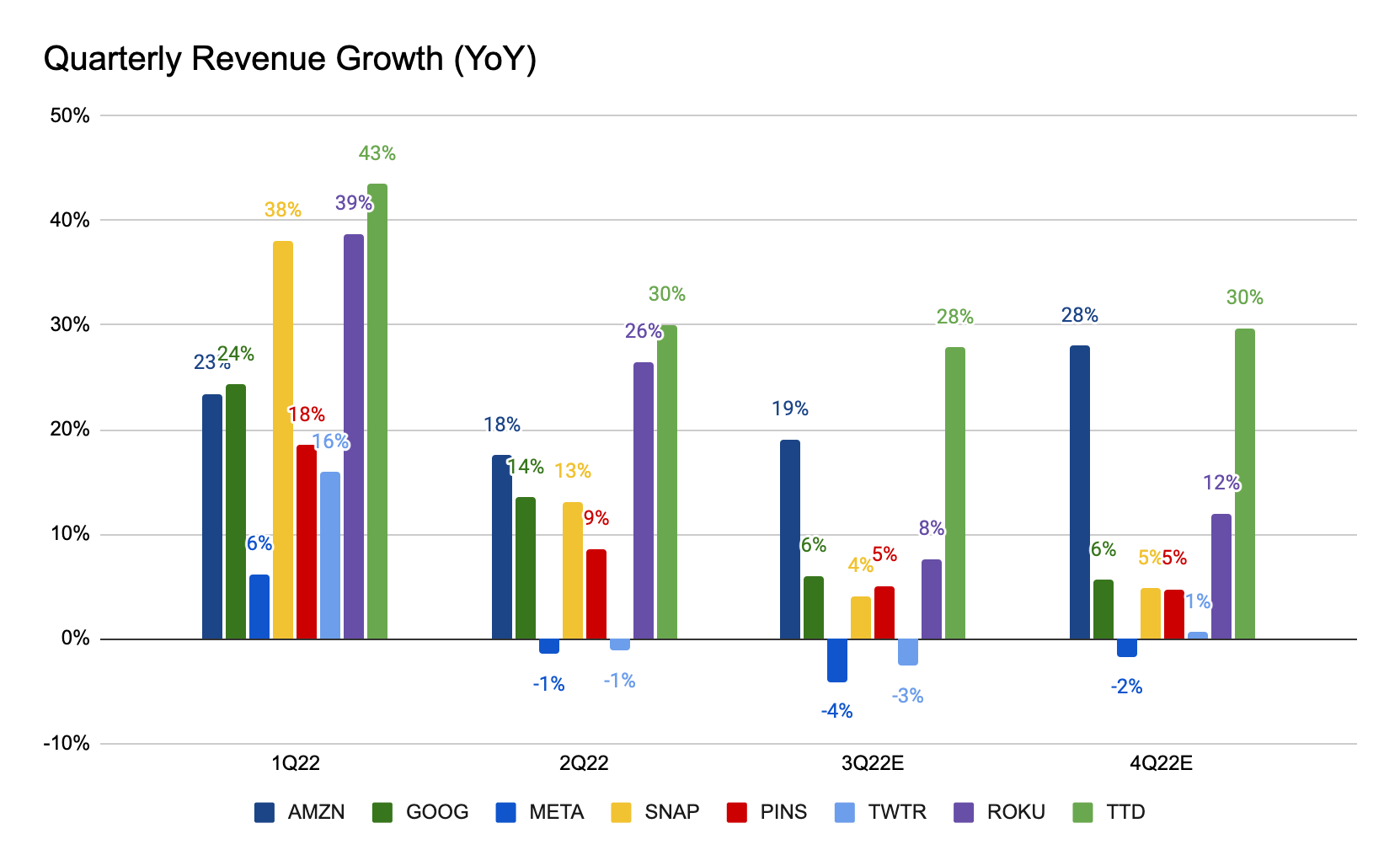

Meta (META), the largest social media platform in the world, reported negative revenue growth in Q2 and provided Q3 revenue guidance that was 10% below Street estimates as management pointed to worsening macro conditions. Snap’s (SNAP) revenue growth fell off a cliff in Q2 as CEO Spiegel cited a challenging macro from inflation to the Russia-Ukraine crisis and did not provide Q3 guidance. While Roku’s (ROKU) ad revenue grew 26% in Q2, guidance for the current quarter was >20% below consensus as the team blamed on a weak scatter market and subsequently canceled its full year 2022 outlook. The Trade Desk (TTD) was a blossom in the dessert with 30% growth in Q2 and a beat in Q3 guide was a major surprise to the Street, but that doesn’t make Q4 any more predictable given the current economic outlook.

