alleachday/iStock via Getty Images

PERFORMANCE as of May 31, 2022

|

6 months ended 5/31/22 |

1 year ended 5/31/22 |

2 years annualized as of 5/31/22 |

12/31/19-5/31/22 as of 5/31/22 |

5 years annualized as of 5/31/22 |

10 years annualized as of 5/31/22 |

since inception annualized1 as of 5/31/22 |

|

|

GOODX |

-3.86% |

3.41% |

27.01% |

12.56% |

8.93% |

5.93% |

6.00% |

|

S&P 500 Index2 |

-8.85% |

-0.30% |

18.28% |

12.49% |

13.38% |

14.40% |

12.94% |

|

Wilshire 5000 Total Market Index |

-10.32% |

-6.55% |

15.21% |

12.23% |

12.97% |

14.13% |

12.56% |

|

HFRI Fundamental Growth Index3 |

-12.00% |

-12.27% |

11.57% |

7.03% |

5.76% |

5.63% |

3.60% |

|

HFRI Fundamental Value Index3 |

-3.67% |

-6.28% |

17.43% |

9.34% |

7.31% |

7.60% |

6.09% |

|

CS Hedge Fund Index3 |

3.84% |

3.36% |

10.76% |

6.82% |

5.16% |

4.83% |

4.11% |

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent monthend may be obtained by calling (855) OK-GOODX or (855) 654-6639. The Fund imposes a 2.00% redemption fee on shares redeemed within 60 days of purchase. Performance data for an individual shareholder will be reduced by redemption fees that apply, if any. Redemption fees are paid directly into the Fund and do not reduce overall performance of the Fund. The annualized gross expense ratio of the GoodHaven Fund is 1.10%. |

“Markets Post Worst First Half of a Year in Decades: Investors gird for more volatility; almost everything – from stocks to bonds and crypto – falls to start 2022” – Akane Otani, Wall Street Journal 6/30/22

“Information cannot serve as an effective substitute for thinking.” – Bernard M. Baruch

“We used to spend like $200 or $250 of shipping, all-in, on a piece of hardware. Today, it’s north of $900.” – Barry McCarthy Peloton CEO

“Nothing is so firmly believed as that which we least know.” – Michel De Montaigne

When we last wrote to you in January the world was at relative peace. Interest rates were slowly climbing. The oil markets were balanced, and inflation was higher though seemingly manageable. Global stock markets were stable. We write to you – six months later amidst an ongoing war in Europe, rampant inflation, dramatically higher interest rates, and shortages and supply chain issues affecting many goods and commodities. Most global stock markets have recently experienced material declines and some sectors have been decimated. Talk of imminent recession – or worse – are commonplace.

For the 2022 semi-annual fiscal period, we materially outperformed the S&P 500 – declining 3.86% vs. a decline of 8.85% for the S&P 500. Here are a few other statistics to capture the progress at GoodHaven 2.0: Since immediately after our reorganization, from 12/31/19 through the current fiscal period, we slightly outperformed the S&P 500 and the Wilshire 5000 and strongly outperformed most of the other indexes in the chart on the previous page.

Over the last two semi-annual fiscal years we have handily outperformed all of the indexes we compare against. For those around since we started, while we have regained much relative ground, we still have work to do to improve our since inception results.

People sometimes ask if we focus on relative returns (compared to a benchmark) or absolute returns (without regard to a benchmark). Our answer is – both – over the long term. We won’t be satisfied with mediocre long-term returns (even if they are positive) that trail the index. We also won’t be celebrating a slightly less material decline than the index in a weaker period. However, we remind you that the portfolio is not designed to avoid volatility or periodic drawdowns over the short term.

We are striving for strong, long-term returns on a relative and absolute basis through our ownership of high-quality companies and opportunistic special situations that have outsized return potential, all purchased with a significant margin of safety. Ours is a concentrated portfolio and there will be some periods of underperformance in future periods.

In the summer of 2020, we wrote that no one needed (another) armchair epidemiologist and so we stuck to talking about (and thinking about) the portfolio and how we were then allocating capital for us all while mindful of the risks, rewards, unknowns and probabilities present. Books will be written about the geopolitical and macro events of the last few months, but not by us.

The best use of our time and intellectual resources is to focus on the business analysis of our holdings – combined with portfolio structuring and trying to opportunistically take advantage of market volatility – while being mindful but not predictive of macro events. However, the sea change lately regarding interest rates and inflation, although discussed in the past and previously considered in our positioning, has our attention and will be discussed later.

