tdub303

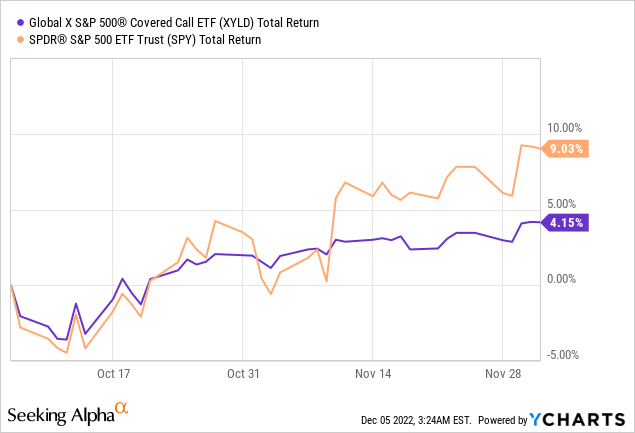

Since the last article I published about the Global X S&P 500 Covered Call ETF (NYSEARCA:XYLD) and the general short-premium ETF space back on October 5th, a lot has happened in markets.

Namely, we went through another one of those dreaded bear-market rallies, the exact thing I warned about in the previous article.

As expected, it resulted in the fund underperforming the index, the S&P 500 (SPY), drastically – resulting in permanent losses for investors in the fund.

This wasn’t surprising to me, and just validates my fears regarding the fund, and the general short-premium ETF space.

Article Thesis

It’s my belief that this underperformance during bear market rallies will continue to punish investors in this fund – and to a significant degree, resulting in permanent capital losses due to realized volatility overstating the expected volatility.

Combine this with the reality that the market is at high valuations, nearly what it was at in September when the effective fed funds rate was around 2.6%, while it currently sits near 3.8%, the market is overbought and due for a pullback.

As a result, now (or soon) is the perfect time to swap out of this broken fund into a simple ETF like the SPY, or simply raise some cash from this position.

Why XYLD is Fundamentally Broken

While I did a bigger deep-dive into the problems with XYLD and put a few arguments as to why it could be broken in my last article about XYLD, I’d like to briefly expand on a few elements that really make this fund broken.

#1 – XYLD sells covered calls too close to the money

Due to the fund’s stated goals, to generate yield, income, they do so quite aggressively choosing to sell relatively close-to-the-money calls that have a higher risk of principle loss.

They sell calls @2% OTM, when the market is experiencing drastic swings, rallying 14% in the last 54 days. This is creating permanent losses of the underlying, as they either have to rebuy the calls or rebuy the underlying at a premium after each of these moves.

#2 – XYLD is getting whip-lashed by volatility

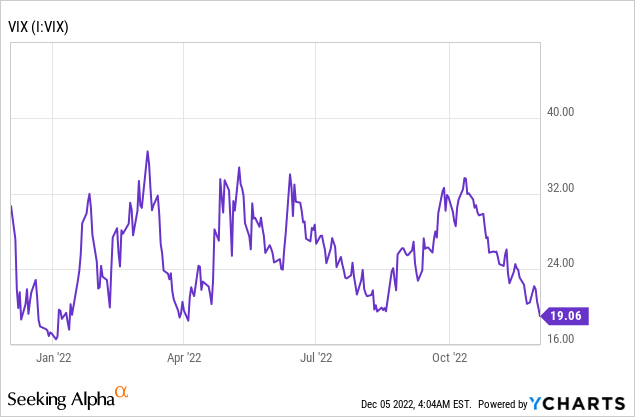

Due to these large swings in sentiment from hyper-bearish and pessimism to hyper-bullish optimism the VIX has been swinging from 19ish to 30+ all year – a trend I believe will continue.

When people are hopeful, like they are now, VIX plummets to <20 – and when people are afraid it skyrockets to >30.

This results in XYLD selling calls for very cheap at the top of rallies, such as now, 2% OTM as normal – but collecting little premium due to the low volatility. They then hold these positions and put new ones on as the market declines and these expire – meanwhile volatility has risen. Premiums have increased.

Instead of doing as most investors would and opting to sell slightly further OTM, yielding the same premiums as before, taking on the same risk as during lower volatility periods, they stick to the 2% OTM rule.

This adds a level of risk, upside risk, in particularly volatile times when outsized moves typically occur – and as a result the fund is experiencing lots of permanent losses.

#3 – The market is simply too volatile now

While it has worked in the past like I pointed out in the previous article, back in 2015~, the market has fundamentally changed. We’re teetering on the edge of a recession, we have war in Europe, China is acting much more rash and hands-on with their markets and governance, rates are high and there is plenty of uncertainty abound in the markets. People can’t even decide if the Fed is pivoting, easing, or continuing its hawkish stance. Inflation narratives have flip-flopped from week to week from “it’s peaked” to “it’s entrenched” to “it’s increasing” to “it’s rolling over” time and time again.

Market conditions changed, and we seem to be in a new era of investing.

Conclusion & Closing Thoughts

Due to general market valuations, combined with this confirmation of my fears, I’d now rate the stock/fund a sell – meaning if it’s not too painful tax-wise to liquidate the position and transfer into an alternative fund such as the S&P 500 (SPY), it would almost certainly be wise over the long term, or at least the next 6-12 months in my opinion.

This doesn’t fit my normal sell criteria of being a short candidate due to borrowing fees + tax consequences, but I’ll make an exception here as it is undoubtedly a sell in the case of longs, at least in my view.

Once this situation improves, volatility reduces, or the fund changes its target OTM sell % I’ll likely revisit this topic once again and change my stance. Until then I would not go long XYLD and would discourage friends and family from holding ongoing positions in the fund.

Actionable Takeaways

If you own XYLD or other covered-call ETFs and are bullish on the market, it’s likely wise to swap them out for the standard ETF versions to stop capping your upside, as the covered-call versions seem to be underperforming drastically unless the VIX stays consistently below 15~ for months on end.

If you own XYLD or other covered-call ETFs and are bearish on the market, it’s likely wise to raise cash from these positions today and look to buy back into the non-covered call varieties a little bit lower – if you don’t want the market risk, then holding your position until the market has gone down a bit, and then swapping over to a non-covered call fund when you turn neutral to bullish on the market.

As mentioned in the previous article, there are some ways to replicate this manually that make sense in my opinion, but they entail more risk – if that’s okay with you, go check out the old actionable takeaways.

Risks to consider

Lastly, before we close out, I’d just like to remind everyone to check into the tax consequences before making any actions.

Due to XYLD’s current price, it is unlikely to come with realized capital gains; however, you should check anyways – you may be able to harvest capital gains losses here before the end of the year if you’ve been long for some time.

Be the first to comment