On the bottom end of the marketing funnel where advertisers are more focused on conversion over impression, Amazon Advertising (AMZN) proved to be highly resilient as consumers are literally standing in front of sellers on the e-commerce site. As much of a giant as Google is, Q2 Search revenue still grew 14% following 24% in Q1. Predicting 2H22 growth was a difficult exercise for analysts as management didn’t provide quantitative guides, so the Street isn’t getting its hopes up as Search revenue grew 44%/36% in 3Q/4Q21.

In short, what one can easily conclude for the digital advertising space (as well as for most industries) is that winter is here, and the setup for 2023 doesn’t look so good as the economy is heading into a recession if not already in one. The question now becomes: what will Google look like in a 2023 recession?

Coming up with the worst case scenario

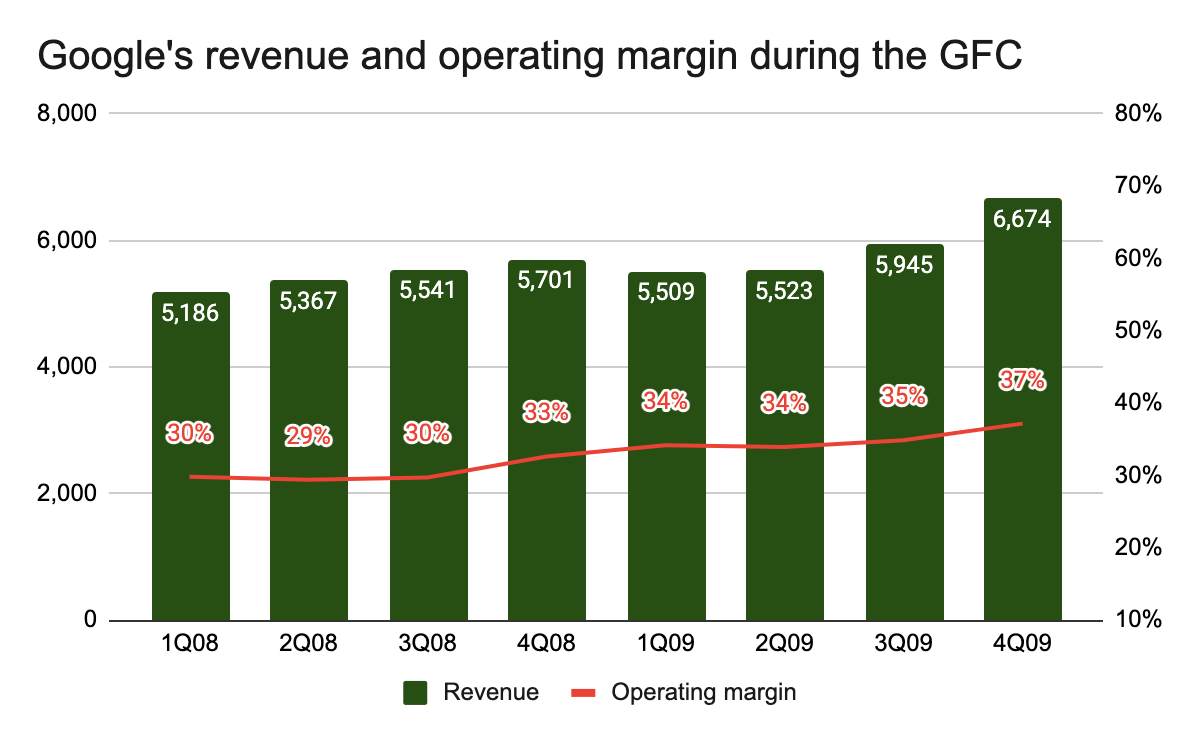

While there are no perfect methods to accurately forecast Google’s top and bottom line in a recession (since we have no idea how bad things will be), we can first borrow from history that Google obviously experienced a meaningful decline in revenue growth during the 2008 Global Financial Crisis driven by indiscriminate mortgage lending in the United States of America. Throughout the crisis, Google saw its quarterly revenue growth decelerate materially from +42% in 1Q08 to +18% in 4Q08 and eventually bottomed out at +3% in 2Q09 before re-accelerating to +7% in 3Q09 and +17% 4Q09. For the entire 2008 and 2009, however, revenue still grew 9% and 8%, a highly respectable feat as the world was literally falling apart.