TABLE OF TOP 5 GAINERS & DETRACTORS ($’s)

|

Contributors (11/30/21 – 05/31/22) |

Detractors (11/30/21 – 05/31/22) |

|

Devon Energy Corp. (DVN) |

|

|

Jefferies Financial Group Inc. (JEF) |

|

|

Alleghany Corp. (Y) |

Meta Platforms Inc. – Class A (META) |

|

The Progressive Corp. (PGR) |

Lennar Corporation – Class B (LEN) |

|

Hess Midstream Corp. – Class A (HESM) |

KKR & Co Inc. (KKR) |

Alphabet was our top dollar detractor after having been a top gainer in many prior periods. As a top holding in our portfolio, its price movement will often impact overall performance in either direction. Alphabet’s Q1 2022 results were strong, the top line increased by 26% and operating income increased by over 20%.[1]Shares outstanding have begun declining due to stepped-up share repurchases. We’ve owned Alphabet for many years and for almost all of that time have been expecting growth to moderate.

We’ve been happily proven wrong so far but that expectation remains. As many companies in the tech/venture capital world retrench and possibly reduce their spending on digital advertising, we would not be surprised to see this negatively impact Alphabet’s growth. At a recent stock price implying a forward P/E of about 14X to 2023 earnings (excluding net cash) we remain optimistic about Alphabet’s long-term upside potential and ability to navigate the regulatory headwinds.

Jefferies Financial was our next biggest dollar detractor, and had also been a strong contributor in prior periods. As we have previously mentioned, while Jefferies has become a better business it is still a cyclical business, and that some moderating earnings after the recent boom were to be expected. In the first six months of their fiscal 2022, Jefferies earned a ROATE (Return on Adjusted Tangible Equity) of over 11%, reasonable given the very material slowdown in the capital markets lately.

They also repurchased over $620 million of their shares at $34+ per share and Jefferies’ stock now trades below tangible book value/share. Given the obvious slowdown in capital raising transactions industry wide, we expect continued muted results in the near-term but also continued share buybacks. Our long-term enthusiasm remains, as does our view of the material upside for the shares from recent levels.[2]

Our biggest dollar gainer within this period was Devon Energy, a position which emanated from a takeover in early 2021 of our long time holding WPX Energy. We are sitting on a material (unrealized) gain from our cost and are now receiving material dividends thanks to Devon’s thoughtful fixed/variable dividend policy. Energy is now a hot sector for investors but we have had a material exposure for a long time. We remember a bit too well $40 oil, NEGATIVELY PRICED front-month oil contract, and what it’s like to own a company with leverage and negative free cash flow during such periods.

Our desire to have our biggest portfolio exposures be high return, growing, reasonably predictable and moderately levered companies lead us to reduce our Devon exposure in the past. When the recent facts and circumstances for the industry changed and appeared supportive of healthy oil prices, we decided to maintain a sizable holding and more recently added to the position. At Devon’s Q1 dividend rate, which is mostly variable in nature, the shares now yield approximately 10% and our yield on our average cost is materially higher.

In addition, we maintain additional energy exposure through our long-term (and successful) holding in Hess Midstream and less directly through TerraVest (OTCPK:TRRVF) and Berkshire Hathaway’s energy investments.

Berkshire Hathaway was our next biggest dollar contributor. We are pleased with recent earnings and capital deployment and we feel the shares remain undervalued. Other investors seem to have awoken to the positive things we have been saying about Berkshire over the past few years. We remind you that Berkshire’s Buffett and Munger will unfortunately no longer be running the company one of these days but that we are currently comfortable with the possible ways management succession may evolve.

Another broad sector now garnering investor attention that we had established exposure to a while ago are financial companies that might benefit from the new higher level of interest rates. Back in July 2021 we wrote saying:

“Our portfolio in aggregate has a material exposure to businesses that are in many ways “financial companies.” Holdings that are directly/indirectly involved in commercial banking, investment banking/trading, asset management, insurance, and conglomerates with investments in those sectors, include: Jefferies, Bank of America, JP Morgan, Berkshire, Brookfield Asset Management, Alleghany, Progressive, KKR, Exor, Chubb, and Guild Holdings. Many of these sectors have remained undervalued over the last few years, beset by different investor worries such as 1) low interest rates/spreads will never improve, and may worsen, ala “Japanification,” 2) newer “fintech” competitors will take material market share from existing players, 3) trading and loan losses will overwhelm capital in a downturn, ala the global financial crisis, and 4) climate change will increase insurance risks and more. These are good concerns, and we feel we have good answers, and so we have found these areas to be a fertile category for new and larger investments. We are pleased with our exposure and results from this eclectic group.”

