Chris Hondros

Just when we thought Goldman Sachs (NYSE:GS) CEO David Solomon pulled the bear case against its Q4 and FY23 outlook at its Q3 earnings call, he decided to go even further.

It was reported recently that Solomon informed his employees that the leading investment bank would conduct its layoffs in January, as he emphasized:

We are conducting a careful review, and while discussions are still ongoing, we anticipate our headcount reduction will take place in the first half of January. There are a variety of factors impacting the business landscape, including tightening monetary conditions that are slowing down economic activity. For our leadership team, the focus is on preparing the firm to weather these headwinds. – Bloomberg

Therefore, Solomon appears to be planning for worse headwinds than what his strategists have postulated for the US economy in avoiding a recession in 2023. Notably, his strategists see US GDP increasing by 1% in 2023, more optimistic than the Fed’s revised median estimates of a 0.5% uptick, based on the most recent summary of economic projections.

Goldman Sachs’ strategists are not alone in their prognostication of “no recession,” supported by their counterparts from Morgan Stanley (MS) and Credit Suisse (CS). Yet GS was also reported as being more aggressive in cost/headcount cutting than its Wall Street peers.

Therefore, Goldman Sachs investors have likely received mixed messages from management and their strategists/economists in deciding whether GS might miss its earnings in Q4 and proffer a worse-than-anticipated outlook.

Despite that, we believe market operators are likely not unduly concerned over Goldman Sachs’ outlook in 2023, even as it could revise its guidance. Why?

While cutting staff could imply the bank could be struggling to meet its profitability targets, it also indicates that Goldman Sachs is willing to take decisive action to slash costs, given worsening macroeconomic headwinds.

Furthermore, we gleaned that Wall Street analysts have likely baked in significant pessimism in the bank’s earnings projections for FY22 and FY23. Accordingly, the consensus estimates suggest that Goldman could post an adjusted EPS decline of nearly 45% in FY22 before a recovery in 2023.

Therefore, with such a marked impact on its FY22 profitability projections, we postulate that GS could have staged its lows in June and October before powering a remarkable rally to form its December top (which we cautioned previously).

As such, Goldman’s aggressive approach in lifting its operating leverage suggests that the bank remains in control of its cost management and could improve its ability to meet the Street’s outlook.

Investors also need to remember that the bank wields tremendous leverage against its bankers, given the scale of bonuses in their compensation packages. For example, Bloomberg highlighted in an early December article that:

For legions of bankers and traders, their annual bonuses can stretch into millions of dollars and is many multiples of their annual salary. Wall Streeters spend months banking on their bonuses to pay for tony private schools, luxury vacation homes and private-club memberships. – Bloomberg

Therefore, we assess that the market seems confident that Goldman’s more aggressive bonus management/cuts could give it the edge in FY23, suggesting that investors should stay sanguine.

Of course, Goldman Sachs also needs the investment banking environment to recover in 2023. It may not need to replicate 2021’s tremendous success. Moreover, the earnings estimates for FY23 suggest it’s still expected to be down nearly 40% from FY21’s levels. Hence, analysts aren’t expecting Goldman Sachs to report a spectacular FY23, but it needs to be “less bad” than FY22.

Possible? Why not? If the US economy could skirt a severe recession (our base case), Goldman Sachs remains well-primed to benefit from it. Also, the Fed is expected to taper its rate hike cadence in 2023, which could lead to less market volatility that hampered dealmaking markedly in 2022. Hence, we believe these are reasonable assumptions that Goldman Sachs’ outlook for FY23 isn’t that bad, suggesting much pessimism has likely been priced in.

But does the market agree? Yes. We think it’s reasonable to assume that GS has likely bottomed in October. Why?