Company data, Albert Lin

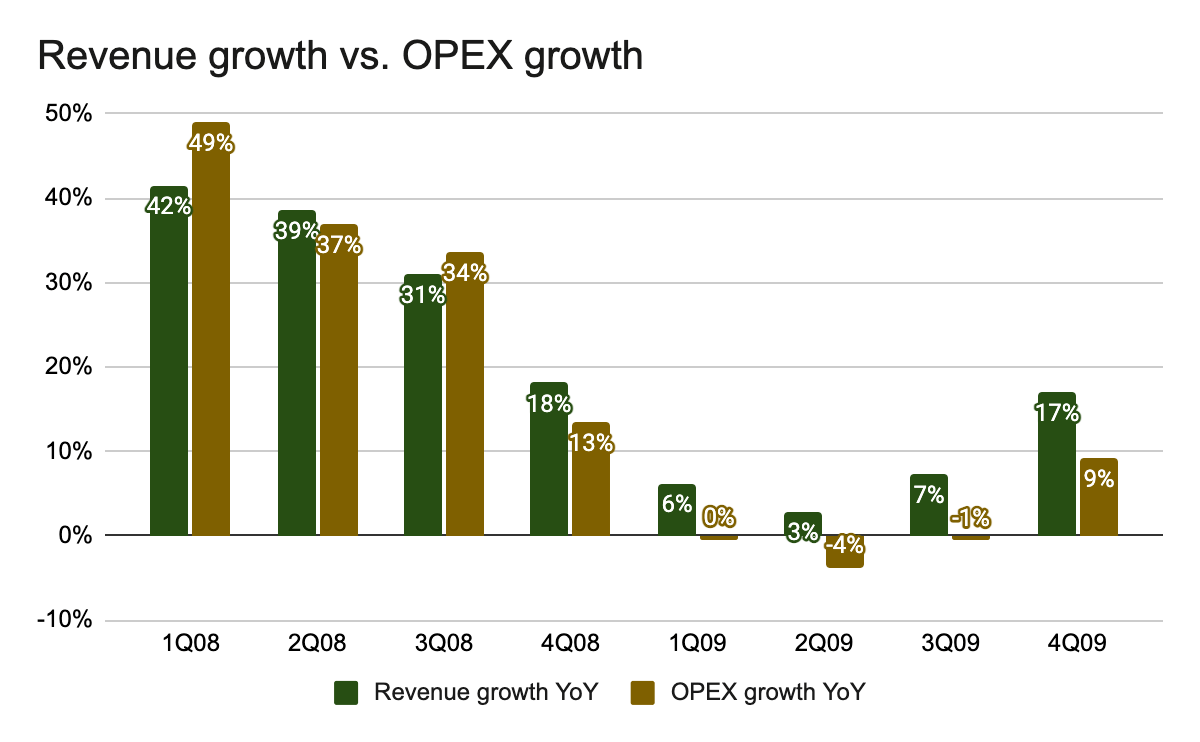

As bleak as things were, what was frankly a positive surprise to investors was that Google was able to protect its operating margin by containing costs throughout the global recession. While year-over-year top-line growth slowed from over 40% to single digits, changes in operating expenses were largely in line with revenue. OPEX actually declined for two consecutive quarters in 2009 and only ramped up in Q4 when revenue growth was back to double digits.

Company data, Albert Lin

Now that we have a basic understanding of how Google fared in the 2008 recession, we can assume with some degree of confidence that Google will at least be able to demonstrate flexibility on the expense side of the equation should top-line growth begin to slow materially in the next (or current) recession.

The question now is how much revenue growth will fall. Since digital advertising was still in its infancy back in 2008, it’s conceivable that digital ad budgets will likely experience a bigger impact today given the >65% penetration vs. 12% back then. For this reason, we can probably imagine a worst case scenario of 0% revenue growth in 2023 vs. +8% in 2009. Given Google is still very much an advertising company, we will focus exclusively on the Google Services segment (90% of revenue) for now.