Alleghany was our next biggest dollar gainer. We had added to Alleghany on a few occasions earlier in the period, making it a top ten holding. We had intended to use this letter to discuss our positive outlook for the company given its recent strong results, a thoughtful 2021 shareholder letter from new CEO Joe Brandon, and a cheap stock price. On March 21, 2022, we were surprised when it was announced that Alleghany had entered into an agreement to be acquired by Berkshire for $848.02/share in cash.

Wearing our “Berkshire hat,” we love the acquisition for its attractive price in an industry Berkshire knows better than anyone. We also like the potential that Joe Brandon may again be part of Berkshire going forward. However, nobody has ever said “boy Warren Buffett paid top dollar for that acquisition.” Wearing our “Alleghany hat,” we would have hoped for a buyout at a higher price and a deal in stock versus cash so we might have the option to participate in the future (and not pay current capital gains tax).

Higher interest rates will help many of our financial companies who maintain large, fixed income and cash equivalent holdings. A reminder that the insurance focused companies will likely report material “mark to market” declines in the prices of their bond holdings as required by GAAP. This is more noise than underlying economic impact for our companies but it will garner some headlines when earnings are reported.

We have had for some time a material exposure to two companies, Lennar Corp and Builders FirstSource (BLDR), that operate in/around the housing market. Our long-term enthusiasm for their future remains unchanged. On the way up we reminded you that although these had become better businesses (an important part of our thesis), they were still cyclical businesses and that we prepared to own them through a normal housing cycle, versus trying to predict the cycle. In July 2021 we wrote:

“One of these days the red hot housing market will slow – in fact a more normalized pace of demand might be better – as Lennar and its brethren are striving to balance very strong demand with higher raw materials and tight labor markets. While we trimmed our Builders FirstSource position to free up funds for new buys, we remain very constructive on both Builders and Lennar’s long-term prospects. Expect periodic normal demand slowdowns from time to time, though we think slowdowns will be less pronounced than in prior cycles.”

Recent financial results for these companies have ranged from strong to exceptional. Builders adjusted EBITDA (Earnings before Interest, Taxes, Depreciation, and Amortization) more than doubled in Q1 YOY (Year over Year), while also repurchasing $1.5 billion shares in the past two quarters. Builders stock currently trades at a price to earnings ratio of about 5.4x and price to free cash flow of 5x based on FY 2023 market estimates.

Although housing starts may slow from its recent peak, we remain optimistic on the company’s ability to navigate this period defensively and the opportunity to further gain market share that is supported by its strong balance sheet. Builders had less than 1x net debt to EBITDA in the most recent quarter, and has no debt maturities until 2030.

Lennar’s Q2 earnings increased 49% while also repurchasing almost $850 million of shares YTD. The Lennar “B” shares currently trade at a FY2023E price to earnings ratio of about 4x and price to free cash flow of 5x. Industry trends have softened recently after the spike in mortgage rates, however on Lennar’s recent Q2 2022 earnings call, management commented that demand remains reasonably strong and although cancellations and incentives have ticked higher, both remain significantly below historical levels.

Lennar’s spin-off of non-core assets is on schedule for year-end. The shift to an asset light land strategy is close to complete with approximately 62% of homesites controlled through land options, which should improve the return on invested capital while also potentially providing downside protection in a weaker environment. Lennar has one of the lowest net leverage ratios in the industry that is also less than half its own level during the 2018 housing slowdown.

Ten-year treasury yields have recently almost doubled from around 1.60% to around 3.00%. Mortgage rates have risen materially as well. Lumber prices have declined lately which over the short term can negatively impact Builders’ results. We anticipate more negative impacts in the near-term to their businesses (as does “Mr. Market”) but feel current stock prices compensate for this likely cyclical weakness. Our view on the U.S. long-term housing demand/supply and demographic trends remains intact, and our appropriately sized housing exposure allows us to participate in this growth tailwind with a significant margin of safety.

Other activity in the period included eliminating our holding in PG&E (PCG) and adding a few new holdings – the luxury furniture and lifestyle company RH(formerly Restoration Hardware) and Goldman Sachs (GS). A few important developments changed at PG&E including higher future capex plans and changes in long-term guidance, and so we changed our mind and sold. Purchases were made on a handful of occasions in 2020 and mid-2021 at an approximate average price of $9.20 and fully sold during February 2022 at an approximate average price of $11.42, earning approximately 24%.