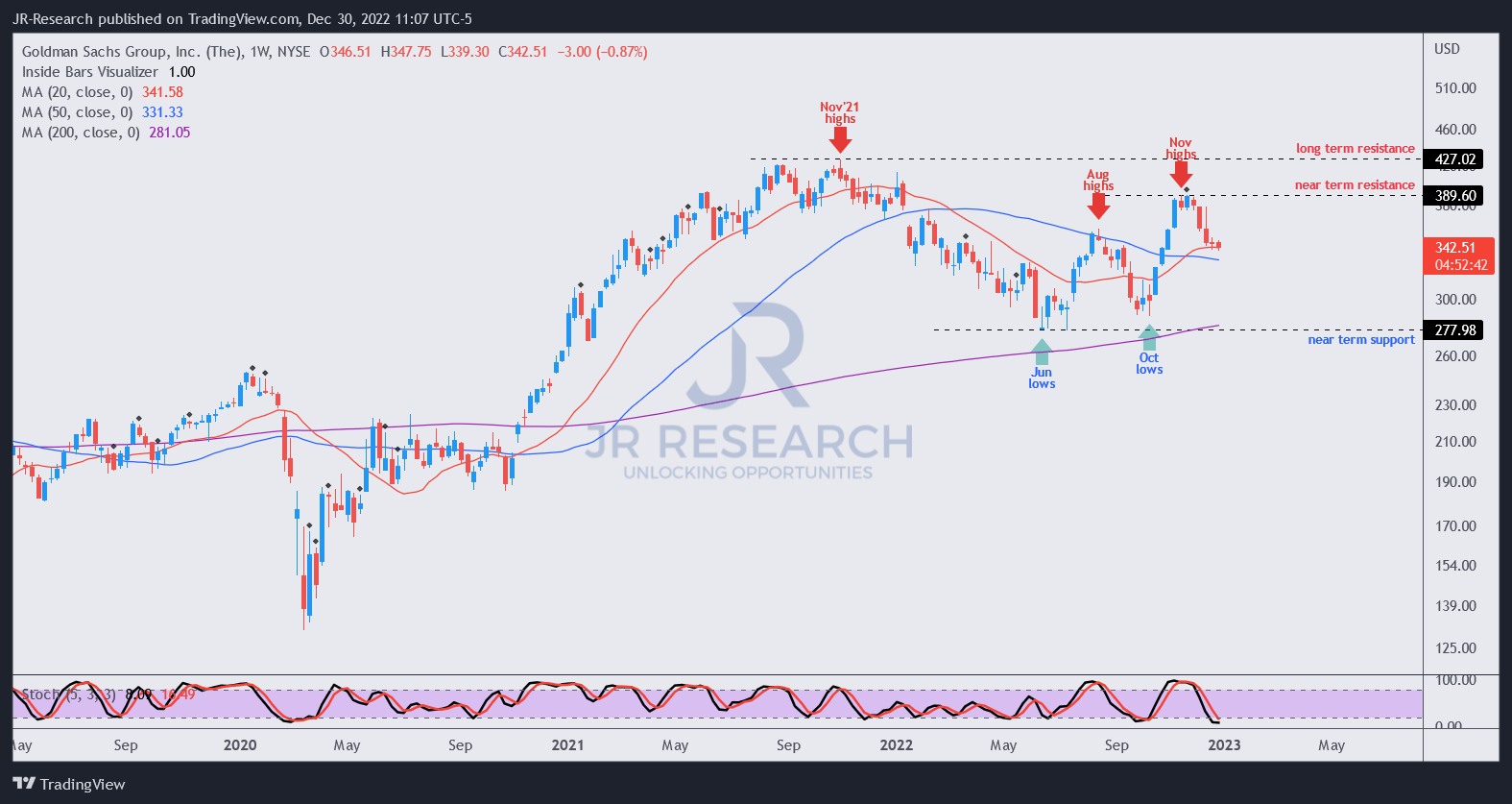

GS price chart (weekly) (TradingView)

In our late September article, we discussed how market operators forced massive pessimism that saw GS form its October bottom shortly after.

The bull trap, following its remarkable rally, then set up its December highs. Hence, we were waiting to glean how the consolidation could follow as we anticipated a pullback discussed in our previous article.

The pullback appears to be robustly supported, as GS regained control of its 20-week moving average or 20-week MA (red line). It’s a pivotal development suggesting that its 50-week MA could help support a medium-term recovery of GS’ medium-term bullish bias from here.

With GS FY24 P/E of 8.2x, it’s way below its 10Y average of 10.3x. Hence, the market has likely not re-rated GS. As such, if we can avoid falling into a deep economic freeze, a further liftoff in GS looks plausible and reasonable from here.

Rating: Buy (Revise from Hold)

Be the first to comment