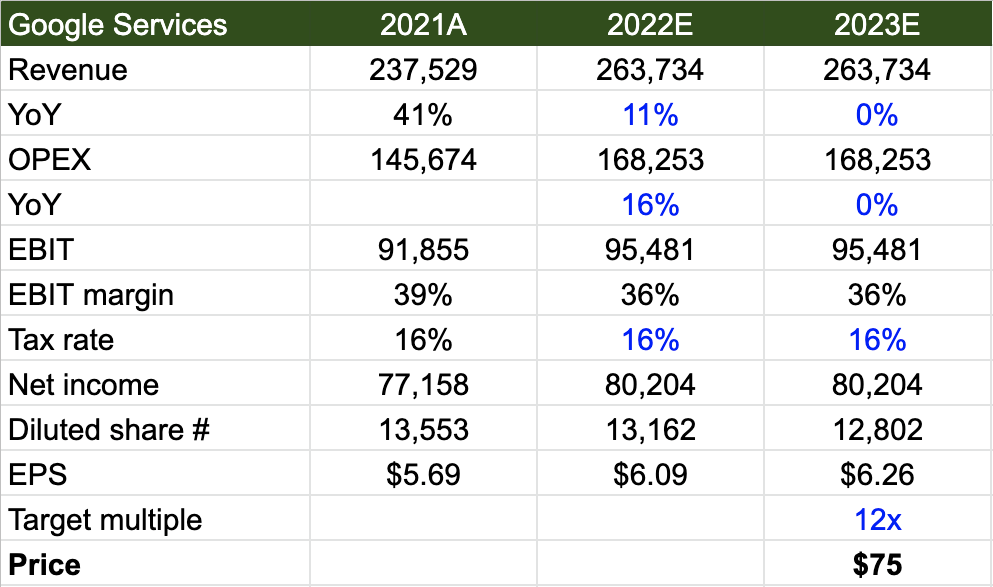

The current 2022 consensus calls for Google Services revenue of ~$264 billion, which implies an 11% YoY growth on an exceptional 41% growth in 2021. Operating income is estimated to come in at ~$95 billion for an EBIT margin of 36% vs. 39% in 2021. With an effective tax rate of 16%, Google Services should generate net income of ~$80 billion and EPS of $6.09 in 2022.

Company data, Albert Lin

Based on how Google managed costs during the 2008 recession, I’d expect OPEX growth to stay flat just like revenue, leading to an EBIT margin of 36% in 2023. Already, CEO Sundar Pichai has indicated that he wants to make Google 20% more efficient. Assume the same 16% tax rate, this should come down to an estimated EPS of $6.26. The ~3% increase in EPS primarily comes from buybacks, for which Google has plenty of financial firepower. At the end of 2Q22, Google had $58.9 billion remaining in its buyback program after approving $70 billion for share repurchase in April 2022. There’s $125 billion of cash on the balance sheet, which indicates a strong possibility for more buybacks in the future.

During the Global Financial Crisis, Google’s P/E multiple contracted from 33x in 4Q07 to 12x in 4Q08. Applying the same trough multiple of 12x, we can arrive at a per share value of $75 for Google Services in 2023. At this price, markets should have sufficiently priced in a full blown recession and investors would theoretically be paying $0 for Google Cloud and Other Bets.

Company data, Albert Lin

It’s unclear how Google Cloud will perform in a recession given cloud migration is more of a structural vs. cyclical story, but suppose Google Cloud grows 30% in 2022 and growth gets cut in half to 15% in 2023, Cloud revenue is estimated at $28.7 billion or $2.24 on a per share basis next year. Applying a depressed 2x P/S multiple should give us a value of $4 a share. Taken altogether, we should have a worst case scenario of $79 for Google’s shares in a recessionary environment.

Final thoughts

The bad news is Google’s stock may have a 20% downside if markets are to price in a full-blown recession. The good news is Google was able to demonstrate strong resiliency in managing its bottom line in the last economic recession. Net-net, I continue to see Google as a high-quality company that should fare relatively better than most in this recession and would remain on the buy side to capitalize on further price weakness going forward.

Be the first to comment