We have for some time admired what RH’s unique leader Gary Friedman and his team have built at RH and what we think the future holds. After the shares declined more than 30% from the early December 2021 high, we established a position and have increased our holdings more recently.

Referring to RH as a furniture company is technically accurate, but a very incomplete description of where the company is headed. Gary has a unique blend of management skills and we look forward to writing about this holding and potentially materially increasing the position opportunistically, cognizant that the coming housing market slowdown will likely negatively impact results at RH as well. We also initiated a position in Goldman Sachs at an inexpensive valuation and are attracted by the potential durability of the company’s ability to generate high returns on equity driven in part by the growth in their existing and new franchises.

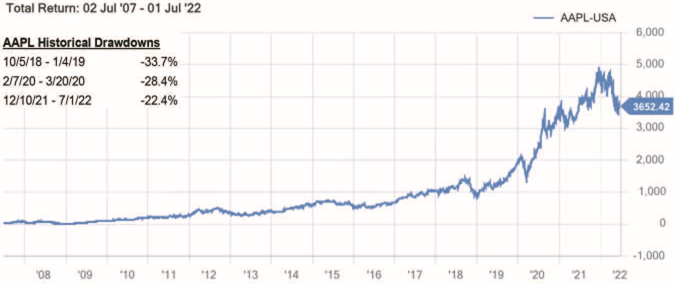

Earning above-average (and tax efficient) long-term compounded returns from part ownership of a unique company normally requires experiencing – and not getting shaken out by – some material declines along the way. The below chart and statistics from Apple (AAPL) over the past fifteen years – as an example – are an instructive reminder of this.

Data from FactSet.

Have we entered a new economic paradigm where interest rates only go up, oil remains in short supply and prices stay above $100/barrel and inflation is not transitory but stays elevated? Will tighter monetary policy and inflation send us into a recession? Are we already in a “bear market”? We don’t know, and if someone expresses certainty in these areas don’t forget that most of the time people’s views on such things tells you a lot about the person but very little about what might happen in the future.

Having a fervent view on something and being wrong for ten years and right in year eleven does not make you prescient – it makes you slightly less wrong. However, these are dramatic recent shifts, so it’s worth reviewing our positioning. Since our reorganization we have upgraded the portfolio to more holdings that earn high returns on capital and have pricing power – which should be helpful if inflation remains high. We have opted to selectively maintain a material, but appropriately sized, exposure to energy and to gold companies.

None of these moves are binary macro decisions, that’s not what we do. They are an outgrowth of allocating capital to strive for above average returns with manageable risk and consistent with the evolution of GoodHaven 2.0. We think we are positioned well whether or not a new inflation paradigm is upon us, which by the way is a “consensus” view. Finally, some signs of supply chain improvements and excess retailer inventories appear daily and might help the inflation outlook.

After the end of the fiscal period, most markets have weakened further. As a reminder, our strong returns after the spring 2020 weakness were due in no small part to opportunistic purchases made around that March downturn. We do not think the current economic backdrop is fraught with the existential business risks that were present in 2020. Much of the recent market contraction has been a decline in valuations, not earnings. Some adjustment in the valuations of businesses and assets from higher interest rates is logical.

Our recent pace of adding to existing positions and initiating new investments has accelerated and we will keep looking to take advantage of the market volatility while being mindful of any potential exogenous downside risks. We are now even more optimistic in our outlook for potential future portfolio gains given recent price (not value) declines and the undervaluation we believe exists in our portfolio today. As we have said for a while – dramatic price volatility in security prices over the short term is the new normal, we expect it even if we can’t predict it and will try and use it to our advantage.

Over the long-term we expect continued economic growth – as we have all seen in the past – with bumps along the way.

The firm continues to run smoothly and efficiently on the operations, administrative, and client services side thanks to our dedicated and talented David Gresser and Lynn Iacona, both of whom have been with GoodHaven since its inception. Artie Kwok – our long-time senior analyst – has recently become a partner, in recognition of his contributions and valuable insights.

I thank all fellow clients for their confidence as GoodHaven 2.0 continues to unfold. During the fiscal period I have added to my personal fund holdings. I also thank our Fund Board of Trustees and our long-time partner and investor Markel for their support and wise counsel.

Stay healthy and safe.

Larry Pitkowsky

Footnotes

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment